Report of the Auditor General of Canada to the Board of Directors of the Royal Canadian Mint—Special Examination—2023

Independent Auditor’s Report

Table of Contents

- Audit Summary

- Introduction

- Findings, Recommendations, and Responses

- Conclusion

- About the Audit

- List of Recommendations

- Exhibits:

- 1—Flow of domestic coins, from production to circulation

- 2—As Canadians transitioned to using less cash, the supply of coins in Canada declined

- 3—The corporation’s facilities in Ottawa and Winnipeg

- 4—Corporate governance—Key findings and assessment

- 5—Strategic planning—Key findings and assessment

- 6—Corporate risk management—Key findings and assessment

- 7—The corporation’s gross revenue by business line from 2018 to 2022

- 8—In addition to manufacturing Canadian and foreign circulation coins, the corporation works with precious metals, including bullion products and services, and numismatics (collectible coins, tokens, and medals)

- 9—Operations—Key findings and assessment

- 10—Environment and sustainable development—Key findings and assessment

- 11—Security—Key findings and assessment

- 12—Human resource management—Key findings and assessment

- 13—Organizational and digital transformation—Key findings and assessment

Audit Summary

We found no significant deficiencies in the corporate management practices or in the management of operations and the organizational and digital transformation of the Royal Canadian Mint during the period covered by the audit. However, we found that improvement was needed in the areas of corporate risk management, the environment and sustainable development, information security, and human resource management, as well as in systems and practices related to the corporation’s organizational and digital transformation. Despite these weaknesses, the corporation reasonably maintained the systems and practices that we examined to carry out its mandate.

Introduction

Background

1. The Royal Canadian Mint is a Crown corporation owned solely by the Government of Canada. The Royal Canadian Mint Act mandates the corporation to mint coins in anticipation of profit and carry out other related activities.

2. The corporation’s core responsibility is to manage Canada’s circulation coin life cycle—that is, to produce, redistribute, and recycle the coins that Canadian people and businesses use, thereby supporting the smooth operation of the country’s economy (Exhibit 1). Other activities of the corporation involve manufacturing collectible and commemorative coins and medals, investment products made of precious metals, and some other countries’ circulation coins. By using precious metals in its products, the corporation supports both the Canadian and international mining and financial industries. Its coins and medals celebrate Canadian culture and honour Canadians and their achievements.

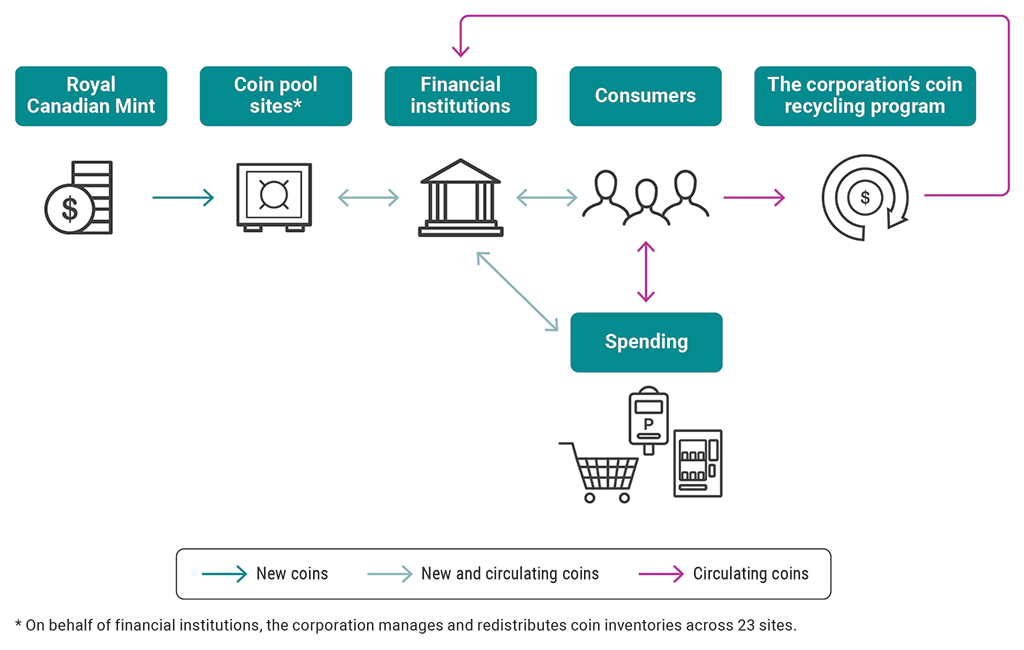

Exhibit 1—Flow of domestic coins, from production to circulation

Source: Adapted from information provided by the Royal Canadian Mint

Exhibit 1—text version

This chart shows the flow of both new and circulating domestic coins in Canada, starting when new coins are produced at the Royal Canadian Mint to when coins are spent by consumers or recycled.

New coins are produced by the Royal Canadian Mint and are distributed to 23 coin pool sites across the country where coins are stored until needed by financial institutions. On behalf of financial institutions, the corporation manages and redistributes coin inventories across the 23 sites. From these sites, both new and existing coins are sent to and received from financial institutions.

Financial institutions purchase these coins to support trade and commerce so that their clients, such as businesses or individual consumers, can withdraw coins for use.

Businesses require coins to make change when consumers purchase goods and services. Businesses withdraw and deposit coins using their financial institutions as needed.

Consumers withdraw coins from financial institutions and use coins in a variety of ways. They

- spend their money at retailers, parking, vending machines, or other

- deposit coins at their financial institutions

- recycle coins at kiosks

Coins are used in many ways and flow back to financial institutions to be used again, forming a continuous loop of withdrawals and deposits.

