Office of the Auditor General of Canada 2022–23 Departmental Plan

ISSN 2371-7661

Message from the Auditor General of Canada

Auditor General of Canada

I am pleased to present the 2022–23 Departmental Plan of the Office of the Auditor General of Canada (OAG). In this report, we set out our plans, priorities, and expected results for the upcoming fiscal year.

Throughout the continued challenges created by the coronavirus disease (COVID‑19) pandemic and with the added complexity of a labour dispute within the organization, the OAG has remained agile and focused on delivering audits that provide objective, relevant, and value-added information for our stakeholders (Parliament, the people of Canada, and the entities we audit). The ongoing labour dispute within our organization will cause delays in our delivery of our audit products and in our progress on large corporate initiatives.

In the 2022–23 fiscal year, the OAG expects to deliver on its legislative mandate by issuing reports on 88 financial audits, 25 performance audits, and 4 special examinations.

One of our objectives in the next fiscal year includes maximizing engagement and establishing greater collaboration with our stakeholders to contribute to better-managed government programs and continued accountability to Parliament. We consider the needs of our stakeholders when selecting areas for audit to deliver value-added findings and recommendations that are relevant and timely. We also understand that federal organizations are still working to deliver services to Canadians during the pandemic.

Goal 16 of the United Nations’ Sustainable Development Goals (SDG) focuses on strengthening government institutions, and we are doing our part to make that happen in a meaningful way. We contribute to advancing the Sustainable Development Goals by integrating them into our audit work and reporting. Our own commitments to contributing to the advancement of the goals are outlined in the Sustainable Development Strategy for the Office of the Auditor General of Canada—2020–2023.

Diversity and inclusion are also priorities for the OAG. We have incorporated gender-based analysis plus (GBA Plus) considerations into our audit work. The inclusion of both SDG and GBA Plus in our work is supported through refined audit methodology and increased awareness and knowledge of the goals among our audit professionals.

We are undertaking a digital transformation to instill an OAG mindset that is responsive and adaptive to change through the use of data and digital solutions. With our integrated corporate planning approach, our available resources will be aligned and optimized to quickly respond to stakeholder needs as we carry out our work.

Our success depends on the people who work together across this organization to make our efforts count, whether under normal circumstances or when facing challenges. We are focusing on the new skills needed by our workforce as we provide our employees with a flexible work environment. While our employees are currently working mainly off-site, we are taking the opportunity to modernize our offices. Our employees will have a safe workplace with the appropriate tools to allow them to effectively collaborate and deliver value-added results.

During these times of uncertainty, the staff of the OAG have demonstrated and continue to demonstrate great resilience, caring for one another, and a devotion to excellence. Everyone across the organization remains focused on achieving the results promised in this plan. Together, we bring forward information that government organizations can use to improve their day‑to‑day work and that parliamentarians and members of the northern legislatures can use to influence meaningful change for all the people of Canada.

[Original signed by]

Karen Hogan, Fellow Chartered Professional AccountantFCPA, Fellow Chartered AccountantFCA

Auditor General of Canada

4 February 2022

Our core responsibility: Planned results and resources

This section contains information on the OAG’s planned results and resources for its core responsibility.

Legislative auditing

Our audit reports provide objective, fact-based information and expert advice on federal government programs and activities. With our audits, we assist Parliament in its work on the authorization and oversight of government spending and operations. Our audits are also used by territorial legislatures, boards of Crown corporations, and audit committees to help them oversee the management of government activities and hold them to account for the handling of public funds. Financial audits assess whether the annual financial statements of the Government of Canada, Crown corporations, and others are presented fairly, consistent with applicable accounting standards. Performance audits assess whether government organizations manage with due regard for economy, efficiency, and environmental impact, and measure their effectiveness. Special examinations assess whether Crown corporation systems and practices provide reasonable assurance that assets are safeguarded, resources are managed economically and efficiently, and operations are managed effectively.

Planning highlights

Our audits

Financial audits. In the 2022–23 fiscal year, we will conduct 88 financial audits and related assurance engagements. These include audits of the consolidated financial statements of the Government of Canada and each of the 3 territorial governments and the financial statements of federal Crown corporations, territorial corporations, and other organizations, including the United Nations Educational, Scientific and Cultural Organization (UNESCO) and the International Criminal Police Organization (INTERPOL).

