Report of the Auditor General of Canada to the Board of Trustees of the Canadian Museum of History—Special Examination—2023

Independent Auditor’s Report

Table of Contents

- Audit Summary

- Introduction

- Findings, Recommendations, and Responses

- Commentary on the United Nations’ Sustainable Development Goals and on diversity, equity, and inclusion

- Conclusion

- About the Audit

- List of Recommendations

- Exhibits:

- 1—The Canadian Museum of History and the Canadian War Museum

- 2—The COVID-19 pandemic caused a significant decrease in museum visits

- 3—Corporate governance—Key findings and assessment

- 4—Strategic planning—Key findings and assessment

- 5—Corporate risk management—Key findings and assessment

- 6—The corporation develops, maintains, and promotes its collections

- 7—The Grand Hall at the Canadian Museum of History and Lebreton Gallery at the Canadian War Museum

- 8—Operational planning and performance measurement, monitoring, and reporting—Key findings and assessment

- 9—Collections management—Key findings and assessment

- 10—Conducting research—Key findings and assessment

- 11—Exhibitions and public programs—Key findings and assessment

Audit Summary

We examined how the Canadian Museum of History carried out its corporate management practices and managed its operations for the period covered by the audit.

In examining operations, we found weaknesses in collections conservation that amounted to a significant deficiency. Of these weaknesses, we were particularly concerned that the corporation did not have robust inventory management systems and practices, which put the safeguarding of its collections containing over 4 million objects at risk. There were no action plans to deal with issues such as more than 300 items lacking proper storage, more than 15,000 items lacking source information, and over 800 missing items identified in some inventory verifications performed between 2012 and 2022 in the corporation’s 2 museums. Other weaknesses included a lack of formal documentation for conservation treatment processes and a lack of regular and systematic reviews of individuals’ electronic security access to various locations, including vaults and other places where collections were stored. We also found areas for improvement in the other corporate management practices and operations that we examined.

Except for the significant deficiency and despite weaknesses, the corporation reasonably maintained the systems and practices that we examined to carry out its mandate.

We also noted that the corporation was undertaking important initiatives such as the cultural transformation of its working environment. This comprehensive initiative will likely take considerable time to complete and take hold. For that reason, we encourage the corporation to monitor its progress diligently and its results continually, once implemented.

Introduction

Background

1. The Canadian Museum of History is a federal Crown corporation with a mandate under the Museums Act to enhance Canadians’ knowledge, understanding, and appreciation of events, experiences, people, and objects that reflect and have shaped Canada’s history and identity. Its mandate is also to enhance Canadians’ awareness of world history and cultures. The corporation reports to Parliament through the Minister of Canadian Heritage.

2. The corporation consists of 2 museums in Canada’s National Capital Region (Exhibit 1). The corporation operates

- the Canadian Museum of History in Gatineau, Quebec

- the Canadian War Museum in Ottawa, Ontario

Exhibit 1—The Canadian Museum of History and the Canadian War Museum

Photo: Canadian Museum of History

Photo: Canadian War Museum

3. The corporation’s strategic direction comprises the following 6 strategic objectives:

- inspire Canadians across the country to engage in a greater understanding of their shared history

- position the corporation as a trusted source of research and knowledge about Canadian history

- strengthen relationships with Indigenous peoples through respectful collaboration and shared stewardship of Indigenous collections and intangible heritage

- build and share a collection that best reflects Canada’s history and distinctiveness

- pursue cultural diplomacy to exchange ideas and values and advance mutually beneficial projects, both nationally and internationally

- ensure sustainability, capacity, and museological excellence by continuing to develop an empowering corporate culture

4. The corporation also administers a national investment program called Digital Museums Canada and administers the Canadian Children’s Museum inside the Canadian Museum of History. It also presents a permanent virtual exhibition, the Virtual Museum of New France.

5. As of September 2022, the corporation employed 364 permanent and 38 temporary employees.

6. The restrictions related to the coronavirus disease (COVID‑19)Definition 1 pandemic led to significant decreases in museum visits and in operating revenue (Exhibit 2).

Exhibit 2—The COVID‑19 pandemic caused a significant decrease in museum visits

| 2019–20 | 2020–21 | 2021–22 | |

|---|---|---|---|

| On-site attendance (thousands) | 1,452 | 43 | 189 |

| Operating revenues (thousands) | $14,993 | $769 | $4,252 |

Source: Canadian Museum of History

Focus of the audit

7. Our objective for this audit was to determine whether the systems and practices we selected for examination at the Canadian Museum of History were providing it with reasonable assurance that its assets were safeguarded and controlled, its resources were managed economically and efficiently, and its operations were carried out effectively, as required by section 138 of the Financial Administration Act.

8. In addition, section 139 of the Financial Administration Act requires that we state an opinion, with respect to the criteria established, on whether there was reasonable assurance that there were no significant deficiencies in the systems and practices we examined. We define and report significant deficiencies when, in our opinion, the corporation could be prevented from having reasonable assurance that its assets are safeguarded and controlled, its resources are managed economically and efficiently, and its operations are carried out effectively.

9. On the basis of our risk assessment, we selected systems and practices in the following areas:

The selected systems and practices, and the criteria used to assess them, are found in the exhibits throughout the report.

10. More details about the audit objective, scope, approach, and sources of criteria are in About the Audit at the end of this report.

Findings, Recommendations, and Responses

Corporate management practices

The corporation had good corporate management practices in some areas but needed improvement in others

11. We found that the corporation had some good corporate management practices. However, we found areas for improvement in practices related to board independence; board oversight; performance measurement, monitoring, and reporting; and risk mitigation, monitoring, and reporting.

12. The analysis supporting this finding discusses the following topics:

13. The Board of Trustees is accountable for the overall stewardship of the corporation and for ensuring that the corporation’s business activities contribute to achieving its mandate. The corporation can have up to 11 board members, including the Chairperson and the Vice‑Chairperson. Board members are appointed by the Minister of Canadian Heritage with approval of the Governor in CouncilDefinition 2, a process outside the corporation’s control. At the end of the period covered by the audit, there was 1 vacancy on the board and 1 term had just expired, which did not pose a threat to maintaining quorum. The board is supported by 3 standing committees: Audit and Finance, Governance and Human Resources, and Canadian War Museum.

14. In recent years, the corporation indicated in its corporate plans a need to stabilize its team of executives and senior managers for various reasons, including expected retirements, hiring a new President and Chief Executive Officer, and in response to corporate reorganization. Starting in December 2020, the President and Chief Executive Officer position was vacant and the function was carried out through an interim appointment until December 2022, when that interim appointment became permanent. About half of the corporation’s senior managers had been appointed between January and October of 2022.

15. Additionally, the corporation was undertaking a holistic cultural transformation of its work environment to achieve the following:

- re-shape its culture

- strengthen employee engagement

- improve employees’ well-being and mental health

- increase diversity, equity, and inclusion

This transformation was in its early stages and will likely require considerable time to complete and take hold. Given its importance to the corporation, we encourage the board and executive team to diligently monitor its progress and assess its results once the initiative has been fully implemented.