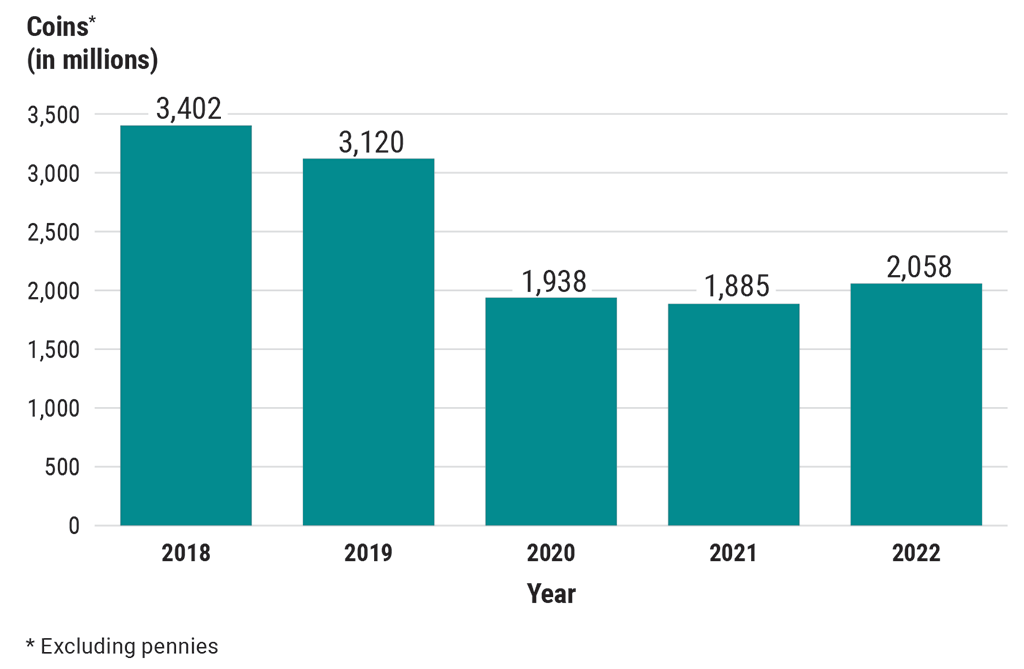

3. Several broad societal and economic factors affect the corporation’s business. For example, evolving payment systems and global events such as the coronavirus disease (COVID‑19)Definition 1 pandemic have accelerated the transition to a cash‑light society, gradually reducing the use of coins or banknotes (Exhibit 2). Conversely, economic instability and recent geopolitical events have increased the demand for bullion—that is, coins and bars of precious metals refined to a high degree of purity and held for investment purposes. While dealing with these changes, the corporation has reiterated the importance of managing the coin supply to facilitate trade and commerce and to ensure financial inclusion for all Canadians.

Exhibit 2—As Canadians transitioned to using less cash, the supply of coins in Canada declined

Source: Based on data in the Royal Canadian Mint’s annual reports

Exhibit 2—text version

This bar chart shows the supply of coins in millions in Canada from 2018 to 2022. Pennies were excluded from the totals. The largest decrease in the supply of coins in Canada was from 2019 to 2020, after which supply remained at reduced levels, increasing only slightly in 2022.

In 2018, there were 3,402 million coins in Canada.

In 2019, there were 3,120 million coins in Canada.

In 2020, the number of coins in Canada decreased significantly to 1,938 million.

In 2021, the number of coins in Canada decreased again to 1,885 million.

In 2022, the number of coins in Canada increased slightly to 2,058 million.

4. The corporation explicitly recognized the changing market conditions when it launched its One Mint strategy in 2020, as articulated in its corporate plan. The strategy is an organizational transformation supported by a digital transformation program; environmental, social, and governance commitments; and a people strategy focusing on diversity, equity, and inclusion and on health and safety. More information on the strategy can be found later in the report in the section on organizational and digital transformation.

5. The corporation has facilities in Ottawa and Winnipeg (Exhibit 3). The majority of the corporation’s approximately 1,200 employees work in manufacturing operations. More information regarding the corporation’s operations can be found in the section of our report on management of operations.

Exhibit 3—The corporation’s facilities in Ottawa (left) and Winnipeg (right)

Photos: Royal Canadian Mint

Focus of the audit

6. Our objective for this audit was to determine whether the systems and practices we selected for examination at the Royal Canadian Mint were providing it with reasonable assurance that its assets were safeguarded and controlled, its resources were managed economically and efficiently, and its operations were carried out effectively, as required by section 138 of the Financial Administration Act.

7. In addition, section 139 of the Financial Administration Act requires that we state an opinion, with respect to the criteria established in subsection 138(3), on whether there was reasonable assurance that there were no significant deficiencies in the systems and practices we examined. We define and report significant deficiencies when, in our opinion, the corporation could be prevented from having reasonable assurance that its assets are safeguarded and controlled, its resources are managed economically and efficiently, and its operations are carried out effectively.

8. On the basis of our risk assessment, we selected systems and practices in the following areas:

The selected systems and practices, and the criteria used to assess them, are found in the exhibits throughout the report.

9. More details about the audit objective, scope, approach, and sources of criteria are in About the Audit at the end of this report.

Findings, Recommendations, and Responses

Corporate management practices

The corporation had good corporate management practices, but an improvement was needed in corporate risk management

10. We found that the corporation had good corporate management practices. However, an improvement was needed in risk mitigation.

11. The analysis supporting this finding discusses the following topics:

12. The corporation is governed by its Board of Directors, consisting of 9 to 11 members. They include the Chair of the Board as well as the President and Chief Executive Officer, who are appointed and whose terms of office are defined by the Governor in CouncilDefinition 2. The other directors are appointed by the Minister of Finance with the approval of the Governor in Council, and they hold office for a term not exceeding 4 years. All board members are eligible for reappointment when their terms expire. At the end of our examination period, there were 9 appointed board members and 2 vacant positions.

13. Five of the board members’ terms will expire in December 2026. The Royal Canadian Mint Act states that, as far as possible, not more than half of the directors’ terms should expire in any single year. If many directors were to be replaced within a short time frame, continuity and corporate memory could be affected. Significant turnover within a short time could also reduce the board’s ability to exercise effective oversight. We encourage the corporation to continue working with the Minister of Finance to ensure that appropriate appointments to the board are timely and staggered.

14. The corporate strategy and objectives derive from the corporation’s strategic planning processes, which include annual strategic retreats by senior management (the President and Chief Executive Officer and the vice‑presidents) and board members. The corporation prepares a long‑term strategic plan every 10 years. Every 3 years, it reviews its strategic plan, mission, vision, and corporate objectives to ensure that they are still in line with expectations. It then develops a 3- to 5‑year plan, which is set out annually in the corporate plan. Each year, the corporation also updates its corporate objectives as it deems necessary. As part of this long‑term strategic planning process, the corporation established its One Mint strategy in 2020, launching the corporation’s organizational transformation.

15. Our recommendation in this area of examination appears at paragraph 21.

16. Analysis. We found that the corporation had good systems and practices for corporate governance (Exhibit 4).

Exhibit 4—Corporate governance—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Board independence |

The board functioned independently. |

The board made decisions independently of senior management and held regular private meetings without senior management in attendance. Board members declared conflicts of interest at board meetings and in annual letters and third-party disclosure forms. The corporation had a code of conduct and ethics that stated corporate values and expected behaviours. This code was applicable to board members. |

Check mark in a green circle |

|

Providing strategic direction |

The board provided strategic direction. |

The corporation’s strategic objectives were clearly linked to the legislative mandate and public policy mandate and were reflected in the corporate plan. The board provided strategic direction through its annual strategic planning session and by approving the strategic direction in the corporate plan. The board was active in setting annual objectives for the President and Chief Executive Officer. It conducted an annual assessment of performance against those objectives. |

Check mark in a green circle |

|

Board appointments and competencies |

The board collectively had the capacity and competencies to fulfill its responsibilities. |

The board had a process for members to perform a self‑evaluation of their skills, knowledge, and expertise. The board communicated with the responsible minister about board appointments, renewals, and vacancies. The corporation had an orientation program for new members. Board members were provided ongoing training. |

Check mark in a green circle |

|

Board oversight |

The board carried out its oversight role over the corporation. |

The board regularly discussed the corporation’s financial status, corporate risk profile, and progress against strategic targets, including the progress of major projects. The corporation’s internal audit function provided an independent, objective view on risk and internal controls. This helped the board exercise its oversight and monitoring responsibilities. The board annually evaluated its performance and that of its committees, individual directors, and the Chair. |

Check mark in a green circle |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

17. Analysis. We found that the corporation had good systems and practices for strategic planning (Exhibit 5).

Exhibit 5—Strategic planning—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Strategic planning |

The corporation established a strategic plan and strategic objectives that aligned with its mandate. |

The corporation defined a strategic direction that aligned with its mandate in its enabling legislation. The corporation took into consideration its internal and external environments when preparing its corporate plan. The corporation had a strategic planning process in place, which included analyzing its strengths, weaknesses, and opportunities, as well as key risks and threats. |

Check mark in a green circle |

|

Performance measurement, monitoring, and reporting |

The corporation established performance indicators in support of achieving its strategic objectives, and monitored and reported on its progress against these indicators. |

The corporation established performance indicators and targets to assess ongoing progress in achieving strategic objectives. The corporation reported performance results quarterly to senior management and the board. The corporation published its key achievements related to strategic objectives in its annual report and held an annual public meeting. |

Check mark in a green circle |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

18. Analysis. We found that the corporation had good systems and practices for risk management. However, improvements were needed in risk mitigation (Exhibit 6).