Performance audits. Our performance audit practice will broaden our audit coverage of government programs and spending. In the 2022–23 fiscal year, we plan to deliver 25 performance audit reports, including those presented to Parliament by the Commissioner of the Environment and Sustainable Development and those presented to northern legislative assemblies.

In the 2022–23 fiscal year, we will present audit reports on a variety of social and environmental topics, such as homelessness, the management of nuclear waste, and the cybersecurity of personal information in the cloud. We will deliver audit reports that are in progress on COVID‑19 topics, including new work that Parliament requested in December 2021. A full list of anticipated topics for 2022–23 is available on the OAG’s website.

This list is subject to change on the basis of emerging events and government priorities.

Special examinations. Under the Financial Administration Act, federal Crown corporations are required to undergo special examinations, which are a special kind of performance audit that reviews Crown corporations’ systems and practices. These examinations are carried out in a cycle, ensuring that each corporation undergoes at least 1 examination every 10 years. In the 2022–23 fiscal year, we plan to complete 4 special examinations. A list of the Crown corporations under examination for 2022–23 is available on the OAG’s website.

Our strategic framework

When we developed our mission and vision in 2020, we set strategic objectives emphasizing caring for our people, building connections with our stakeholders, and modernizing our processes, products, and technology to facilitate delivery of our legislative auditing program.

Care. Under this objective, our focus is to foster a diverse and inclusive environment where the health and wellness of our people is paramount, where our employees have interesting opportunities for learning and growth, and where our culture helps us attract and retain diverse, skilled, and engaged professionals.

Canada is a diverse nation and our work and workplace strive to capture that breadth of backgrounds, experiences, and skills to remain relevant for all the people of Canada. We will continue to take actions toward our commitment to support diversity and inclusion and to identify and address racism, bias, and discrimination. Our renewed values, along with some core behaviours, help guide our day-to-day interactions.

A modernization initiative is underway to ensure that our workspaces provide safe, flexible, hybrid working environments with the tools needed to enhance how we work together.

Connect. Nurturing collaborative and respectful relationships rooted in trust and accountability is at the heart of this objective. To build the connections that help position the OAG as a trusted partner to spur government‑wide improvements in the best interests of Canada, we seek to better understand stakeholder needs. This enhanced understanding will allow us to develop and deliver products and services that will provide increased value to our stakeholders: Parliament, the people of Canada, and the entities we audit.

We will explore new approaches to reach out to our stakeholders in Parliament, within government, and in the external environment to help us better understand the value they expect from our work. Our goal is to ensure that our audits remain relevant and timely and that the information provided is useful for making decisions that contribute to meaningful results for Canadians.

Modernize. To modernize means we are continuously evolving and improving our approaches, tools, and products, as well as combining innovation with expertise to support the delivery of audits that remain relevant and add value for parliamentarians, the people of Canada, and the entities we audit.

We are undertaking a digital transformation to examine how people, processes, and technology work together to further enhance and streamline how we conduct our work. We continue to increase our cybersecurity through our security assessments and implementation of security controls. The current implementation of a new audit working paper tool will result in increased administrative efficiencies, improved audit quality, and the use of improved audit oversight. In addition, a more collaborative and integrated corporate planning approach will result in prioritizing, planning, resourcing, and monitoring our corporate activities and aligning them with our mission, vision, strategic objectives, and business outcomes.

Gender-based analysis plus

The OAG incorporates gender-based analysis plus considerations in our audit work, to provide elected officials and all Canadians with objective information on the impacts of program expenditures on gender and diversity. A summary of the planned activities to support the advancement of Canada’s GBA Plus commitments is included in a supplementary table accompanying this report.

United Nations’ 2030 Agenda for Sustainable Development and Sustainable Development Goals

The OAG is committed to aligning its audit work with the United Nations’ 2030 Agenda for Sustainable Development and the underlying 17 Sustainable Development Goals. All of the OAG’s audits—financial audits, performance audits, and special examinations—contribute to the goal of peace, justice, and strong institutions (Goal 16). In addition, we consider the other goals when planning and reporting on our audit work as appropriate.

Planned results

Through our legislative audits, the overall result that the OAG seeks is to contribute to a well‑managed and accountable government. Although we recognize that some of our results relating to our audits are not exclusively within our control, we seek to influence the performance of the organizations we audit through the work that we do.