16. Our recommendations in this area of examination appear at paragraphs 21, 26, 31, and 35.

17. Analysis. We found that the corporation had good systems and practices for board appointments and competencies and for providing strategic direction. However, some areas of board independence and oversight needed improvement (Exhibit 3).

Exhibit 3—Corporate governance—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Board appointments and competencies |

The board collectively had capacity and competencies to fulfill its responsibilities. |

The board developed a board profile that included descriptions of the skills, experience, and knowledge required for board members, along with attributes of diversity, inclusion, and geographical representation. The board developed a skills matrix that mapped board profile attributes against those possessed by its members. Both the board profile and the skills matrix were provided to the Department of Canadian Heritage. Board members were given orientation sessions and the corporation provided opportunities for ongoing training. The board solicited independent advice when necessary to fill gaps in its skills and expertise and to supplement its decision making. |

Check mark in a green circle |

|

Board independence |

The board functioned independently. |

The corporate by law promoted the board’s independence by assigning responsibility for the corporation’s day‑to‑day operations to the President and Chief Executive Officer. The board held regular private meetings without management in attendance. Board members declared conflicts of interest at board meetings. Weaknesses The corporation did not have a code of conduct that applied specifically to its board members. Upon their appointment, board members declared their understanding of and obligation to comply with various policies outlining expected behaviour. However, there was no requirement to subsequently reconfirm those declarations. |

Exclamation point in a yellow circle |

|

Providing strategic direction |

The board provided strategic direction. |

The board reviewed and approved strategic and corporate plans prepared by management. The board was active in setting the President and Chief Executive Officer’s annual objectives and evaluating her performance. These objectives aligned with the corporation’s strategic direction. |

Check mark in a green circle |

|

Board oversight |

The board carried out its oversight role over the corporation. |

The board began a comprehensive review of its terms of reference and that of its committees. The corporation had a calendar for its board committee activities. The board regularly (quarterly) discussed the corporation’s financial status and its progress against strategic targets and various initiatives. The internal audit team conducted audits identified in the corporation’s risk‑based audit plan. Management presented its responses to the audit recommendations to the board. Weaknesses The board did not perform oversight of the corporation’s compliance with corporate policies. Many policies had not been reviewed in a long time. The board did not receive complete risk management information from management (this weakness is discussed in paragraph 33). |

Exclamation point in a yellow circle |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

18. Weaknesses—Board independence. The corporation made available to its board members various legislative authorities and guidelines concerning values, ethics, and conflicts of interest. While the corporation had a code of conduct for its employees, we found that it did not have one explicitly addressed to its board members.

19. Furthermore, we found that after board members declared, upon appointment, their understanding of and obligation to comply with various policies outlining expected behaviour, they were not required to make subsequent declarations confirming their continued understanding and commitment to comply. This finding also applied to the corporation’s employees.

20. These weaknesses matter because adherence to corporate values and ethics and ongoing awareness of the proper handling of potential conflicts of interest are important to establishing the corporation’s credibility and fostering sound governance and accountability.

21. Recommendation. The corporation should establish a code of conduct for its board members. The corporation should also ensure that board members and employees periodically declare their understanding of and commitment to comply with ethical and conflict‑of‑interest requirements and to adhere to the corporation’s values.

The corporation’s response. Agreed. The corporation has drafted a code of conduct for board members and will adopt it in early 2023–24. The corporation will implement a yearly commitment on the part of board members and employees to ethical and conflict of interest requirements and adherence to the corporation’s values.

22. Weaknesses—Board oversight. We found weaknesses in how the board monitored the corporation’s compliance with corporate policies.

23. The corporation had many policies covering various corporate management and operational areas. Some of them required periodic review to ensure that they remained relevant. We found that management did not provide the board with information on compliance with policies. We also found that the policies had not been reviewed regularly and that many of them were considerably more than a decade old. The corporation began reviewing and updating its policies during the period of our audit.

24. Furthermore, we observed that some of the policy requirements were not met. For example, the Research Policy required a research advisory committee to approve research projects, but such a committee did not exist during the period of our audit.

25. These weaknesses matter because the corporation’s policies outline expectations that employees must meet and are an important part of its governance regime. Also, in its oversight role, the board must have confidence that the corporation is complying with its policies, and that the policies are being periodically reviewed to ensure that they remain relevant.

26. Recommendation. Upon comprehensively reviewing and updating its policies, management should provide the board with the information necessary to overseeing the corporation’s compliance with its policies.

The corporation’s response. Agreed. The corporation has developed a Corporate Policy Renewal Framework and is undertaking a comprehensive review and update of its policies. In 2023–24, the corporation will inaugurate a yearly compliance report to assist the board in monitoring the corporation’s compliance with corporate policies.

27. Analysis. We found that the corporation had good practices in its strategic planning processes, but improvement was needed in performance measurement, monitoring, and reporting (Exhibit 4).

Exhibit 4—Strategic planning—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Strategic planning processes |

The corporation established a strategic plan and strategic objectives that were aligned with its mandate. |

The corporation had an annual corporate planning process, through which it developed a corporate plan. The plan aligned with the strategic objectives, which were consistent with its mandate. The corporate planning process took into account internal and external environments. Strategic objectives and corporate plans were communicated to employees through the corporate intranet and employee meetings. |

Check mark in a green circle |

|

Performance measurement, monitoring, and reporting |

The corporation established performance indicators in support of achieving its strategic objectives and monitored and reported on its progress against these indicators. |

The corporation had a recently updated performance measurement framework, which provided a structure to plan and budget for the corporation’s activities and report on its results. Each strategic objective had accompanying performance indicators and targets consistent with those outlined in the performance measurement framework. Management held regular meetings to discuss progress on various activities related to the strategic objectives. Management monitored and measured results against the strategic objectives and reported them quarterly to the board. The corporation published its annual report and held an annual public meeting. Weakness The corporation did not establish performance indicators and targets to measure its achievement of some of the priorities and key activities that supported its strategic objectives. |

Exclamation point in a yellow circle |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

28. Weakness—Performance measurement, monitoring, and reporting. We found that the corporation did not establish performance indicators and targets to measure the achievement of some of its priorities and key activities supporting its strategic objectives.

29. The corporate plan identified between 1 and 3 performance indicators and targets for each of its 6 strategic objectives, to measure their progress. Also, for each strategic objective, the corporate plan described several high‑level priorities and highlighted key activities. We found that some of these activities did not have performance indicators and targets and that the corporation did not systematically monitor and report on their achievement to the board or in the annual report. For example, one of the key activities was to upgrade a particular section of 1 gallery, but the corporation did not report progress on this activity to the board or in the annual report.

30. This weakness matters because without performance indicators and targets for priorities and key activities that support the strategic objectives, the corporation cannot systematically measure and monitor their achievement. This, combined with the absence of specific reporting on each key activity, meant that the board and stakeholders could not determine whether some of these activities had achieved their planned outcomes.

31. Recommendation. The corporation should set clear performance indicators and targets for the priorities and key activities presented in its corporate plans. It should report regularly to the board on their achievement and include this information in its annual report.

The corporation’s response. Agreed. In 2023–24, the corporation will renew its Performance Measurement Framework and performance reports to the board and to the senior leadership team, so that clear performance indicators are monitored against milestones. The corporation will continue to report on performance quarterly to the board and include results in the annual report.