Exhibit 6—Corporate risk management—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Risk identification and assessment |

The corporation identified and assessed risks to achieving its strategic objectives. |

The corporation had an enterprise risk management framework. The corporation identified its functional and strategic risks, and assigned residual risk ratings to them according to the likelihood of their occurrence and the potential impact. The corporation provided quarterly updates to the board on its strategic risk profile. |

Check mark in a green circle |

|

Risk mitigation |

The corporation defined and implemented risk mitigation measures. |

The corporation established mitigating controls and actions for functional and strategic risks. The corporation had a risk appetite statement in place for its key risk categories. This set risk tolerances and provided guidance for the development of mitigation strategies. Weakness The corporation did not establish clear timelines for the majority of the mitigating actions in its functional risk registers. |

Exclamation point in a yellow circle |

|

Risk monitoring and reporting |

The corporation monitored and reported on the implementation of risk mitigation measures. |

The corporation monitored emerging risks and updated risk registers when required. The corporation reported on risk management activities through detailed quarterly reports to the board. These included a description of the strategic risks, as well as an update on mitigating actions and emerging risks. |

Check mark in a green circle |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

19. Weakness—Risk mitigation. We found that the corporation did not establish clear timelines for the majority of the mitigating actions in its functional risk registers. For example, the corporation had identified its ability to attract and retain talent as a risk, and determined that establishing a succession plan would mitigate that risk. This was particularly important because of the changes in the labour market stemming from the COVID‑19 pandemic. However, there was no set timeline for implementation of the succession plan.

20. This weakness matters because without clear timelines for mitigating actions, it is difficult for senior management to determine whether the corporation is making timely progress toward achieving its risk mitigation strategies.

21. Recommendation. The corporation should ensure that its risk mitigation actions have timelines that allow for measurement of progress against them.

The corporation’s response. Agreed. At the end of 2022, the corporation commenced the documentation of timelines for mitigation plans of functional risks, which will be completed by the end of 2023.

Management of operations

The corporation generally managed its operations well, but improvements were needed

22. We found that the corporation generally managed its activities well in the areas of operations, environment and sustainable development, security, and human resources. However, improvements were needed in operational plan implementation, environment and sustainable development, information security, and human resource management.

23. The analysis supporting this finding discusses the following topics:

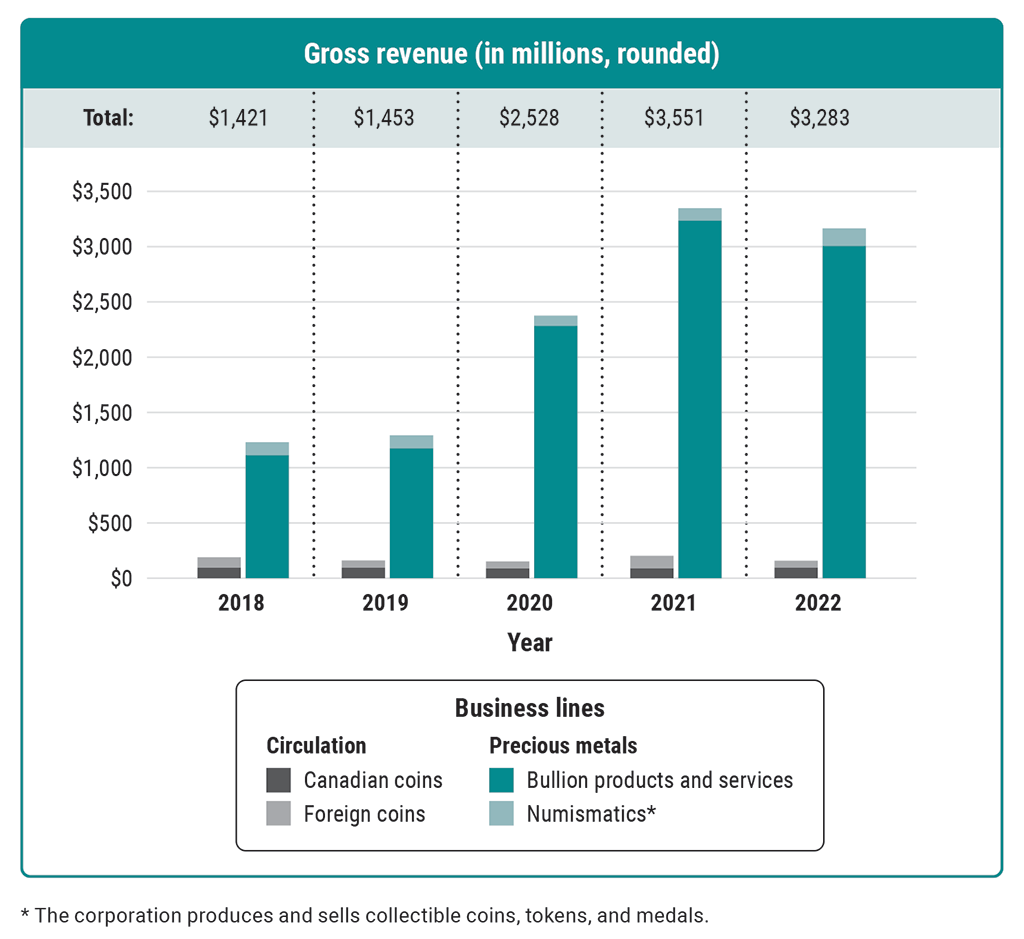

24. The corporation has 2 business lines: circulation and precious metals (exhibits 7 and 8). The circulation business line is based at the corporation’s Winnipeg facility and involves manufacturing both Canadian and foreign coins. The precious metals business line includes bullion products and services, as well as numismatics. It is based at the corporation’s Ottawa facility.

Exhibit 7—The corporation’s gross revenue by business line from 2018 to 2022

Source: Based on information in the Royal Canadian Mint’s annual reports

Exhibit 7—text version

This bar chart shows the corporation’s gross revenue in millions (rounded) from its 2 business lines from 2018 to 2022. The circulation business line comprises Canadian and foreign circulation businesses. The precious metals business line comprises bullion products and services and the numismatics business (collectible coins, tokens and medals).

Gross revenue from the circulation business line remained steady over the 5‑year period, but the gross revenue from the precious metals business line increased significantly from 2019 to 2021 and declined slightly in 2022. Bullion products and services drove the increases.

In 2018, the total gross revenue from both business lines was $1,421 million. The gross revenue from Canadian circulation was $95 million and from foreign circulation was $95 million. Under precious metals, gross revenue from bullion products and services was $1,114 million and from numismatics was $117 million.