The OAG maintains a departmental results framework for reporting corporate results in keeping with the Treasury Board’s Policy on Results. We also maintain an internal performance measurement framework. In the 2022–23 fiscal year, we will complete the work started in the 2021–22 fiscal year to update and renew both our results and performance measurement frameworks. Exhibit 1 shows the planned results, the result indicators, the targets, and the target dates for the 2022–23 fiscal year, as well as the actual results for the 3 most recent fiscal years for which results are available.

Exhibit 1—Planned and actual results for legislative auditing

| Departmental result | Well-managed and accountable government | ||||

|---|---|---|---|---|---|

| Departmental result indicator | Target | Date to achieve target | 2018–19 actual result |

2019–20 actual result | 2020–21 actual result |

|

Percentage of audit reports on financial statements without qualifications or “other matters” raised. |

100% |

Ongoing |

Target not met |

Target not met |

Target not met |

|

Percentage of special examination reports with no significant deficiencies. |

100% |

Ongoing |

Target not met |

Target not met |

Target not met |

|

Percentage of audit recommendations or opinions addressed by entities: For financial audits, percentage of qualifications and “other matters” addressed from one financial audit report to the next. |

100% |

Ongoing |

Target not met |

Target not met |

Target not met |

|

Percentage of audit recommendations or opinions addressed by entities: For performance audits, percentage of recommendations examined for which progress made is assessed as “substantial improvement.” |

At least 75% |

Ongoing |

No follow‑up |

No follow‑up |

Not applicablenote 4 |

|

Percentage of audit recommendations or opinions addressed by entities: For special examinations, percentage of significant deficiencies reported in our special examination reports that are addressed from one examination to the next. |

100% |

Ongoing |

Target not met |

Not applicablenote 5 |

Not applicablenote 5 |

|

Percentage of audits that meet statutory deadlines, where applicable, or our planned reporting dates: |

|||||

|

100% |

Ongoing |

Target not met |

Target not met |

Target not met |

|

At least 80% |

Ongoing |

Target met |

Target met |

Target not met |

The financial, human resources, and performance information for the OAG’s program inventory is available in the GC InfoBase.

Planned spending and human resources

This section provides an overview of the OAG’s planned spending and human resources for the next 3 fiscal years and compares planned spending for the 2022–23 fiscal year with actual spending for the current year and the previous year.

Planned spending

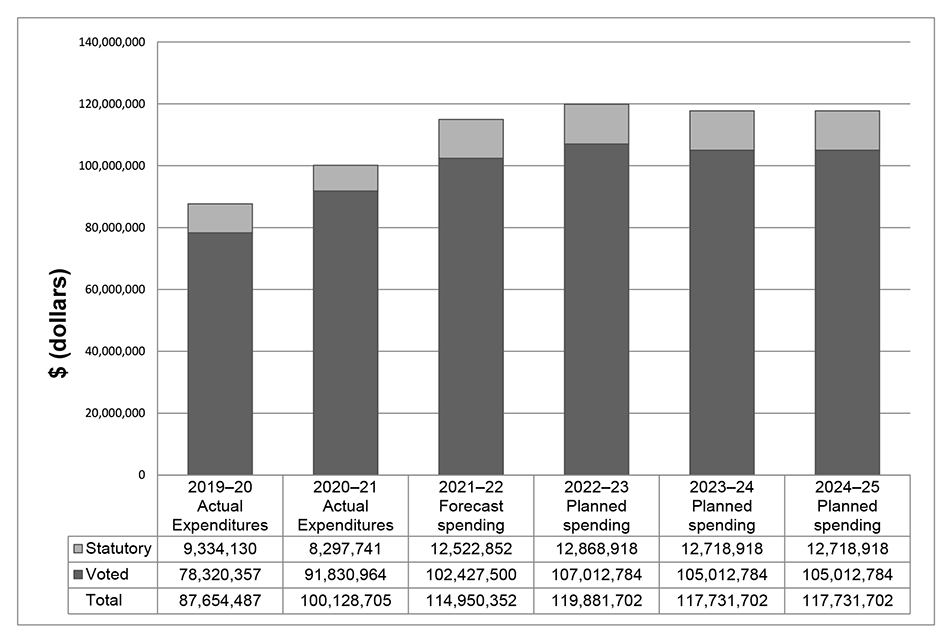

The OAG’s spending, 2019–20 to 2024–25

Exhibit 2 presents planned (voted and statutory) spending over time.

Exhibit 2—The Office of the Auditor General of Canada’s spending trend (in dollars)

Note: “Forecast spending” represents the total cost forecast to affect the current year’s authorities, and “2022–23 Planned spending” refers to those amounts requested in the Main Estimates.