32. Analysis. We found that the corporation had good practices for identifying and assessing risks. However, improvements were needed in risk mitigation, monitoring, and reporting (Exhibit 5).

Exhibit 5—Corporate risk management—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Risk identification and assessment |

The corporation identified and assessed risks to achieving strategic objectives. |

The corporation recently updated its risk management framework, which included the key elements of risk management best practices and a corporate risk profile. The corporation identified its corporate and operational risks, which it assessed according to their likelihood of occurrence and their potential impact. |

Check mark in a green circle |

|

Risk mitigation |

The corporation defined and implemented risk mitigation measures. |

Weaknesses The corporation did not formally develop risk appetite statements and risk tolerance levels. The corporation’s risk profile described mitigation measures. However, for some risks, the action plans to mitigate them were not clearly defined, and there were no specific timelines for the mitigation measures. |

Exclamation point in a yellow circle |

|

Risk monitoring and reporting |

The corporation monitored and reported on the implementation of risk mitigation measures. |

The corporate risk profile was updated and reported quarterly to both senior management and the board. Weakness Management provided the board with updated risk profiles, but these did not include the risk mitigation strategies planned for upcoming quarters. |

Exclamation point in a yellow circle |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

33. Weaknesses—Risk mitigation, monitoring, and reporting. We found that the corporation did not develop risk appetite statements and risk tolerance levels. Also, some of its risk mitigation strategies lacked action plans and generally lacked specific timelines. Because the mitigation strategies presented to the board lacked these elements, it was challenging for the board to understand how they would be implemented and what impact they would have. The corporation’s risk profile used by management included brief descriptions of mitigation strategies, but the implementation timeline was general in nature and spanned only the next few quarters.

34. These weaknesses matter because without well‑defined mitigation strategies, risk appetite statements and tolerances, and time‑bound, detailed action plans, the board and management could not ensure that the corporation had effective practices to mitigate the risks to achieving its objectives.

35. Recommendation. The corporation should further define its mitigation strategies and develop risk appetite statements and risk tolerances, and specific action plans. Implementation of those action plans and any associated target dates should be reported in the corporate risk profile to both senior management and the board.

The corporation’s response. Agreed. In 2023–24, the corporation will develop risk appetite statements and risk tolerances. It will develop more robust mitigation strategies and specific action plans for its corporate risks and report on them quarterly to the senior leadership team and the board.

Management of operations

The corporation had a significant deficiency in collections conservation and needed improvements in all other operational areas we examined

36. We found weaknesses in collections conservation that amounted to a significant deficiency. The corporation lacked clear guidelines for approving and reviewing conservation treatments and could not consistently and systematically demonstrate that this was being performed in the treatments we examined. Inventory verifications were performed on an ad hoc basis and there were no plans to resolve any problems uncovered in these verifications, including finding missing items. Also, the corporation had not regularly or systematically reviewed electronic access permissions.

37. We also found weaknesses in all other areas of managing operations that we examined. These included

- insufficiently defined elements for planned activities in the key operational work plan preparation process

- not completing certain steps on time in collection acquisitions (adding items to the collection) and deaccessions (removing items from the collection)

- a lack of formal processes and documentation in conducting research

- inconsistent application of exhibitions and public program process requirements

38. The analysis supporting this finding discusses the following topics:

- Operational planning and performance measurement, monitoring, and reporting

- Collections management

- Conducting research

- Exhibitions and public programs

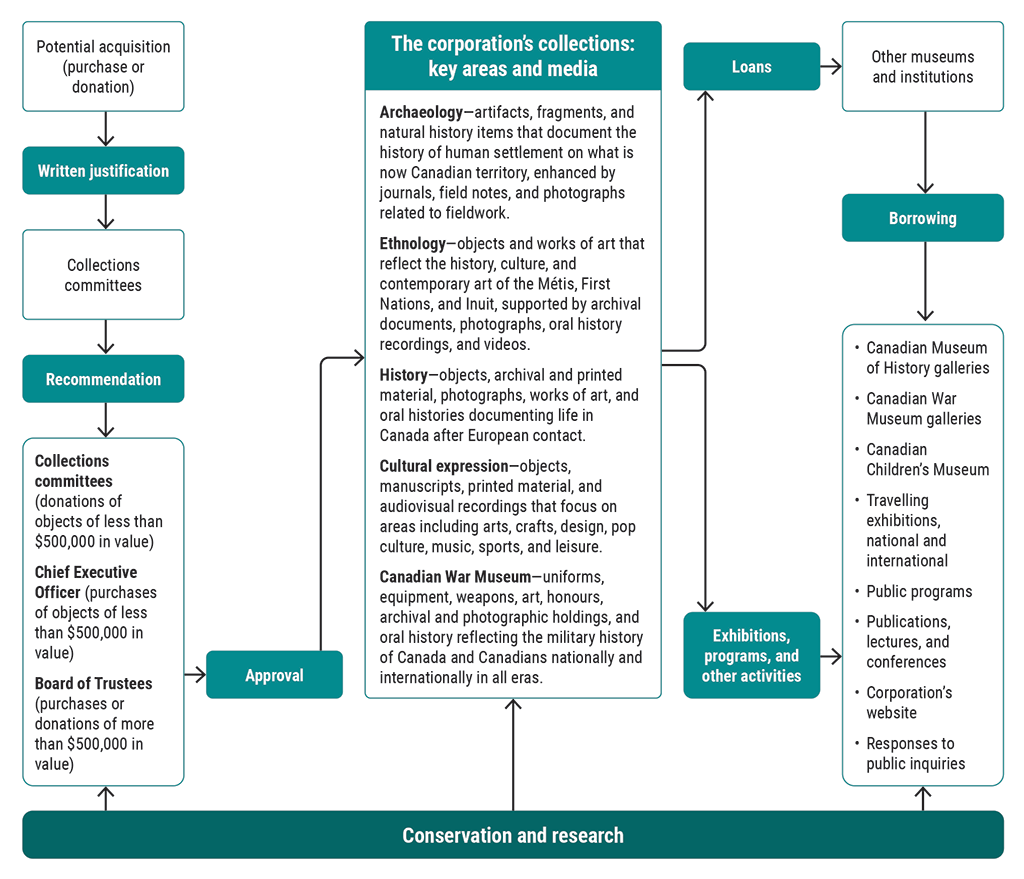

39. The corporation’s important business activities consist of developing and conserving its collections, conducting research, and delivering exhibitions and public programs (Exhibit 6).

Exhibit 6—The corporation develops, maintains, and promotes its collections

Source: Based on information from the Canadian Museum of History

Exhibit 6—text version

This chart shows how the corporation develops, maintains, and promotes its collections.

The corporation develops its collections through acquisitions. In the case of a potential acquisition through purchase or donation, the collections committees receive a written justification for the acquisition. The committees review the written justification for the proposed acquisition and make a recommendation.

Recommendations require approval, and approvals depend on the dollar value of the acquisition:

- Collections committees approve donations of objects of less than $500,000 in value.

- The Chief Executive Officer approves purchases of objects of less than $500,000 in value.