In 2019, the total gross revenue from both business lines was $1,453 million. The gross revenue from Canadian circulation was $95 million and from foreign circulation was $65 million. Under precious metals, the gross revenue from bullion products and services was $1,176 million and from numismatics was $117 million.

In 2020, the total gross revenue from both business lines increased significantly to $2,528 million. The gross revenue from Canadian circulation was $88 million and from foreign circulation was $64 million. Under precious metals, the gross revenue from bullion products and services was $2,284 million (a significant increase) and from numismatics was $92 million.

In 2021, the total gross revenue from both business lines increased to $3,551 million. The gross revenue from Canadian circulation was $90 million and from foreign circulation was $113 million. Under precious metals, the gross revenue from bullion products and services was $3,236 million (another substantial increase) and from numismatics was $112 million.

In 2022, the total gross revenue from both business lines decreased slightly to $3,283 million. The gross revenue from Canadian circulation was $96 million and from foreign circulation was $63 million. Under precious metals, the gross revenue from bullion products and services was $3,007 million (a slight decrease) and from numismatics was $158 million.

Exhibit 8—In addition to manufacturing Canadian and foreign circulation coins, the corporation works with precious metals, including bullion products and services, and numismatics (collectible coins, tokens, and medals)

Photos: Royal Canadian Mint

25. Canadian circulation. The corporation manages Canada’s coin life cycle, including monitoring and forecasting coin use, producing coins, managing inventory, and recirculating and recycling coins. In a memorandum of understanding covering 2022 to 2025, the Department of Finance Canada agreed to pay a fee to the corporation for conducting these activities. The corporation works with partners, such as the National Coin Committee and the Bank of Canada, to maintain its coin life cycle management practices. The corporation also advises the federal government on trends and scenario planning to help Canada prepare for possible market disruptions affecting coin supply and demand.

26. Foreign circulation. The corporation also uses its expertise and manufacturing capacity to produce coins for other countries. The corporation manages the production of Canadian and foreign demand to prevent domestic coin shortages. The purpose of this approach is to help the corporation optimize the use of its assets and resources.

27. Bullion products and services. The corporation produces coins, bars, and wafers of precious metals for purchase by investors. The corporation also provides related services: refining gold and silver, assaying (that is, testing bullion for fineness or purity), and offering secure storage.

28. Numismatics. The corporation produces and sells collectible coins, tokens, and medals.

29. Both the circulation and precious metals business lines are supported by the corporation’s innovation and digital technology programs, its people strategy, and its environmental, social, and governance commitments. For example, in keeping with its environmental, social, and governance goals, the corporation has committed to reviewing the recycling of existing coins, and to introducing socially and environmentally responsible products, services, and processes. The corporation has also committed to building an inclusive and diverse workforce.

30. Our recommendations in this area of examination appear at paragraphs 34, 39, 43, 46, 51, 54, and 57.

31. Analysis. We found that the corporation had good systems and practices for managing the operations of its 2 business lines, but there was room for improvement in implementing the operational plan for its foreign circulation component (Exhibit 9).

Exhibit 9—Operations—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Operational planning |

The corporation’s operational planning aligned with the strategic objectives. |

Operational plans aligned with the corporation’s strategic plans and mandate. Operational plans considered the business risks and identified those responsible for the implementation and monitoring of projects. |

Check mark in a green circle |

|

Operational plan implementation |

The corporation implemented its operational plans to deliver results in accordance with the expected outputs. |

The corporation had a framework established to effectively manage the domestic life cycle of coins. The corporation’s process for product development gave careful consideration to diversity, equity, and inclusion. The corporation had processes and accreditations in place to ensure that its precious metals were sourced, refined, and stored responsibly. The corporation had policies and processes in place to frequently assess, monitor, and report on its exposure to volatility in the pricing of precious metals. Weakness The corporation did not establish mitigating strategies to address the risks associated with long‑term trends in demand for foreign circulation coins. |

Exclamation point in a yellow circle |

|

Operational performance measurement, monitoring, and reporting |

The corporation established performance indicators to measure its operational performance, and monitored and reported on progress. |

The corporation regularly reported on the operational and financial performance of its circulation and precious metals business lines to senior management, the board, and key stakeholders. Senior management regularly monitored the corporation’s key performance indicators for its manufacturing and refinery operations, including indicators of process productivity and efficiency. Senior management regularly reported to the board on the progress of operationalizing the corporation’s strategic plan. |

Check mark in a green circle |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

32. Weakness—Operational plan implementation. The foreign circulation business is historically a highly competitive market. Furthermore, it has been negatively affected by geopolitical events and economic instability since the COVID‑19 pandemic. Recognizing the unpredictable impacts of these events, management performed detailed market studies to update its foreign sales strategy, and monitored risks and performance of its foreign business. However, we noted that for 2021 and 2022, the corporation did not meet all of its targets for foreign circulation revenue, contribution margin, and the efficiency of its Winnipeg plant. Although the corporation reacted by implementing some efficiency initiatives in 2022, we found that it did not establish mitigating strategies to address long‑term trends in demand for foreign coins, despite the risks and uncertainty over the performance of the foreign circulation business.

33. This weakness matters because foreign sales performance has a direct effect on the Winnipeg plant’s efficiency. The plant’s resource planning is closely related to foreign sales forecasts, particularly because the same employees at the Winnipeg plant are scheduled on both domestic and foreign coin production. Without establishing mitigating strategies to manage the risks associated with long‑term trends in demand for foreign circulation coins, the corporation could not optimize the use of its resources in a timely manner.

34. Recommendation. To optimize the efficiency of its Winnipeg plant, the corporation should establish mitigating strategies in response to long‑term trends in demand for foreign circulation coins.

The corporation’s response. Agreed. By the end of 2024, as part of its next strategic plan, the corporation will develop an action plan that would allow it to respond to the risks associated with long‑term trends of foreign circulation and optimize the use of its resources in a timely manner.

35. Analysis. We found that the corporation had good systems and practices for the environment and sustainable development, but needed to make improvements in its monitoring and reporting (Exhibit 10).

Exhibit 10—Environment and sustainable development—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Environment and sustainable development |

The corporation had processes in place to manage, periodically review, and report on its environmental performance, and to implement timely corrective actions. |

The corporation had an environmental management system, which it defined in its policies, manuals, and guidelines. The corporation established its environmental, social, and governance commitments and roadmap. Weakness Although senior management received information and monitored the performance of the corporation’s environmental management system, only limited information reached the board. |

Exclamation point in a yellow circle |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

36. Weakness—Environment and sustainable development. The goal of an environmental management system is to establish systems and practices that enable the corporation to achieve its environmental objectives by consistently reviewing, evaluating, and improving its environmental performance. Although senior management received information and monitored the performance of the corporation’s environmental management system, we found that only limited information reached the board.

37. We also noted that the corporation had not yet comprehensively assessed how its environmental, social, and governance program and related commitments would contribute to achieving the United Nations’ Sustainable Development Goals. The government established formal expectations for federal departments and agencies to integrate the Sustainable Development Goals into their operations. We recognize that the government did not establish similar expectations for Crown corporations. However, in our view, the Sustainable Development Goals offer a framework for organizations, including Crown corporations, to identify and contribute to social, economic, and environmental initiatives.

