2014 Fall Report of the Auditor General of Canada Chapter 5—Support to the Automotive Sector

2014 Fall Report of the Auditor General of Canada

Chapter 5—Support to the Automotive Sector

Table of Contents

- Introduction

- Observations and Recommendations

- Conclusion

- About the Audit

- Appendix A—Managing financial support to private sector firms

- Appendix B—List of recommendations

- Exhibits:

Performance audit reports

This report presents the results of a performance audit conducted by the Office of the Auditor General of Canada under the authority of the Auditor General Act.

A performance audit is an independent, objective, and systematic assessment of how well government is managing its activities, responsibilities, and resources. Audit topics are selected based on their significance. While the Office may comment on policy implementation in a performance audit, it does not comment on the merits of a policy.

Performance audits are planned, performed, and reported in accordance with professional auditing standards and Office policies. They are conducted by qualified auditors who

- establish audit objectives and criteria for the assessment of performance;

- gather the evidence necessary to assess performance against the criteria;

- report both positive and negative findings;

- conclude against the established audit objectives; and

- make recommendations for improvement when there are significant differences between criteria and assessed performance.

Performance audits contribute to a public service that is ethical and effective and a government that is accountable to Parliament and Canadians.

Introduction

Background

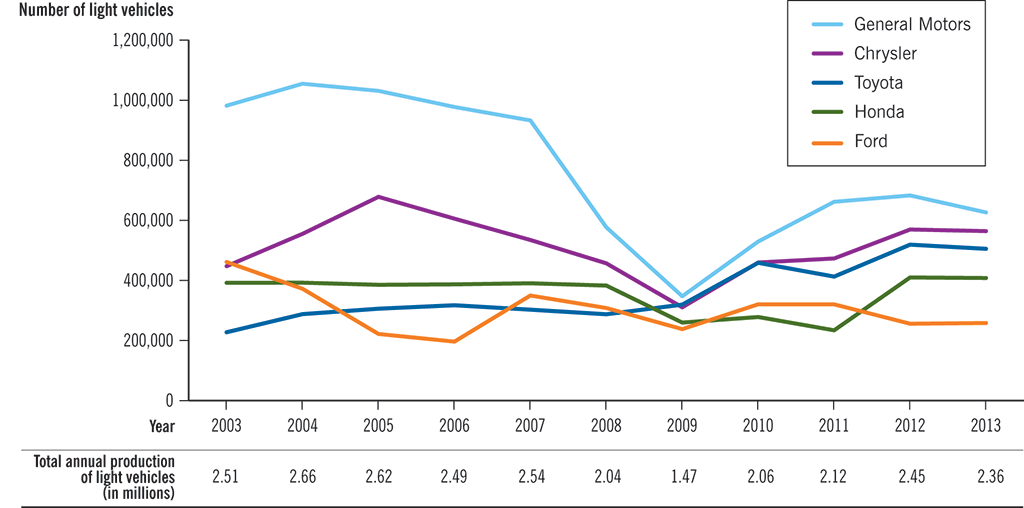

5.1 The Canadian automotive industry consists of five car manufacturers and hundreds of Canadian suppliers of automotive parts. The industry is largely concentrated in Ontario. Approximately 85 percent of cars produced in Canada are exported, and these exports are sent almost exclusively to the United States. Exported vehicles and parts represent about 15 percent of Canada’s manufactured product exports. Exhibit 5.1 shows the production of light vehicles in Canada from 2003 to 2013.

Exhibit 5.1—Production of light vehicles in Canada, 2003-2013

5.2 The global economic recession of 2008 negatively affected Canada’s production and employment in the automotive industry. In 2007, approximately 1.5 percent ($21.4 billion) of the Canadian gross domestic product was attributable to the car industry, compared with about 1.1 percent ($19.1 billion) in 2013. In 2007, car manufacturers and parts suppliers employed 152,000 people. In 2013, the sector employed about 117,000 people.