- The Board of Trustees approves purchases or donations of more than $500,000 in value.

If approved, the corporation acquires the object or objects.

The corporation’s collections include the following key areas and media:

- Archaeology—artifacts, fragments, and natural history items that document the history of human settlement on what is now Canadian territory, enhanced by journals, field notes, and photographs related to fieldwork.

- Ethnology—objects and works of art that reflect the history, culture, and contemporary art of the Métis, First Nations, and Inuit, supported by archival documents, photographs, oral history recordings, and videos.

- History—objects, archival and printed material, photographs, works of art, and oral histories documenting life in Canada after European contact.

- Cultural expression—objects, manuscripts, printed material, and audiovisual recordings that focus on areas including arts, crafts, design, pop culture, music, sports, and leisure.

- Canadian War Museum—uniforms, equipment, weapons, art, honours, archival and photographic holdings, and oral history reflecting the military history of Canada and Canadians nationally and internationally in all eras.

The corporation lends objects from its collection to other museums and institutions, and it borrows objects from other museums and institutions. Objects that the corporation makes available to the public can include objects from its collections and borrowed objects.

The corporation promotes its collections and makes them available to the public through exhibitions, programs, and other activities:

- Canadian Museum of History galleries

- Canadian War Museum galleries

- Canadian Children’s Museum

- Travelling exhibitions, national and international

- Public programs

- Publications, lectures, and conferences

- Corporation’s website

- Responses to public inquiries

The corporation’s conservation and research activities contribute to developing, maintaining, and promoting its collections.

40. Collections. Both of the museums manage their own collections. The Canadian Museum of History collections are wide‑ranging and contain approximately 3.8 million objects, including works of art, archival documents, photographs, audiovisual archives, and archaeological items. These collections fall into 4 major categories: archaeology, ethnology, history, and cultural expression. The collections of the Canadian War Museum contain more than 500,000 objects, including uniforms, medals, archival documents, photographs, audiovisual archives, vehicles, and works of art.

41. Collections development. The corporation adds to its collections primarily through funding from its annual budget provided by the government and through donations. In the 2021–22 fiscal year, spending on acquisitions amounted to $2.5 million from the annual budget, while donations amounted to $700,000.

42. Collections conservation. The corporation’s conservation systems and practices are governed by its Conservation Policy. These include the examination of and treatments carried out on objects, with the aim of slowing their deterioration. A treatment may range from simple stabilization to extensive intervention, including restoration (returning an object to the appearance and condition of some known former state). Conservation also includes the documented narrative or illustrated record of the physical state of an object, including the record of the applied conservation treatments. Safeguarding activities, such as monitoring environmental conditions, protecting collections from pests, providing support and protection through appropriate storage mounts and containers, and controlling access to collections, are also part of conservation.

43. Conducting research. Research provides a basis for collecting and preserving the museums’ national collections. The corporation’s 10‑year Research Strategy provides a framework to guide research activities at both museums, under 3 areas of concentration: Meaning and Memory, First Peoples, and Compromise and Conflict. This strategy guides the subjects and types of material studied, collected, and disseminated. Results of research are used in different contexts, including informing exhibitions, publishing research papers and books, and sharing expertise through seminars, lectures, and workshops. Examples include

- participation in an Indigenous Archaeological Field School with members of local Pikwàkanagàn and Kitigan Zibi communities, to teach Indigenous youth about archaeology and help them discover their own history

- “In Their Own Voices,” a Canadian War Museum oral history project designed to preserve the memories and experiences of Canadian veterans and their families

- publication of books in the Mercury Series, such as 1968 in Canada: A Year and Its Legacies; and Material Traces of War: Stories of Canadian Women and Conflict, 1914–1945

44. Exhibitions and public programs. Exhibitions and public programs are key means by which the corporation makes its collection known and furthers Canadians’ knowledge, understanding, and appreciation of events that have shaped Canadian and world history.

45. The corporation displays artifacts within its galleries through permanent and special temporary exhibitions in the National Capital Region, travelling exhibitions, virtual exhibits, and through its online databases. Exhibitions during our period of examination included the following:

- Permanent exhibition halls, such as the Grand Hall of the Canadian Museum of History (Exhibit 7), which offers an introduction to the history, cultures, and beliefs of the First Peoples of Canada’s Pacific coast. It includes exhibits of large totem poles, Indigenous houses, and sculptures of national significance. The Lebreton Gallery of the Canadian War Museum contains the most extensive collection of military weapons, vehicles, and equipment in Canada.

- Queens of Egypt: a special exhibition developed by the Pointe‑à‑Callière Montréal Archaeology and History Complex, in collaboration with Museo Egizio (Turin, Italy), that explored stories of women of power in ancient Egypt.

- Munnings—the War Years: a Canadian War Museum travelling exhibition, displaying paintings by Sir Alfred Munnings that depict activities of the Canadian Cavalry Brigade and the Canadian Forestry Corps.

- The W. J. Roué Collection—Bluenose and Beyond: an online exhibition presenting the life and achievements of Canada’s best‑known naval architect as well as a look at the care and conservation of the collection.

Exhibit 7—The Grand Hall at the Canadian Museum of History and Lebreton Gallery at the Canadian War Museum

Photo: Canadian Museum of History

Photo: Canadian War Museum

46. Public programs are organized encounters between visitors and the museums. These encounters are sometimes linked to exhibitions or formal educational curriculums but often exist independently. School programs include on‑site and online programs and sharing resource materials. Other public programs include large group events such as behind‑the‑scenes tours, conferences, lectures, and workshops. For example, the “An Evening With” conference series invites guests to discuss their chosen career or expertise. Also, Virtual School Programs provide educational content for students, such as “This Belongs in a Museum—First World War Edition,” where students investigate 3 intriguing artifacts from the Canadian War Museum galleries.

47. Our recommendations in this area of examination appear at paragraphs 53, 59, 68, 69, 70, 74, and 79.

48. Analysis. We found that the corporation had weaknesses in operational planning, as well as in performance measurement, monitoring, and reporting (Exhibit 8).

Exhibit 8—Operational planning and performance measurement, monitoring, and reporting—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Operational planning |

The corporation’s operational planning aligned with its strategic objectives. |

The corporation had an operational planning process that required each division to prepare work plans. These plans included descriptions of activities that were aligned with approved strategic objectives and identified the resources required to achieve them. Weakness The corporation did not conduct operational planning consistently through the use of work plans. |

Exclamation point in a yellow circle |

|

Operational performance measurement, monitoring, and reporting |

The corporation established performance indicators to measure its operational performance and monitored and reported on progress. |

The corporation used its operational planning process to monitor and assess ongoing resource needs. The corporation undertook some visitor appreciation surveys, which included metrics to quantify satisfaction. It frequently requested feedback for its public programs. Weaknesses The corporation did not develop performance indicators that would enable proper monitoring of the implementation of planned activities. The corporation did not use its divisions’ work plans to monitor their performance. |

Exclamation point in a yellow circle |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

49. Weaknesses—Operational planning and performance measurement, monitoring, and reporting. Although operational planning was guided by formal practices such as the use of work plans, we found that there were weaknesses in the quality of the information provided in the work plans and in the use of that information.