38. This weakness matters because environmental, social, and governance commitments are part of the corporation’s corporate objectives. In our view, performance information on the corporation’s environmental activities would help the board exercise its oversight role, especially as progress in this area is rapidly becoming part of the government’s expectations for all federal organizations.

39. Recommendation. The corporation should provide the board with comprehensive reporting on the performance of its environmental management system.

The corporation’s response. Agreed. The corporation will report its environmental performance, which includes environmental management system information, annually to the board beginning in 2024. Furthermore, since the beginning of 2023, the corporation has improved the documentation of the explicit links between its environmental, social, and governance initiatives and the United Nations’ Sustainable Development Goals, and will continue to develop these linkages with the corporation’s other activities and programs.

40. Analysis. We found that the corporation had good systems and practices related to security. However, improvements were needed in information security (Exhibit 11).

Exhibit 11—Security—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Information security |

The corporation had an information security management program to protect the confidentiality, integrity, and availability of information assets, and to prevent, detect, and respond to security breaches. |

The corporation established cybersecurity policies, directives, and procedures. These included roles and responsibilities, an awareness program, threat and risk assessments, and an incident response plan. Weaknesses The corporation did not have an information management and data governance policy, framework, or program that supported information and data security objectives. The corporation did not maintain a centralized list of third-party providers that had access to its information assets. It did not conduct a cybersecurity risk assessment of several service providers. |

Exclamation point in a yellow circle |

|

Physical security |

The corporation had systems and practices in place to safeguard and control precious metals. |

The corporation had controls to safeguard precious metals in its possession. The corporation’s processes for determining the quantity and valuation of its precious metals included continuous monitoring, and reporting to the board and the Minister of Finance. External consultants regularly assessed the processes. |

Check mark in a green circle |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

41. Weakness—Information security (information management and data governance). We found that the corporation did not have an information management and data governance policy, framework, or program that supported information and data security objectives. We also found that without a policy and directives in place, employees exercised their own discretion to determine the measures for protecting and managing the corporation’s information and data assets. The corporation’s internal audit function and the assessments conducted by third parties provided similar observations in 4 separate reports since 2015.

42. This weakness matters because employees responsible for protecting confidentiality and safeguarding the corporation’s information and data need guidance to ensure that decisions related to information security are consistent and appropriate to the level of sensitivity of the information. Moreover, because such policies and programs were not in place before the launch of the digital transformation, there was a risk that information and data security controls would not be integrated efficiently into existing or new infrastructure and platforms.

43. Recommendation. The corporation should develop and implement a comprehensive information management and data governance policy, framework, and program to support information and data security objectives.

The corporation’s response. Agreed. The corporation has prioritized its Information Management and Data Governance program to begin in 2023. Implementing information management classification is a critical next step, which the corporation will also integrate with its the overall Information Management strategy. The corporation will develop and implement its information management and data governance policies, frameworks, and programs by the end of 2025.

44. Weakness—Information security (cybersecurity and third parties). The corporation hires third-party service providers to support various aspects of its operations, including human resources and finance. To perform their work, the third-party service providers might have access to information or data assets considered to be of key importance to the corporation. We found that the corporation did not maintain a centralized list of its third-party service providers that had access to its information and data assets, and did not conduct a comprehensive cybersecurity risk assessment of several service providers.

45. This weakness matters because if the cybersecurity of third-party service providers is compromised, the corporation’s information and data assets that those service providers can access may also be compromised. Without consistently conducting cybersecurity risk assessments of third-party service providers, the corporation cannot know the extent of exposure and cybersecurity risks related to its information and data assets.

46. Recommendation. The corporation should maintain a centralized list and perform regular cybersecurity risk assessment of all third-party service providers that have access to its information and data assets.

The corporation’s response. Agreed. The corporation recognizes the importance of vendor management. The corporation will establish a centralized list of third-party service providers by the end of 2023. The corporation will also enhance our cyber security program to cover all third-party service providers that have access to our information and data set between now and the end of 2025.

47. Analysis. We found that the corporation needed improvements in human resource management in the areas of workplace health and safety, as well as in workforce and succession planning (Exhibit 12).

Exhibit 12—Human resource management—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Human resource management |

The corporation established a comprehensive workforce plan, which was aligned to the strategic plan and corporate priorities. |

The corporation established a short-term workforce plan. The corporation had a workforce planning process, which mainly assessed short-term priorities, from various business areas to staffing needs, while considering the overall corporate budget. The corporation performed analyses of the gaps between its existing skills and its needs. Weaknesses The corporation did not perform workforce planning beyond 12 months. The corporation did not implement a comprehensive succession planning process across the organization. |

Exclamation point in a yellow circle |

|

The corporation had a recruitment and retention framework in place that enabled it to attract and retain the people it needed to meet the strategic and operational objectives. |

The corporation established and monitored key performance measures regarding recruitment, retention, and learning and development. The corporation performed salary benchmarking in support of its recruitment and retention processes. The corporation established learning and development plans. The corporation considered diversity, equity, and inclusion in its recruitment and retention processes. |

Check mark in a green circle | |

|

The corporation established a healthy and safe workplace. |

The corporation had health and safety policies, procedures, and programs. These dealt with physical and mental health, radiation safety, and emergency preparedness and response. The corporation prepared a health and safety dashboard, with key performance indicators. Senior management and the board monitored the dashboard regularly. The corporation had processes to investigate and report on incidents and to implement corrective actions and monitor their status. Weakness Individuals required to be trained for hazardous materials did not meet all of the training requirements set out by the corporation. |

Exclamation point in a yellow circle | |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

48. Weakness—Human resource management (workforce planning). We found that the corporation did not perform long‑term workforce planning to ensure that its needs aligned with its strategic plan and corporate priorities. As a result, the corporation lacked several resources and skills for which it had identified needs. We raised the issue of workforce planning in our 2005 and 2014 special examination reports.

49. As a result of not having a long‑term workforce plan, the corporation did not have sufficient time to respond to ongoing changes in the labour market or to attract, train, and certify people with the right skills. With the number and complexity of initiatives undertaken to achieve the One Mint strategy, the lack of resources with the right skills affected the corporation’s ability to advance some strategic projects and delayed the start of others.

50. This weakness matters because long‑term workforce planning would help the corporation manage its talent pool risk by ensuring that it has the number of employees it needs, along with the necessary skills and experience, to carry out its operations and deliver on its short- to long‑term strategic objectives.

51. Recommendation. The corporation should develop and implement a workforce plan that identifies its future skills and resource needs beyond 12 months.

The corporation’s response. Agreed. Although the corporation’s current workforce planning tools include some data beyond 12 months, the corporation will enhance its workforce planning process with a focus beyond 12 months, beginning in 2024. The competitive labour market may continue to impact the corporation’s ability to attract talent in certain areas.

52. Weakness—Human resource management (succession planning). In view of its unique and complex operations, the corporation requires highly trained and specialized staff at all levels. However, we found that the corporation had not implemented a comprehensive succession planning process across the organization. Furthermore, although the corporation had identified key positions and some successors for directors and senior management positions, the list of successors was not comprehensive and the corporation had not consistently implemented development plans for potential successors.

53. This weakness matters because the corporation’s long‑term success and ability to mitigate its talent pool risk depends on determining key positions that require critical skills and competencies, identifying potential successors, and implementing development plans or recruitment strategies.