5.3 The 2008 economic downturn and the lack of access to credit made it harder for potential buyers to obtain car loans, and for car dealers to secure inventory financing. As a result, vehicle sales declined sharply in the United States and Canada. Some parts companies and some manufacturers, including Chrysler and General Motors (GM), could not generate sufficient income to fund their operations. In response to these conditions, the companies accelerated their efforts to restructure their operations and reduce costs. However, the widespread financial turmoil made it difficult for some of these companies to access financial markets for assistance.

5.4 According to Industry Canada, the five automobile manufacturers in Canada buy many of their parts from the same major suppliers. During the economic downturn, the government was concerned that the loss of one or more manufacturers would compromise the financial stability of these suppliers and threaten their ability to supply the remaining manufacturers. The interdependence of manufacturers and suppliers had the potential, therefore, to destabilize the entire industry.

5.5 Economic impact studies carried out in 2008 and 2009 found that if Chrysler and GM had ceased production in Canada in 2009, the Canadian economy would have lost many thousands of jobs over a short period. In addition, government tax revenues would have decreased while some expenditures, such as those for social programs, would have increased.

5.6 The federal government has put in place a number of initiatives to support the automotive sector. This chapter covers two of these initiatives:

- the financial assistance for restructuring Chrysler and GM in 2009; and

- the Automotive Innovation Fund (launched in February 2008), which provides financial support for eligible investment projects undertaken by automotive companies in Canada.

Restructuring of Chrysler and General Motors

5.7 In 2008, Chrysler Canada employed approximately 8,400 people. It had three main production sites in Ontario: a casting plant in Etobicoke and assembly plants in Windsor and Brampton. Chrysler Canada also operated a research and development centre in Windsor.

5.8 In 2008, General Motors of Canada Limited (GM Canada) employed approximately 12,500 people. It assembled cars and trucks in Oshawa and Ingersoll, and made engines and transmissions in Windsor and St. Catharines. It also had an engineering research centre in Oshawa.

5.9 In November 2008, the Chrysler and GM parent companies approached the US government for financial assistance. In December 2008, the US government announced that it would provide interim financial support to Chrysler and GM. Shortly thereafter, the governments of Canada and Ontario joined the US government and offered financial assistance to Chrysler Canada and GM Canada. The federal and provincial governments agreed to provide two thirds and one third, respectively, of the Canadian share of assistance.

5.10 Between December 2008 and July 2009, the federal government worked with the governments of Ontario and the United States, and the companies, to determine the conditions and the level of financial assistance for Chrysler’s and GM’s restructuring. As a condition for this assistance, the companies were required to develop plans that would demonstrate that they could be viable in the short and long terms and ensure that Canada would retain its share of the companies’ North American production.

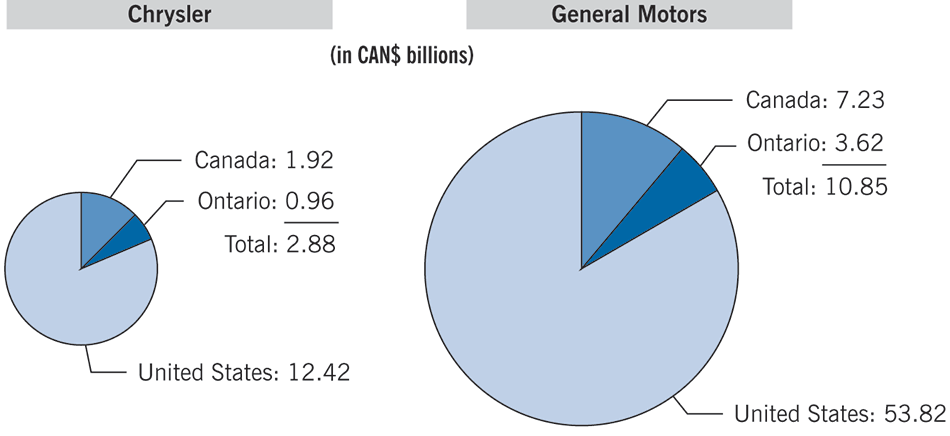

5.11 The operations of the Canadian subsidiaries of Chrysler and GM were closely integrated with those of the parent companies in the United States. Consequently, the governments of Canada and Ontario offered financial assistance proportionate to the share of manufacturing located in Canada for each company and participated financially in the restructuring of the US parents and their Canadian subsidiaries. Exhibit 5.2 shows the total amounts of assistance provided to Chrysler and GM from Canada, Ontario, and the United States.