50. Each division in the corporation prepared a work plan to guide its work toward achieving the corporation’s strategic objectives. The work plans included project descriptions, performance indicators, alignment with strategic directions, and the budget required for carrying out each project. We found weaknesses in the work plan process. For example, although the 2 museums have similar work in conservation, the breakdown of that work in the 2 museums’ work plans was very different. This raised the question of whether the level of detail across various work plans was sufficient to clearly communicate what was required to carry out the work and meet expectations for divisions. Also, the performance indicators in the work plans often constituted qualitative descriptions, rather than measurable indicators with targets. Such indicators would allow for more effective monitoring of whether the activity was achieved.

51. We also found that the work plans were primarily used for assessing the required levels of human and financial resources, as opposed to monitoring and reporting on operational performance. We did not find specific documented performance assessments of each planned activity. According to management, operational performance was largely monitored through ongoing informal discussions with staff.

52. These weaknesses matter because sound operational planning clarifies expectations to those responsible for meeting them. This also helps managers monitor whether the targeted performance has been achieved and determine whether to take corrective action if needed.

53. Recommendation. The corporation should ensure that work plans include enough detail to communicate expectations of employees. This includes setting clear performance indicators and targets. The corporation should use these indicators to systematically monitor operational progress and report on its achievement.

The corporation’s response. Agreed. The corporation is currently reviewing its work planning processes and in 2023–24 will launch a renewed process for the 2024–25 work planning exercise. The corporation will standardize the level of work details and the type of performance indicators required for approval and monitoring by management and will use the work plans as a basis for approving projects and monitoring and reporting on operational progress.

54. Analysis. We found weaknesses in both collections development and collections conservation. The combined weaknesses in collections conservation amounted to a significant deficiency (Exhibit 9).

Exhibit 9—Collections management—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Collections development |

The corporation collected objects of historical or cultural interest and other museum material. |

The corporation had a Collections Development Plan, and documented detailed acquisition and deaccessioning processes. The corporation’s acquisition of objects aligned with priorities established in its Collections Development Plan. Acquisitions and deaccessions were properly authorized. Weaknesses The acquisition and deaccessioning processes were not completed within target timelines for many artifacts. The Collections Development Plan identified several complex challenges that called for the formulation of action plans to overcome them. Activities, when undertaken, generally did not have such action plans. |

Exclamation point in a yellow circle |

|

Collections conservation |

The corporation maintained its collections by preservation, conservation, or restoration, or the establishment of records or documentation. |

The corporation protected its collections through the use of security guards at its museums, environmental monitoring, pest management, and the use of electronic access cards. The corporation assessed the condition of newly acquired items to be used in exhibitions, to propose treatments when necessary. Significant deficiency The corporation did not formally document conservation treatment processes, including specific approval and review requirements, to help employees meet related corporate expectations. The corporation did not have comprehensive inventory management processes to guide the verification of its collections and the resolution of identified issues. While the corporation undertook some inventory verifications, the identified issues were not resolved. The corporation did not regularly or systematically review individuals’ electronic security access to various locations, including vaults and other places where collections were stored. |

An X in a red circle |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

55. Weaknesses—Collections development. The corporation had formal processes to evaluate and process potential acquisitions and deaccessions, indicating key steps (proposal, decision, and intake or transfer), required approvals, and target timelines for completion. However, the corporation did not complete acquisition and deaccessioning processes within the target timelines.

56. The corporation required that the intake of acquisitions and the transfer of deaccessioned objects be completed within 4 months of receiving approval from a collections committee. We examined 18 acquisitions and found that 12 did not have their intake process completed within this timeframe, with some timelines reaching 8 months at the time of our examination. Similarly, of the 20 items approved for deaccessioning in November 2021 that we examined, 15 still needed to be transferred at the time of our audit, and 7 of them were still displayed in an exhibition gallery. The corporation did not have an action plan to complete these processes. Furthermore, due to the length of time it took for the corporation to make a decision and lack of clear tracking, an opportunity for an acquisition deemed to be of national significance was lost.

57. We also found that the corporation identified challenges related to collections management in its Collections Development Plan for the period spanning from 2016 to 2026. The Collections Development Plan noted that to resolve these challenges, action plans were required. We observed that the corporation was working toward addressing some of these challenges; however, it was not doing so in a systematic way or following an action plan. Therefore, it did not have a clear assessment of the progress it had made within identified areas, including the inventory verification of some of the collections (discussed in paragraphs 63 and 64).

58. These weaknesses matter because delayed processing of acquisitions or missed opportunities to acquire important items can affect the development and quality of exhibitions and public programs. Delayed processing of items to be deaccessioned can affect the resources required to store and maintain them. Also, when challenges identified in the Collections Development Plan are not addressed systematically, this prolongs the risks that those challenges pose.

59. Recommendation. The corporation should ensure that it meets its standards for processing acquisitions and deaccessions. Furthermore, given the lack of clarity on the resolution of challenges identified in the Collections Development Plan that spans the 2016–2026 period, the corporation should review this plan, develop appropriate action plans, and systematically monitor the progress of their implementation.

The corporation’s response. Agreed. In 2023–24, the corporation will review and reissue standards for processing acquisitions and deaccessions, better tailored to the various types of acquisitions and deaccessions, and will put in place an effective monitoring and reporting regime. The corporation will review and update the Collections Development Plan in 2024–25 and institute action plans to address identified challenges, with quarterly reporting to senior leadership.

60. Significant deficiency—Collections conservation. The corporation had several weaknesses in collections conservation that, taken together, amounted to a significant deficiency.

61. The corporation had a process to identify artifacts that required treatments, evaluate their condition, and propose and conduct treatments. However, we found that it had not formally clarified all important requirements such as mandatory steps, reviews, and approvals.

62. In the absence of clearly documented requirements, corporation officials advised us that normally, treatments proposed by a curator or conservation specialist should be approved by a manager. In the 13 treatments that we examined, evidence of approval could not be clearly demonstrated in 5. In 3 of those 5 instances, the corporation indicated that approvals were not needed because the treatments were considered minimal. However, we found that there was no formal guidance describing what actions constituted minimal treatments.

63. We also found that the corporation did not have comprehensive formal procedures and guidelines for inventory verification. While the Canadian Museum of History had issued guidelines on how inventory verification procedures should be performed, they lacked clarity in several areas, notably in the resolution of identified issues. The Canadian War Museum did not have any documented inventory verification procedures.

64. We reviewed the progress made by the corporation in resolving identified issues from 3 of its inventory verifications performed between November 2016 and March 2022 at the Canadian Museum of History. We also reviewed a large-scale inventory verification of more than 500,000 objects at the Canadian War Museum performed between 2012 and 2014. We found the following:

- The inventory verification of various rooms completed at the Canadian Museum of History in March 2022 identified more than 700 issues, of which almost 400 were still awaiting resolution in August 2022, with no formal plan or timeline to address them. These issues included close to 300 instances relating to a lack of proper storage due to deteriorated containers or overcrowded shelving and almost 80 missing items, 5 of which were deemed to be of great historical significance. The type of issues were similar in all 3 inventory verifications.