Exhibit 2—text version

| 2019–20 Actual expenditures |

2020–21 Actual expenditures |

2021–22 Forecast spending |

2022–23 Planned spending |

2023–24 Planned spending |

2024–25 Planned spending |

|

|---|---|---|---|---|---|---|

| Statutory | 9,334,130 | 8,297,741 | 12,522,852 | 12,868,918 | 12,718,918 | 12,718,918 |

| Voted | 78,320,357 | 91,830,964 | 102,427,500 | 107,012,784 | 105,012,784 | 105,012,784 |

| Total | 87,654,487 | 100,128,705 | 114,950,352 | 119,881,702 | 117,731,702 | 117,731,702 |

Planned human resources

Exhibit 3 shows information on human resources, in full-time equivalents, for the OAG’s core responsibility for the 2019–20 to 2024–25 fiscal years.

Exhibit 3—Human resources planning summary (full-time equivalents)

| Actual 2019–20 |

Actual 2020–21 |

Forecast 2021–22 |

Planned full-time equivalents | ||

|---|---|---|---|---|---|

| 2022–23 | 2023–24 | 2024–25 | |||

| 567 | 632 | 737 | 747 | 737 | 737 |

Estimates by vote

Information on the OAG’s organizational appropriations is available in the 2022–23 Main Estimates.

Future-oriented condensed statement of operations

Exhibit 4 presents the future-oriented condensed statement of operations of the OAG. The forecast of financial information on expenses and revenues is prepared on an accrual accounting basis to strengthen accountability and to improve transparency and financial management. The forecast and planned spending amounts presented in other sections of the Departmental Plan are prepared on an expenditure basis and, as a result, differ from the forecast and planned results presented below.

Exhibit 4—Future-oriented condensed statement of operations for the year ending 31 March 2023 (in thousands of dollars)

| Financial information | 2021–22 Forecast results |

2022–23 Planned results |

|---|---|---|

| Financial audits of Crown corporations, territorial governments, and other organizations, and of the summary financial statements of the Government of Canada | 66,000 | 65,400 |

| Performance audits and studies | 47,800 | 54,200 |

| Special examinations of Crown corporations | 5,200 | 5,500 |

| Sustainable development monitoring activities and environmental petitions | 3,300 | 3,000 |

| Professional practices | 7,100 | 6,500 |

| Total cost of operations | 129,400 | 134,600 |

| Total revenues | (850) | (1,100) |

| Net cost of operations before government funding and transfers | 128,550 | 133,500 |

Note to the future-oriented condensed statement of operations—Parliamentary authorities

The OAG is financed by the Government of Canada through parliamentary authorities. Financial reporting of authorities provided to the OAG differs from financial reporting according to generally accepted accounting principles because authorities are based mainly on cash flow requirements. Items recognized in the future-oriented statement of operations in one year may be funded through parliamentary authorities in prior, current, or future years. Accordingly, the OAG has a different net cost of operations for the year on a government funding basis than on an accrual accounting basis. The differences are reconciled in Exhibit 5.

Exhibit 5—Reconciliation of net costs of operations to authorities forecast (in thousands of dollars)

| 2021–22 Forecast results |

2022–23 Planned results |

|

|---|---|---|

| Net cost of operations before government funding and transfers | 128,550 | 133,500 |

| Adjustments for items recorded as part of net cost of operations but not affecting current year authorities: | ||

|

Services provided without charge by other government departments

|

(15,300) | (15,500) |

|

Amortization of tangible capital assets

|

(700) | (850) |

|

Total items recorded as part of net cost of operations but not affecting current year authorities

|

(16,000) | (16,350) |

| Adjustments for items not recorded as part of net cost of operations but affecting current year authorities: | ||

|

Acquisition of tangible capital assets

|

700 | 2,300 |

|

Decrease in liabilities not previously charged to authorities

|

1,700 | 700 |

|

Total items not recorded as part of net cost of operations but affecting current year authorities

|

2,400 | 3,000 |

| Forecast spending (authorities forecast to be used) | 114,950 | 120,150 |

| Add: Forecast lapse (authorities forecast to be lapsed) | 7,156 | 5,364 |

| Authorities forecast (authorities forecast to be requested) | 122,106 | 125,514 |

| Main Estimates | ||

|

Vote 1: Program expenditures

|

104,834 | 107,013 |

|

Statutory amounts: Contributions to employee benefit plans

|

12,523 | 12,869 |

|

Total Main Estimates

|

117,357 | 119,882 |

| Supplemental operating authorities | 1,570 | 1,400 |

| Authorities carried forward from previous yearnote 1 | 3,179 | 4,232 |

| Authorities forecast (authorities forecast to be requested) | 122,106 | 125,514 |