Exhibit 5.2—Canada and Ontario contributed $13.7 billion to Chrysler and General Motors in 2009

Note: Amounts for the United States have been converted to Canadian dollars. The U.S. Government Accountability Office listed these amounts as US$10.4 billion for Chrysler and US$49.5 billion for General Motors.

Sources: Data from Public Accounts of Canada, 2009–10 and the U.S. Government Accountability Office

5.12 On 30 April 2009, Chrysler entered a court-supervised bankruptcy process in the United States. It emerged from that process on 10 June 2009 as a new company with an alliance with Fiat. GM entered into a similar court-supervised bankruptcy process in the United States on 1 June 2009. It emerged from bankruptcy on 10 July 2009 and began its operations as a new company. Chrysler Canada and GM Canada did not go through bankruptcy in Canada—they remain subsidiaries of the new companies.

Automotive Innovation Fund

Contribution—Transfer payment that is subject to the performance conditions specified in the funding agreement. Contributions are to be accounted for and are subject to audit. They may be repayable in whole or in part if conditions specified in the contribution agreement come into being. Unconditionally repayable contributions must be repaid without qualification.

5.13 In 2008, the federal government launched the Automotive Innovation Fund program. The program’s objective is to support automotive firms in their strategic, large-scale research and development projects to produce innovative, greener, and more fuel-efficient vehicles. In addition, the government expects the program to contribute to a more competitive Canadian automotive sector. For each project, a potential recipient is required to invest a minimum of $75 million over five years. The support can take the form of a conditionally or unconditionally repayable contribution, which is taxable in the year it is received. The repayment terms are negotiated on a case-by-case basis.

5.14 The initial program budget was $250 million available over five fiscal years (2008–09 to 2012–13). The program was renewed in January 2013 with an additional $250 million available over the next five fiscal years (2013–14 to 2017–18). In February 2014, the government added $500 million to the program budget ($250 million per year in the 2014–15 and 2015–16 fiscal years). As of May 2014, the program had committed to a maximum of $310 million for six approved projects, of which $131 million had been paid.

Roles and responsibilities

Restructuring plan—A plan produced by a company with significant financial difficulties to restore its viability in the short and long terms. The plan lays out the actions to be taken, the costs of these actions, the sources of funds, and the milestones to be met. It also serves as a tool for monitoring whether the actions taken and funds used were according to plan.

5.15 The federal government approved the level and share of Canada’s financial assistance toward the restructuring of Chrysler and GM. Industry Canada was responsible for

- analyzing the restructuring plans of the companies, including their subsidiaries;

- negotiating with Ontario and the US Government, on behalf of the federal government, the levels of financial assistance to be provided to the companies;

- negotiating with the companies, on the federal government’s behalf, the terms and conditions of the loans; and

- providing guidance and confirmation to Export Development Canada in all important matters involving loans and advances.

In addition, Industry Canada is responsible for managing the Automotive Innovation Fund program.

Canada Account—An account used by the Government of Canada for transactions it considers to be in the national interest. Under section 23 of the Export Development Act, the Government of Canada can authorize support for these transactions, which are administered and executed by Export Development Canada. The government assumes the associated financial risks by providing all funds required for the transactions.

5.16 The financial assistance for restructuring Chrysler and GM, and their Canadian subsidiaries, was provided to the companies through loan transactions funded from the Canada Account, under the Export Development Act. Loan agreements could be entered into with Canadian subsidiaries or with US parent companies. In the case of GM, most loans were converted into shares.

5.17 Export Development Canada was responsible for seeking and receiving the authorizations needed to undertake transactions under the Canada Account. The Corporation was also responsible for administering and executing the loan transactions, in accordance with the confirmation and guidance of Industry Canada.