- At the Canadian War Museum, close to 22,000 issues remained unresolved at the time of our audit, including lack of source information for more than 15,000 items, and approximately 750 missing items.

65. Additionally, in 2016, the corporation committed to constructing a databank of an estimated 1.1 million archeological records as a first step in inventorying this collection. However, approximately 200,000 records were not completed by the initial target date of 31 March 2022, and no new timelines had been established.

66. We also found that the corporation had systems and practices to protect the physical integrity of its collections, including electronic locks limiting access to approved individuals only. However, the corporation did not regularly and systematically review these accesses. The last review occurred in 2005 for the Canadian War Museum, and in March 2021 for the Canadian Museum of History. At the time of our audit, the corporation had not planned future reviews.

67. These weaknesses, which amount to a significant deficiency in collections conservation, matter because proper conservation helps maintain historical objects for future generations, which is a fundamental component of the corporation’s mandate. Comprehensive inventory verification procedures serve many purposes, including identifying necessary time‑sensitive conservation treatments, potential storage threats, internal control weaknesses potentially leading to theft, and the ability to support specific exhibitions and public programs. Also, systematic and periodic review of physical access to collection areas would reduce the risks of damage and theft.

68. Recommendation. The corporation should identify specific review and approval steps in its processes for the conservation treatments of its artifacts and should monitor to ensure that employees comply with these steps.

The corporation’s response. Agreed. In 2023–24, the corporation will develop specific review and approval steps for artifact conservation, clearly defining the authorizations required for different levels of treatment. The corporation will put in place an effective monitoring and reporting regime by 31 March 2024.

69. Recommendation. The corporation should update its collections inventory management process for both museums and ensure that appropriate, time‑bound action plans are developed to address identified ssues.

The corporation’s response. Agreed. In 2023–24, the corporation will review and update inventory management procedures for its collections. The corporation will also develop action plans with reasonable timelines to address already identified issues, as well as issues identified in future inventory verifications, by 31 March 2024.

70. Recommendation. The corporation should regularly and systematically review all granted access permissions.

The corporation’s response. Agreed. In 2023–24, the corporation will renew access protocols and will review permission lists regularly, ensuring that the security database reflects appropriate access controls. It will continue to modernize its security infrastructure to enhance reporting and tracking of access permissions, with the access control portion completed by 31 March 2024.

71. Analysis. The corporation had some good practices for conducting research. However, there was an opportunity to strengthen them through formalization (Exhibit 10).

Exhibit 10—Conducting research—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Conducting research |

The corporation undertook or sponsored research related to its purpose or to museology and communicated the results of that research. |

The corporation developed a research strategy consistent with its mandate and highlighted priorities under 3 themes: Meaning and Memory, First Peoples, and Compromise and Conflict. The corporation undertook research activities that aligned reasonably with its research strategy. Research results were shared with the public through conference presentations, research papers, and within exhibitions, virtual exhibits, and public programs. Weakness The corporation did not have formally documented processes that would help researchers meet corporate expectations when conducting research. |

Exclamation point in a yellow circle |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

72. Weakness—Conducting research. We found that although the research divisions within the 2 museums used various practices to plan, conduct, monitor, and report on progress of research activities, they had not formalized them as they had for other areas of operations, such as exhibitions or acquisitions. For example, there was no standardized minimum requirement for the documentation that should be included in the initial proposals for research projects. We examined 10 such proposals and found that 3 of them did not clearly and consistently document some essential planning information, such as required human and financial resources or clear timelines for completion of deliverables. For 9 of the project proposals, there was no documented evidence that a manager had reviewed or approved the proposal before research activities were conducted.

73. This weakness matters because formalized, documented processes and requirements provide employees with a clear understanding of the practices to be used to promote efficiencies, provide support for the diligent use of resources, and monitor whether research activities are effective. Formal documentation is especially important in the context of staff changes, to ensure that all employees have a reference point that clearly sets out the purpose and expected outcomes of their work.

74. Recommendation. The corporation should develop formal documented processes and templates to help researchers understand corporate expectations and to help managers ensure that those expectations are met.

The corporation’s response. Agreed. The corporation is updating its Research Policy and when approved in 2023–24, the policy will provide clarity on research processes and corporate expectations for research. In 2023–24, the corporation will implement the consistent use of research project proposals and tracking templates. These tools will formalize approvals to ensure alignment with corporate priorities and track deliverables against key milestones.

75. Analysis. We found that the corporation delivered exhibitions and public programs that were consistent with its mandate but had weaknesses in their development and delivery (Exhibit 11).

Exhibit 11—Exhibitions and public programs—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Exhibitions and public programs |

The corporation developed and delivered exhibitions and public programs to promote knowledge and disseminate information related to its purpose. |

The corporation planned, developed, and delivered exhibitions and public programs that were consistent with its mandate. It used various means to deliver them, including travelling exhibitions, digital exhibitions, and online public programs, in addition to the offerings at its 2 museums. The corporation had several documents governing exhibitions and public programs. Weakness The corporation did not meet some important requirements of its Experience Development Process. |

Exclamation point in a yellow circle |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

76. Weakness—Exhibitions and public programs. The corporation had a formal Experience Development Process for exhibitions and public programs that provided detailed requirements for their planning, development, implementation, delivery, and conclusion. However, the corporation could not demonstrate that some important steps were performed as the process required.

77. We examined 11 exhibitions and 9 public programs that were at various stages of development and implementation. We found a lack of idea proposal documents required to describe necessary resources and other project parameters. We also found a lack of overall experience assessments following the end of all of the exhibitions we reviewed, and the lack of some documented approvals and decisions required during the planning to implementation phases.

78. This weakness matters because the Experience Development Process is central to the corporation’s control framework, which identifies corporate expectations for developing, presenting, validating, and delivering exhibitions and public programs. It also matters because following the Experience Development Process could contribute to more efficient and effective use of resources.

79. Recommendation. The corporation should update its formal processes and guidelines for developing and delivering exhibitions and public programs and then monitor to ensure that key requirements are being followed.

The corporation’s response. Agreed. The corporation will review and modernize its formal processes and guidelines for developing exhibitions and public programs. This modernization will include an updated monitoring approach to ensure that requirements are being followed, and will be implemented in 2024–25.

Commentary on the United Nations’ Sustainable Development Goals and on diversity, equity, and inclusion

80. Evolving expectations of Crown corporations. In 2015, Canada and other United Nations member states adopted the 2030 Agenda for Sustainable Development, a vision for partnership, peace, and prosperity for all people and the planet. The 2030 Agenda outlined 17 Sustainable Development Goals that aimed to address current and future social, economic, and environmental challenges. At the national level, the Government of Canada reiterated its commitment to implementing these goals.

81. The federal government has established formal expectations for the integration of the Sustainable Development Goals by federal departments and agencies. As announced in Budget 2021, most of Canada’s large Crown corporations (entities with over $1 billion in assets) will report on their climate-related financial risks for their financial years, starting with the 2022 calendar year at the latest. Budget 2021 also proposed that Crown corporations be required to implement gender and diversity reporting.