54. Recommendation. The corporation should develop an organization-wide succession planning process and ensure that related development plans or recruitment strategies are in place for key positions.

The corporation’s response. Agreed. As it develops a more comprehensive succession planning process, to be implemented by the end of 2024, the corporation will identify and develop successors for key positions among current employees and through targeted external recruitment, where necessary.

55. Weakness—Human resource management (workplace health and safety). We found that individuals required to be trained for hazardous materials did not meet all of the training requirements set out by the corporation. Although most of the individuals required to have the hazardous materials training met the requirements by the end of 2022, this was not the case for the entire period covered by the audit. We also found that the corporation lacked an effective process for scheduling, delivering, and monitoring health and safety training.

56. This weakness matters because lives depend on workplace safety. Health and safety risks are elevated in the corporation’s manufacturing facilities, which are more likely to be subject to hazardous materials incidents. Furthermore, without effective processes to schedule, deliver, and monitor health and safety training, the corporation could not be sure that individuals working in manufacturing facilities were trained in a timely manner.

57. Recommendation. The corporation should implement an effective process for scheduling, delivering, and monitoring health and safety training, with the aim of ensuring that all individuals required to have hazardous materials training receive the training in a timely manner.

The corporation’s response. Agreed. Hazardous materials training is 1 element of the emergency management program. Although COVID‑19 created challenges to delivering hazardous materials training in a timely manner, the corporation was able to respond to incidents.

By the end of 2023, the corporation will implement an improved process for scheduling, delivering and monitoring health and safety training.

Organizational and digital transformation

The corporation had good systems and practices for managing its transformation, but improvements were needed

58. We found that the corporation had good systems and practices to manage its organizational and digital transformation. However, improvements were needed in the areas of leadership and project oversight, project management, and change management.

59. The analysis supporting this finding discusses the following topic:

60. In 2020, the corporation established its long‑term vision. Through the One Mint strategy, it launched an organizational and digital transformation. Since then, the corporation has been seeking to achieve its goals of increasing integration, efficiency, collaboration, innovation, agility, and resilience throughout its operations. For example, to create more integration and efficiency of similar products and services, the corporation reorganized the business lines under which it operates, consolidating them from 4 to 2. The corporation is also seeking to maximize its agility and innovation through technology investments.

61. In pursuit of its One Mint strategy, the corporation has identified 2 areas of focus for its desired culture: diversity, equity, and inclusion; and health and safety. It also identified other areas of its existing culture (such as collaboration and innovation) that needed to be further developed to ensure the success of the organizational and digital transformation.

62. Information technology supports all of the corporation’s business lines and is critical to meeting strategic and corporate objectives, including the operationalization of the One Mint strategy. To improve operational efficiency and enhance the customer experience, the corporation is undertaking key initiatives such as upgrading its software systems for Enterprise Resource Planning and for Materials Requirements Planning. It is also implementing a new website for customers.

63. Our recommendations in this area of examination appear at paragraphs 67, 70, 73, and 76.

64. Analysis. We found that the corporation’s systems and practices for its organizational and digital transformation needed improvements in leadership and project oversight, project management, and change management (Exhibit 13).

Exhibit 13—Organizational and digital transformation—Key findings and assessment

| Systems and practices | Criteria used | Key findings | Assessment against the criteria |

|---|---|---|---|

|

Leadership and project oversight |

The corporation had the program and project management structure necessary to oversee, monitor, and report on multiple transformational projects. |

The corporation identified leadership sponsors for the transformation and its major projects. The corporation had processes enabling senior management and the board to monitor progress related to its major transformational projects. Under a communications plan, the corporation regularly shared key messages and progress updates with employees about the One Mint strategy. Weakness The corporation’s transformation office had key resource gaps and lacked a defined mandate and structure. |

Exclamation point in a yellow circle |

|

Project management |

The corporation had a project management framework to initiate, plan, execute, and manage its transformational projects (One Mint). The corporation had the practices and processes in place to successfully acquire and develop its information technology systems and manage the delivery of its projects within an acceptable level of risk. |

The corporation prepared dashboards for major projects, for use in reporting to senior management and the board on scope, schedule, resources, and overall progress. The corporation had a methodology to manage the development of its information technology systems. The corporation established a governance structure for its information technology transformation, with clearly defined roles and responsibilities. Weakness The corporation did not have a comprehensive project management framework to enable it to initiate, plan, execute, monitor, and close all its projects effectively. |

Exclamation point in a yellow circle |

|

Change management |

The corporation implemented the changes necessary to evolve the organization, its people, and its culture. |

The corporation had a change management roadmap and strategy for its organizational transformation, and provided some change management training. The corporation had a diversity, equity, and inclusion action plan with defined goals, key activities, and expected outcomes. Weaknesses The corporation did not manage culture change efforts in a coordinated manner, and did not monitor and report on progress toward achieving all aspects of its desired culture. The corporation did not assess its needs in culture change expertise and skills. |

Exclamation point in a yellow circle |

|

Legend—Assessment against the criteria Check mark in a green circle Met the criteria Exclamation point in a yellow circle Met the criteria, with improvement needed An X in a red circle Did not meet the criteria |

|||

65. Weakness—Leadership and project oversight. In 2022, the corporation hired a Chief Transformation Officer. However, at the time of our audit, it had not yet defined the mandate or the structure of its transformation office. We also noted that the transformation office had key resource gaps.

66. This weakness matters because the transformation office has an important role in supporting a large-scale transformation. An established and mature transformation office would ensure that projects and initiatives are managed in a consistent and integrated way that enables the corporation to support and implement widespread change effectively and efficiently.

67. Recommendation. The corporation should allocate sufficient resources and define the mandate and structure for its transformation office.

The corporation’s response. Agreed. Since the end of the examination period, the corporation has restructured its Project Management Office to include the management of the organizational and digital transformations. The new structure harmonizes all project management offices, which play a key role in delivering on transformation projects and initiatives. By the end of 2023, the corporation will formalize the mandate of the Project Management Office.

Since the end of the examination period, the corporation has approved a staffing plan to ensure adequate resourcing of the Project Management Office.

68. Weakness—Project management. We found that the corporation did not have a comprehensive project management framework to support project management practices. For example, although the corporation identified the stages relevant to managing the project life cycle, it did not have a methodology or process for measuring achievement of the desired outcome at each stage or for linking these benefits to the overall achievement of the long‑term vision and strategic goals.

69. This weakness matters because a comprehensive framework supported by methodologies and tools would enable the corporation to initiate, plan, execute, monitor, and close its projects more effectively.

70. Recommendation. The corporation should develop the methodologies and tools needed to make its project management framework more comprehensive.

The corporation’s response. Agreed. Since the end of the examination period, the corporation has approved its Benefits Realization Framework. The framework includes measurable benefits, which are then tracked throughout both the project life cycle and post‑project close‑out by the business owner. This provides an opportunity to use the measurable benefits as target achievements against the One Mint strategy. Furthermore, by the end of 2024, the corporation will complete an assessment to determine additional methodologies and tools to help improve its project management framework with the support of its third-party risk adviser.

71. Weakness—Change management (managing culture change). Senior management and the board acknowledged the importance of culture change as part of the organizational and digital transformation. Senior management monitored and reported to the board on transformation projects and initiatives related to the 2 areas of focus of its desired culture (diversity, equity, and inclusion; and health and safety). However, management did not establish a plan and strategy to comprehensively manage, monitor, and report on the corporation’s culture change efforts. For example, in the effort to achieve the overall desired organizational culture, it was not clear how the corporation considered integrating other aspects of the existing culture, such as collaboration and innovation.