Corporate information

Organizational profile

Auditor General of Canada: Karen Hogan, Fellow Chartered Professional AccountantFCPA, Fellow Chartered AccountantFCA

Main legislative authorities:

Auditor General Act, Revised Statutes of CanadaR.S.C. 1985, c. A-17

Financial Administration Act, R.S.C. 1985, c. F-11

Year established: 1878

Minister: The Honourable Chrystia Freeland, Privy CouncillorP.C., Member of ParliamentM.P., Minister of Financefootnote *

Raison d’être, mandate, and role: Who we are and what we do

Information on the OAG’s raison d’être, mandate, and role is available on the OAG’s website.

Operating context

Information on the operating context is available on the OAG’s website.

Reporting framework

The OAG’s departmental results framework and program inventory of record for the 2022–23 fiscal year are shown in Exhibit 6.

Exhibit 6—The OAG’s departmental results framework and program inventory

Core responsibility: Legislative auditing

|

Description Our audit reports provide objective, fact‑based information and expert advice on federal government programs and activities. With our audits, we assist Parliament in its work on the authorization and oversight of government spending and operations. Our audits are also used by territorial legislatures, boards of Crown corporations, and audit committees to help them oversee the management of government activities and hold them to account for the handling of public funds. Financial audits assess whether the annual financial statements of the Government of Canada, Crown corporations, and others are presented fairly, consistent with applicable accounting standards. Performance audits assess whether government organizations manage with due regard for economy, efficiency, and environmental impact, and measure their effectiveness. Special examinations assess whether Crown corporation systems and practices provide reasonable assurance that assets are safeguarded, resources are managed economically and efficiently, and operations are managed effectively. |

Result and indicators |

|

Well-managed and accountable government:

|

|

|

Program inventory |

|

|

Supporting information on the program inventory

Supporting information on planned expenditures, human resources, and results related to the OAG’s program inventory is available in the GC InfoBase.

Supplementary information tables

The following supplementary information tables are available on the OAG’s website:

Additionally, details communicating our implementation of the United Nations’ 2030 Agenda and Sustainable Development Goals can be found in these documents.

Federal tax expenditures

The OAG’s Departmental Plan does not include information on tax expenditures.

Tax expenditures are the responsibility of the Minister of Finance. The Department of Finance Canada publishes cost estimates and projections for government‑wide tax expenditures each year in the Report on Federal Tax Expenditures. This report provides detailed information on tax expenditures, including objectives, historical background, and references to related federal spending programs, as well as evaluations, research papers, and gender-based analysis plus.

Planned reports for 2022–23

A list of our planned reports for 2022–23 is available on the OAG’s website.

Organizational contact information

Mailing address

Office of the Auditor General of Canada

240 Sparks Street

Ottawa, Ontario K1A 0G6

CANADA

Telephone: 613‑995‑3708 or 1‑888‑761‑5953

Hearing impaired only telecommunications device for the deafTTY: 613‑954‑8042

Fax: 613‑957‑0474

Email: communications@oag-bvg.gc.ca

Website: www.oag-bvg.gc.ca

Appendix: Definitions

appropriation (crédit)

Any authority of Parliament to pay money out of the Consolidated Revenue Fund.

budgetary expenditures (dépenses budgétaires)

Operating and capital expenditures; transfer payments to other levels of government, organizations or individuals; and payments to Crown corporations.

core responsibility (responsabilité essentielle)

An enduring function or role performed by a department. The intentions of the department with respect to a core responsibility are reflected in one or more related departmental results that the department seeks to contribute to or influence.

Departmental Plan (plan ministériel)

A document that sets out a department’s priorities, programs, expected results, and associated resource requirements, covering a 3‑year period beginning with the year indicated in the title of the report. Departmental Plans are tabled in Parliament each spring.

departmental result (résultat ministériel)

A change that a department seeks to influence. A departmental result is often outside departments’ immediate control, but it should be influenced by program-level outcomes.

departmental result indicator (indicateur de résultat ministériel)

A factor or variable that provides a valid and reliable means to measure or describe progress on a departmental result.

departmental results framework (cadre ministériel des résultats)

A framework that consists of the department’s core responsibilities, departmental results, and departmental result indicators.