82. In our view, the United Nations’ Sustainable Development Goals offer a framework for organizations, including Crown corporations, to identify and positively contribute to social, economic, and environmental effects through their activities and to report on results. We encourage Crown corporations to consider and integrate these goals as a means of embedding sustainability considerations, as well as diversity, equity, and inclusion, into their operations, while supporting the government in these important initiatives. As part of its Sustainable Development Strategy, the Office of the Auditor General of Canada has committed to reporting on progress toward sustainable development goals in the course of performing its audit work. Accordingly, we examined whether the corporation had integrated these goals into its operations.

83. United Nations’ Sustainable Development Goals. While the corporation is not yet required to follow the federal government’s aforementioned expectations for federal departments and agencies, and has not formalized its strategic sustainable development vision in a framework, it had taken some actions that align with the Sustainable Development Goals. For example, over the past several years, the corporation noted that it maintained a geothermal cooling system to generate some of its electricity at the Canadian Museum of History. It used river water to maintain both museums’ grounds and to flush toilets and urinals at the Canadian War Museum. The corporation made various facilities and equipment upgrades to maximize energy savings, including the conversion of fluorescent lighting to high‑efficiency light emitting diodesLEDs with motion sensors, and the replacement of certain water pumping and air control systems with more energy-efficient models.

84. Diversity, equity, and inclusion. The corporation has been working on a diversity, equity, and inclusion strategy and initiatives for several years. For example, it held awareness-raising activities such as lunchtime talks that enabled employees to share their experiences to generate dialogue and enhance understanding. To further formalize its efforts in this area, the corporation recently hired a director whose priorities include managing diversity, equity, and inclusion matters and developing a plan for implementing a diversity, equity, and inclusion strategy to be launched in the 2023–24 fiscal year. These initiatives are consistent with the corporation’s objective within its cultural transformation action plan to strengthen diversity, equity, and inclusion in its workplace.

85. The corporation had an action plan to implement its framework for Indigenous relations and had Indigenous matters embedded in various operations. Officials also informed us that the corporation had begun developing a plan in 2020 for incorporating gender and other considerations into program planning. However, we noted that that plan has not been updated since the amalgamation of the 2 museums’ learning functions. The corporation did make some efforts toward including gender considerations in its delivery of programs. For example, the third gallery of the Canadian History Hall of the Canadian Museum of History includes a large section on diversity and human rights, which contains a subsection on the more recent evolution of Lesbian, Gay, Bisexual, Transgender, Queer, Two-Spirit, PlusLGBTQ2S+ rights and recognition in Canada.

86. In general, the corporation demonstrated in various ways its awareness of the importance of diversity, equity, and inclusion, corporately and in individual museums, to both internal and external audiences. We encourage the corporation to undertake diversity, equity, and inclusion initiatives in a comprehensive and coordinated manner that consolidates various initiatives in 1 place to ensure that it successfully and efficiently achieves its strategic objectives in this area.

Conclusion

87. In our opinion, on the basis of the criteria established, there was a significant deficiency in the corporation’s collections conservation, but there was reasonable assurance that there were no significant deficiencies in the other systems and practices we examined. We concluded that except for this significant deficiency, the Canadian Museum of History maintained its systems and practices during the period covered by the audit in a manner that provided the reasonable assurance required under section 138 of the Financial Administration Act.

About the Audit

This independent assurance report was prepared by the Office of the Auditor General of Canada on the Canadian Museum of History. Our responsibility was to express

- an opinion on whether there was reasonable assurance that during the period covered by the audit, there were no significant deficiencies in the corporation’s systems and practices we selected for examination

- a conclusion about whether the corporation complied in all significant respects with the applicable criteria

Under section 131 of the Financial Administration Act, the corporation is required to maintain financial and management control and information systems and management practices that provide reasonable assurance of the following:

- Its assets are safeguarded and controlled.

- Its financial, human, and physical resources are managed economically and efficiently.

- Its operations are carried out effectively.

In addition, section 138 of the act requires the corporation to have a special examination of these systems and practices carried out at least once every 10 years.

All work in this audit was performed to a reasonable level of assurance in accordance with the Canadian Standard on Assurance Engagements (CSAE) 3001—Direct Engagements, set out by the Chartered Professional Accountants of Canada (CPA Canada) in the CPA Canada Handbook—Assurance.

The Office of the Auditor General of Canada applies the Canadian Standard on Quality Management 1—Quality Management for Firms That Perform Audits or Reviews of Financial Statements, or Other Assurance or Related Services Engagements. This standard requires our office to design, implement, and operate a system of quality management, including policies or procedures regarding compliance with ethical requirements, professional standards, and applicable legal and regulatory requirements.

In conducting the audit work, we complied with the independence and other ethical requirements of the relevant rules of professional conduct applicable to the practice of public accounting in Canada, which are founded on fundamental principles of integrity, objectivity, professional competence and due care, confidentiality, and professional behaviour.

In accordance with our regular audit process, we obtained the following from the corporation:

- confirmation of management’s responsibility for the subject under audit

- acknowledgement of the suitability of the criteria used in the audit

- confirmation that all known information that has been requested, or that could affect the findings or audit conclusion, has been provided

- confirmation that the audit report is factually accurate

Audit objective

The objective of this audit was to determine whether the systems and practices we selected for examination at the Canadian Museum of History were providing it with reasonable assurance that its assets were safeguarded and controlled, its resources were managed economically and efficiently, and its operations were carried out effectively, as required by section 138 of the Financial Administration Act.

Scope and approach

Our audit work examined the Canadian Museum of History. The scope of the special examination was based on our assessment of the risks the corporation faced that could affect its ability to meet the requirements set out in the Financial Administration Act.

As part of our examination, we interviewed the board trustees, senior management, and other employees throughout the corporation to gain insights into its systems and practices. In performing our work, we reviewed key documents related to the systems and practices selected for examination. We also selected and tested samples in our examination of acquisitions and deaccessions, conservation treatments, exhibitions, and public programs.

We did not examine the quality of the conservation treatments that the corporation’s employees applied to objects, nor did we test the quality of environmental reports.

In carrying out the special examination, we did not rely on any internal audits.

The systems and practices selected for examination for each area of the audit are found in the exhibits throughout the report.

Sources of criteria

The criteria used to assess the systems and practices selected for examination are found in the exhibits throughout the report.