72. This weakness matters because a corporation’s organizational culture has several components that interact and can impact the desired culture outcomes. Without a comprehensive strategy to manage the various components of its desired culture in a coordinated manner, the corporation would not be able to monitor and report on the overall progress and impact of its organizational culture change efforts.

73. Recommendation. The corporation should establish a plan and strategy to manage culture change efforts in a coordinated manner, and should monitor and report on progress made toward all aspects of its desired culture.

The corporation’s response. Agreed. By the end of 2023, as the corporation prepares its next strategic plan, it will consider any additional areas of desired culture change and develop a process to integrate them with the management, monitoring, and reporting on culture change.

74. Weakness—Change management (organizational culture skills). We found that the corporation did not assess the expertise and skills it needed in organizational culture that would enable it to identify gaps and ensure that it successfully achieves the desired culture change. Although the corporation hired consultants to advise on change management, they were not engaged to advise specifically on the cultural implications of undertaking an organizational transformation.

75. This weakness matters because the lack of expertise or skills in organizational culture presented a risk that the corporation might not have the knowledge and skills required to implement, monitor, and support the desired culture changes. This was particularly important because culture management is a key factor for ensuring the success of the corporation’s organizational and digital transformation.

76. Recommendation. The corporation should assess its needs in culture change expertise and skills, and address any gaps to ensure the successful achievement of desired culture change.

The corporation’s response. Agreed. By the end of 2023, as it prepares its next strategic plan, the corporation will review internal talents to assess the culture skills and expertise needed to implement the plan and provide, as needed, training with the support of external advisers by the end of 2024.

Conclusion

77. In our opinion, on the basis of the criteria established, there was reasonable assurance that there were no significant deficiencies in the corporation’s systems and practices we examined. We concluded that the Royal Canadian Mint maintained its systems and practices during the period covered by the audit in a manner that provided the reasonable assurance required under section 138 of the Financial Administration Act.

About the Audit

This independent assurance report was prepared by the Office of the Auditor General of Canada on the Royal Canadian Mint. Our responsibility was to express

- an opinion on whether there was reasonable assurance that during the period covered by the audit, there were no significant deficiencies in the corporation’s systems and practices we selected for examination

- a conclusion about whether the corporation complied in all significant respects with the applicable criteria

Under section 131 of the Financial Administration Act, the corporation is required to maintain financial and management control and information systems and management practices that provide reasonable assurance of the following:

- Its assets are safeguarded and controlled.

- Its financial, human, and physical resources are managed economically and efficiently.

- Its operations are carried out effectively.

In addition, section 138 of the act requires the corporation to have a special examination of these systems and practices carried out at least once every 10 years.

All work in this audit was performed to a reasonable level of assurance in accordance with the Canadian Standard on Assurance Engagements (CSAE) 3001—Direct Engagements, set out by the Chartered Professional Accountants of Canada (CPA Canada) in the CPA Canada Handbook—Assurance.

The Office of the Auditor General of Canada applies the Canadian Standard on Quality Management 1—Quality Management for Firms That Perform Audits or Reviews of Financial Statements, or Other Assurance or Related Services Engagements. This standard requires our office to design, implement, and operate a system of quality management, including policies and procedures regarding compliance with ethical requirements, professional standards, and applicable legal and regulatory requirements.

In conducting the audit work, we complied with the independence and other ethical requirements of the relevant rules of professional conduct applicable to the practice of public accounting in Canada, which are founded on fundamental principles of integrity, objectivity, professional competence and due care, confidentiality, and professional behaviour.

In accordance with our regular audit process, we obtained the following from the corporation:

- confirmation of management’s responsibility for the subject under audit

- acknowledgement of the suitability of the criteria used in the audit

- confirmation that all known information that has been requested, or that could affect the findings or audit conclusion, has been provided

- confirmation that the audit report is factually accurate

Audit objective

The objective of this audit was to determine whether the systems and practices we selected for examination at the Royal Canadian Mint were providing the corporation with reasonable assurance that its assets were safeguarded and controlled, its resources were managed economically and efficiently, and its operations were carried out effectively, as required by section 138 of the Financial Administration Act.

Scope and approach

Our audit work examined the Royal Canadian Mint. The scope of the special examination was based on our assessment of the risks the corporation faced that could affect its ability to meet the requirements set out by the Financial Administration Act.

In carrying out the special examination, we reviewed key documents related to the systems and practices selected for examination. We interviewed members of the board of directors, senior management, and employees of the corporation. We tested the systems and practices in place to obtain the required level of audit assurance. Our testing sometimes included detailed sampling to conclude on the relevant examination criteria.

The systems and practices selected for examination for each area of the audit are found in the exhibits throughout the report.

In carrying out the special examination, we relied on the following internal audit reports of the corporation: Audit of the Occupational Health and Safety Program (2022) and Audit of Procurement (2023).

Sources of criteria

The criteria used to assess the systems and practices selected for examination are found in the exhibits throughout the report.

Corporate governance

Practice Guide: Assessing Organizational Governance in the Public Sector, The Institute of Internal Auditors, 2014

Corporate board profile and skills matrix, Royal Canadian Mint

Corporate bylaws, board charters, and terms of reference, Royal Canadian Mint

Internal Control—Integrated Framework, Committee of Sponsoring Organizations of the Treadway Commission, 2013

Strategic planning

Financial Administration Act

Guidance for Crown Corporations on Preparing Corporate Plans and Budgets, Treasury Board of Canada Secretariat, 2019

Royal Canadian Mint Act

2021–25 and 2022–26 corporate plans, Royal Canadian Mint

Annual Report 2021, Royal Canadian Mint

Recommended Practice Guideline 3, Reporting Service Performance Information, International Public Sector Accounting Standards Board, 2015

Corporate risk management

Enterprise Risk Management—Integrating with Strategy and Performance: Executive Summary, Committee of Sponsoring Organizations of the Treadway Commission, 2017

Internal Control—Integrated Framework, Committee of Sponsoring Organizations of the Treadway Commission, 2013

2021–25 and 2022–26 corporate plans, Royal Canadian Mint

Annual Report 2021, Royal Canadian Mint

Enterprise Risk Management Framework, Royal Canadian Mint

Financial Administration Act

International Organization for StandardizationISO 22301:2019—Security and resilience—Business continuity management systems

Management of operations

Internal Control—Integrated Framework, Committee of Sponsoring Organizations of the Treadway Commission, 2013

Control Objectives for Information and related TechnologyCOBIT 5 Framework—APO05 (Manage Portfolio), BAI01 (Manage Programmes and Projects), Information Systems Audit and Control AssociationISACA

Plan-Do-Check-Act management model adapted from the Deming Cycle

Directive on the Management of Procurement, Treasury Board, 2021

Memorandum of Understanding between the Royal Canadian Mint and the Department of Finance, 2022–2025

Directive on Travel, Hospitality, Conference and Event Expenditures, Treasury Board, 2017

Financial Administration Act

Transforming Our World: The 2030 Agenda for Sustainable Development, United Nations, 2015