Departmental Results Report (rapport sur les résultats ministériels)

A report on a department’s actual performance in a fiscal year against its plans, priorities, and expected results set out in its Departmental Plan for that year. Departmental Results Reports are usually tabled in Parliament each fall.

experimentation (expérimentation)

The conducting of activities that explore, test, and compare the effects and impacts of policies and interventions in order to inform decision making and improve outcomes for Canadians. Experimentation is related to, but distinct from, innovation. Innovation is the trying of something new; experimentation involves a rigorous comparison of results. For example, introducing a new mobile application to communicate with Canadians can be an innovation; systematically testing the new application and comparing it against an existing website or other tools to see which one reaches more people, is experimentation.

full‑time equivalent (équivalent temps plein)

A measure of the extent to which an employee represents a full person‑year charge against a departmental budget. Full‑time equivalents are calculated as a ratio of assigned hours of work to scheduled hours of work. Scheduled hours of work are set out in collective agreements.

gender-based analysis plus (GBA Plus) (analyse comparative entre les sexes plus [ACS Plus])

An analytical tool used to support the development of responsive and inclusive policies, programs, and other initiatives, and understand how factors such as sex, race, national and ethnic origin, Indigenous origin or identity, age, sexual orientation, socio-economic conditions, geography, culture, and disability impact experiences and outcomes and can affect access to and experience of government programs.

government-wide priorities (priorités pangouvernementales)

For the purpose of the 2022-23 Departmental Plan, government-wide priorities are the high-level themes outlining the Government’s agenda in the 2021 Speech from the Throne: building a healthier today and tomorrow; growing a more resilient economy; bolder climate action; fighter harder for safer communities; standing up for diversity and inclusion; moving faster on the path to reconciliation; and fighting for a secure, just, and equitable world.

horizontal initiative (initiative horizontale)

An initiative in which 2 or more federal organizations are given funding to pursue a shared outcome, often linked to a government priority.

non‑budgetary expenditures (dépenses non budgétaires)

Net outlays and receipts related to loans, investments and advances, which change the composition of the financial assets of the Government of Canada.

performance (rendement)

What an organization did with its resources to achieve its results, how well those results compare to what the organization intended to achieve, and how well lessons learned have been identified.

performance audit (audit de performance)

An independent, objective, and systematic assessment of how well the government is managing its activities, responsibilities, and resources.

plan (plan)

The articulation of strategic choices, which provides information on how an organization intends to achieve its priorities and associated results. Generally, a plan will explain the logic behind the strategies chosen and tend to focus on actions that lead up to the expected result.

planned spending (dépenses prévues)

For Departmental Plans and Departmental Results Reports, planned spending refers to those amounts presented in the Main Estimates.

A department is expected to be aware of the authorities that it has sought and received. The determination of planned spending is a departmental responsibility, and departments must be able to defend the expenditure and accrual numbers presented in their Departmental Plans and Departmental Results Reports.

program (programme)

Individual or groups of services, activities or combinations thereof that are managed together within a department and that focus on a specific set of outputs, outcomes, or service levels.

program inventory (répertoire des programmes)

An inventory of a department’s programs that describes how resources are organized to carry out the department’s core responsibilities and achieve its planned results.

result (résultat)

An external consequence attributed, in part, to an organization, policy, program, or initiative. Results are not within the control of a single organization, policy, program, or initiative; instead, they are within the area of the organization’s influence.

special examination (examen spécial)

A form of performance audit that is conducted within Crown corporations. The scope of special examinations is set out in the Financial Administration Act. A special examination considers whether a Crown corporation’s systems and practices provide reasonable assurance that its assets are safeguarded and controlled, its resources are managed economically and efficiently, and its operations are carried out effectively.

statutory expenditures (dépenses législatives)

Expenditures that Parliament has approved through legislation other than appropriation acts. The legislation sets out the purpose of the expenditures and the terms and conditions under which they may be made.

target (cible)

A measurable performance or success level that an organization, program, or initiative plans to achieve within a specified time period. Targets can be either quantitative or qualitative.

voted expenditures (dépenses votées)

Expenditures that Parliament approves annually through an Appropriation Act. The vote wording becomes the governing conditions under which these expenditures may be made.