Corporate governance

Practice Guide: Assessing Organizational Governance in the Public Sector, The Institute of Internal Auditors, 2014

Corporate Bylaw numberNo. 1, Canadian Museum of History, 2017

Strategic planning

Guidance for Crown Corporations on Preparing Corporate Plans and Budgets, Treasury Board of Canada Secretariat, 2019

Recommended Practice Guideline 3, Reporting Service Performance Information, International Public Sector Accounting Standards Board, 2015

2021–22 to 2025–26 and 2022–23 to 2026–27 corporate plans, Canadian Museum of History

Financial Administration Act

Museums Act

Risk management

Enterprise Risk Management—Integrating with Strategy and Performance: Executive Summary, Committee of Sponsoring Organizations of the Treadway Commission, 2017

Internal Control—Integrated Framework, Committee of Sponsoring Organizations of the Treadway Commission, 2013

2021–22 to 2025–26 and 2022–23 to 2026–27 corporate plans, Canadian Museum of History

International Organization for StandardizationISO 31000—Risk Management—Principles and Guidelines, International Organization for Standardization, 2009

Collections management

Internal Control—Integrated Framework, Committee of Sponsoring Organizations of the Treadway Commission, 2013

Control Objectives for Information and related TechnologyCOBIT 5 Framework—APO05 (Manage Portfolio), BAI01 (Manage Programmes and Projects), EDM02 (Ensure Benefits Delivery), Information Systems Audit and Control AssociationISACA

Research Strategy, Canadian Museum of Civilization, 2013

Collections Development Plan, Canadian Museum of History, 2016

Acquisition and Deaccession Process, Canadian Museum of History, 2014

Collection Management Policy at Canadian Museum of Civilization Corporation, 2006

Museums Act

Research

COBIT 5 Framework—APO05 (Manage Portfolio), BAI01 (Manage Programmes and Projects), EDM02 (Ensure Benefits Delivery), ISACA

Internal Control—Integrated Framework, Committee of Sponsoring Organizations of the Treadway Commission, 2013

Research Strategy, Canadian Museum of Civilization, 2013

Canadian Museum of Civilization Research Policy, 1988

Museums Act

Exhibitions and public programs

COBIT 5 Framework—APO05 (Manage Portfolio), BAI01 (Manage Programmes and Projects), EDM02 (Ensure Benefits Delivery), ISACA

Internal Control—Integrated Framework, Committee of Sponsoring Organizations of the Treadway Commission, 2013

Research Strategy, Canadian Museum of Civilization, 2013

Experience Development Process, Canadian Museum of History, 2014

Public Programs Procedure Manual, Canadian Museum of Civilization, 2012

Exhibitions Policy, Canadian Museum of Civilization, 2003

Museums Act

Period covered by the audit

The special examination covered the period between 1 January 2022 and 31 October 2022. This is the period to which the audit conclusion applies. However, to gain a more complete understanding of the significant systems and practices, we also examined certain matters that preceded the starting date of this period, including exhibitions, programming, and deaccessions covering the period from 1 October 2021.

Date of the report

We obtained sufficient and appropriate audit evidence on which to base our conclusion on 21 April 2023, in Ottawa, Canada.

Audit team

This special examination was completed by a multidisciplinary team from across the Office of the Auditor General of Canada led by Dusan Duvnjak, Principal. The principal has overall responsibility for audit quality, including conducting the audit in accordance with professional standards, applicable legal and regulatory requirements, and the office’s policies and system of quality management.

List of Recommendations

The following table lists the recommendations and responses found in this report. The paragraph number preceding the recommendation indicates the location of the recommendation in the report.

| Recommendation | Response |

|---|---|

|

21. The corporation should establish a code of conduct for its board members. The corporation should also ensure that board members and employees periodically declare their understanding of and commitment to comply with ethical and conflict‑of‑interest requirements and to adhere to the corporation’s values. |

Agreed. The corporation has drafted a code of conduct for board members and will adopt it in early 2023–24. The corporation will implement a yearly commitment on the part of board members and employees to ethical and conflict of interest requirements and adherence to the corporation’s values. |

|

26. Upon comprehensively reviewing and updating its policies, management should provide the board with the information necessary to overseeing the corporation’s compliance with its policies. |

Agreed. The corporation has developed a Corporate Policy Renewal Framework and is undertaking a comprehensive review and update of its policies. In 2023–24, the corporation will inaugurate a yearly compliance report to assist the board in monitoring the corporation’s compliance with corporate policies. |

|

31. The corporation should set clear performance indicators and targets for the priorities and key activities presented in its corporate plans. It should report regularly to the board on their achievement and include this information in its annual report. |

Agreed. In 2023–24, the corporation will renew its Performance Measurement Framework and performance reports to the board and to the senior leadership team, so that clear performance indicators are monitored against milestones. The corporation will continue to report on performance quarterly to the board and include results in the annual report. |

|

35. The corporation should further define its mitigation strategies and develop risk appetite statements and risk tolerances, and specific action plans. Implementation of those action plans and any associated target dates should be reported in the corporate risk profile to both senior management and the board. |

Agreed. In 2023–24, the corporation will develop risk appetite statements and risk tolerances. It will develop more robust mitigation strategies and specific action plans for its corporate risks and report on them quarterly to the senior leadership team and the board. |

|

53. The corporation should ensure that work plans include enough detail to communicate expectations of employees. This includes setting clear performance indicators and targets. The corporation should use these indicators to systematically monitor operational progress and report on its achievement. |

Agreed. The corporation is currently reviewing its work planning processes and in 2023–24 will launch a renewed process for the 2024–25 work planning exercise. The corporation will standardize the level of work details and the type of performance indicators required for approval and monitoring by management, and will use the work plans as a basis for approving projects and monitoring and reporting on operational progress. |

|

59. The corporation should ensure that it meets its standards for processing acquisitions and deaccessions. Furthermore, given the lack of clarity on the resolution of challenges identified in the Collections Development Plan that spans the 2016–2026 period, the corporation should review this plan, develop appropriate action plans, and systematically monitor the progress of their implementation. |

Agreed. In 2023–24, the corporation will review and reissue standards for processing acquisitions and deaccessions, better tailored to the various types of acquisitions and deaccessions, and will put in place an effective monitoring and reporting regime. The corporation will review and update the Collections Development Plan in 2024–25 and institute action plans to address identified challenges, with quarterly reporting to senior leadership. |

|

68. The corporation should identify specific review and approval steps in its processes for the conservation treatments of its artifacts and should monitor to ensure that employees comply with these steps. |

Agreed. In 2023–24, the corporation will develop specific review and approval steps for artifact conservation, clearly defining the authorizations required for different levels of treatment. The corporation will put in place an effective monitoring and reporting regime by 31 March 2024. |

|

69. The corporation should update its collections inventory management process for both museums and ensure that appropriate, time‑bound action plans are developed to address identified issues. |

Agreed. In 2023–24, the corporation will review and update inventory management procedures for its collections. The corporation will also develop action plans with reasonable timelines to address already identified issues, as well as issues identified in future inventory verifications, by 31 March 2024. |

|

70. The corporation should regularly and systematically review all granted access permissions. |

Agreed. In 2023–24, the corporation will renew access protocols and will review permission lists regularly, ensuring that the security database reflects appropriate access controls. It will continue to modernize its security infrastructure to enhance reporting and tracking of access permissions, with the access control portion completed by 31 March 2024. |

|

74. The corporation should develop formal documented processes and templates to help researchers understand corporate expectations and to help managers ensure that those expectations are met. |

Agreed. The corporation is updating its Research Policy and when approved in 2023–24, the policy will provide clarity on research processes and corporate expectations for research. In 2023–24, the corporation will implement the consistent use of research project proposals and tracking templates. These tools will formalize approvals to ensure alignment with corporate priorities and track deliverables against key milestones. |

|

79. The corporation should update its formal processes and guidelines for developing and delivering exhibitions and public programs and then monitor to ensure that key requirements are being followed. |

Agreed. The corporation will review and modernize its formal processes and guidelines for developing exhibitions and public programs. This modernization will include an updated monitoring approach to ensure that requirements are being followed, and will be implemented in 2024–25. |