ISO 14001:2015—Environmental management systems

International Organization for Standardization/International Electrotechnical CommissionISO/IEC 27002:2022—Information security, cybersecurity and privacy protection—Information security controls

COBIT 2019 Framework: Governance and Management Objectives, ISACA

ISO/IEC 27032:2012—Information technology—Security techniques—Guidelines for cybersecurity

Framework for Improving Critical Infrastructure Cybersecurity Version 1.1, National Institute of Standards and Technology (NIST)

ISO/IEC 27001:2013—Annex A.15: Supplier relationships

London Bullion Market AssociationLBMA Market Standards, London Bullion Market Association

Integrated Planning Guide, Treasury Board of Canada Secretariat, 2007

Ultimate Human ResourcesHR Manual, Human Resources Professionals Association and Commerce Clearing HouseCCH

Policy on People Management, Treasury Board, 2021

National Standard of Canada for Psychological Health and Safety in the Workplace, 2013

Call to Action on Anti‑Racism, Equity, and Inclusion in the Federal Public Service, Clerk of the Privy Council, 2021

Organizational and digital transformation

Leading Change, John P. Kotter, 2012

A Guide to the Project Management Body of Knowledge (PMBOK® Guide), 6th Edition, Project Management Institute IncorporatedInc., 2017

Managing Successful Projects with PRINCE2, 6th Edition, Axelos, 2017

COBIT 2019 Framework: Governance and Management Objectives, ISACA, 2019

Information Technology Infrastructure LibraryITIL® Foundation, ITIL 4th Edition, Axelos, 2019

Directive on the Management of Projects and Programmes, Treasury Board, 2019

Agile Practice Guide, Project Management Institute, 2017

International Organization for Standardization/International Electrotechnical Commission/Institute of Electrical and Electronics EngineersISO/IEC/IEEE 12207:2017—Systems and software engineering–Software life cycle processes

ISO/IEC 27001:2013—Annex A.14: System acquisition, development and maintenance

Period covered by the audit

The special examination covered the period from 1 January 2022 to 31 December 2022. This is the period to which the audit conclusion applies. However, to gain a more complete understanding of the significant systems and practices, we also examined certain matters that preceded the start date of this period.

Date of the report

We obtained sufficient and appropriate audit evidence on which to base our conclusion on 28 April 2023, in Ottawa, Canada.

Audit team

This special examination was completed by a multidisciplinary team, from across the Office of the Auditor General of Canada, led by Mathieu Le Sage, Principal. The principal has overall responsibility for audit quality, including conducting the audit in accordance with professional standards, applicable legal and regulatory requirements, and the office’s policies and system of quality management.

List of Recommendations

The following table lists the recommendations and responses found in this report. The paragraph number preceding the recommendation indicates the location of the recommendation in the report.

| Recommendation | Response |

|---|---|

|

21. The corporation should ensure that its risk mitigation actions have timelines that allow for measurement of progress against them. |

Agreed. At the end of 2022, the corporation commenced the documentation of timelines for mitigation plans of functional risks, which will be completed by the end of 2023. |

|

34. To optimize the efficiency of its Winnipeg plant, the corporation should establish mitigating strategies in response to long‑term trends in demand for foreign circulation coins. |

Agreed. By the end of 2024, as part of its next strategic plan, the corporation will develop an action plan that would allow it to respond to the risks associated with long‑term trends of foreign circulation and optimize the use of its resources in a timely manner. |

|

39. The corporation should provide the board with comprehensive reporting on the performance of its environmental management system. |

Agreed. The corporation will report its environmental performance, which includes environmental management system information, annually to the board beginning in 2024. Furthermore, since the beginning of 2023, the corporation has improved the documentation of the explicit links between its environmental, social, and governance initiatives and the United Nations’ Sustainable Development Goals, and will continue to develop these linkages with the corporation’s other activities and programs. |

|

43. The corporation should develop and implement a comprehensive information management and data governance policy, framework, and program to support information and data security objectives. |

Agreed. The corporation has prioritized its Information Management and Data Governance program to begin in 2023. Implementing information management classification is a critical next step, which the corporation will also integrate with its the overall Information Management strategy. The corporation will develop and implement its information management and data governance policies, frameworks, and programs by the end of 2025. |

|

46. The corporation should maintain a centralized list and perform regular cybersecurity risk assessment of all third-party service providers that have access to its information and data assets. |

Agreed. The corporation recognizes the importance of vendor management. The corporation will establish a centralized list of third-party service providers by the end of 2023. The corporation will also enhance our cyber security program to cover all third-party service providers that have access to our information and data set between now and the end of 2025. |

|

51. The corporation should develop and implement a workforce plan that identifies its future skills and resource needs beyond 12 months. |

Agreed. Although the corporation’s current workforce planning tools include some data beyond 12 months, the corporation will enhance its workforce planning process with a focus beyond 12 months, beginning in 2024. The competitive labour market may continue to impact the corporation’s ability to attract talent in certain areas. |

|

54. The corporation should develop an organization-wide succession planning process and ensure that related development plans or recruitment strategies are in place for key positions. |

Agreed. As it develops a more comprehensive succession planning process, to be implemented by the end of 2024, the corporation will identify and develop successors for key positions among current employees and through targeted external recruitment, where necessary. |

|

57. The corporation should implement an effective process for scheduling, delivering, and monitoring health and safety training, with the aim of ensuring that all individuals required to have hazardous materials training receive the training in a timely manner. |

Agreed. Hazardous materials training is 1 element of the emergency management program. Although COVID‑19 created challenges to delivering hazardous materials training in a timely manner, the corporation was able to respond to incidents. By the end of 2023, the corporation will implement an improved process for scheduling, delivering and monitoring health and safety training. |

|

67. The corporation should allocate sufficient resources and define the mandate and structure for its transformation office. |

Agreed. Since the end of the examination period, the corporation has restructured its Project Management Office to include the management of the organizational and digital transformations. The new structure harmonizes all project management offices, which play a key role in delivering on transformation projects and initiatives. By the end of 2023, the corporation will formalize the mandate of the Project Management Office. Since the end of the examination period, the corporation has approved a staffing plan to ensure adequate resourcing of the Project Management Office. |

|

70. The corporation should develop the methodologies and tools needed to make its project management framework more comprehensive. |

Agreed. Since the end of the examination period, the corporation has approved its Benefits Realization Framework. The framework includes measurable benefits, which are then tracked throughout both the project life cycle and post‑project close‑out by the business owner. This provides an opportunity to use the measurable benefits as target achievements against the One Mint strategy. Furthermore, by the end of 2024, the corporation will complete an assessment to determine additional methodologies and tools to help improve its project management framework with the support of its third-party risk adviser. |

|

73. The corporation should establish a plan and strategy to manage culture change efforts in a coordinated manner, and should monitor and report on progress made toward all aspects of its desired culture. |

Agreed. By the end of 2023, as the corporation prepares its next strategic plan, it will consider any additional areas of desired culture change and develop a process to integrate them with the management, monitoring, and reporting on culture change. |

|

76. The corporation should assess its needs in culture change expertise and skills, and address any gaps to ensure the successful achievement of desired culture change. |

Agreed. By the end of 2023, as it prepares its next strategic plan, the corporation will review internal talents to assess the culture skills and expertise needed to implement the plan and provide, as needed, training with the support of external advisers by the end of 2024. |