5.18 The Department of Finance Canada was responsible for analyzing and reporting on the Government of Canada’s fiscal situation and outlook. The Minister of Finance concurred with the Minister of International Trade to recommend government approval of the amounts of funding needed for the Canada Account transactions.

Focus of the audit

5.19 The audit examined whether Industry Canada, the Department of Finance Canada, and Export Development Canada, in fulfilling their respective roles and responsibilities, managed the financial support to the automotive sector in a way that contributed to the viability of the companies and the competitiveness of the sector in Canada. In looking at the financial assistance provided to restructure Chrysler and GM, the audit team examined the entities’ management of the loans, which included

- gathering the information for decision making,

- analyzing risks,

- setting terms and conditions,

- overseeing loans and monitoring conditions, and

- reporting on use and results of financial assistance.

In this part of the audit, which covered the period from December 2008 to May 2014 (when the examination phase ended), we examined the information available to federal government entities. We did not audit the records of the private sector companies, the Government of Ontario, or the US Government. Consequently, our conclusions cannot and do not pertain to the companies’ practices or performance, or to the work of other governments.

5.20 In looking at the Automotive Innovation Fund, the audit team examined whether Industry Canada managed the program in a manner that took risks into account, and whether the Department monitored and reported measurements of the results against the program’s objectives. This part of the audit covered the period from February 2008 (the program’s beginning), to May 2014 (the end of the examination phase).

5.21 More details on the audit objectives, scope, approach, and criteria are in About the Audit at the end of this chapter.

Observations and Recommendations

Planning the restructuring assistance

5.22 We examined whether Industry Canada and the Department of Finance Canada had planned the financial assistance for Chrysler and General Motors (GM), and their Canadian subsidiaries, in a manner that would contribute to the companies’ viability in Canada. Specifically, we looked at how the entities obtained relevant information for decision making, analyzed risks, and set the terms and conditions of the loans.

5.23 Overall, we found that Industry Canada sought and obtained relevant information and analysis to help it understand the prospects for Chrysler’s and GM’s recoveries, and to help the government decide whether to participate in the financing of the companies’ restructuring. However, the Department had limited analysis performed on the restructuring plans for the Canadian subsidiaries, and its analyses of the required concessions from unionized labour, suppliers, and dealerships were at a high level. Industry Canada had limited documentation to show how it determined the amount of financial assistance provided to help GM Canada deal with its health care costs and pension deficits.

Industry Canada gathered relevant information to assess the recovery prospects of Chrysler and General Motors

5.24 We found that Industry Canada obtained information and had analysis to help it understand the recovery prospects for Chrysler and GM, and to help the government decide whether to contribute financially to the restructuring of the companies. The Department hired consulting firms to help it collect and analyze relevant information about the companies’ situations, including their financial situation, production costs, plans for future car models, and forecasts of production levels in Canada. The Department also consulted with automotive industry specialists to deepen its understanding of the companies’ strategies and risks, and it obtained relevant information on the Canadian subsidiaries.

5.25 The federal government made its decisions on financial assistance in a period of high uncertainty and within tight time frames. It set the broad parameters of its contribution in cooperation with Ontario and the United States. The governments of Canada, Ontario, and the United States agreed that Canada’s assistance would be used to restructure both the Canadian subsidiaries and the parent companies. Canada’s total share of assistance would be based on the ratio of Canadian automotive production to the total automotive production of the three countries of the North American Free Trade Agreement (NAFTA)—Canada, Mexico, and the United States. This share was established at 20 percent for Chrysler and 16 percent for GM.

5.26 Within these parameters, the government set the conditions that Chrysler Canada and General Motors of Canada Limited (GM Canada) would have to meet in order to have access to the financial assistance. One of these conditions was that over a certain period, the companies would maintain production volumes in Canada that were proportionate to those of the three NAFTA countries. The Department of Finance Canada supported the federal government in making these decisions by providing estimates of the financial risks associated with the government’s assistance to the companies. Export Development Canada administered and executed loans, totalling $13.7 billion, to Chrysler and GM and to their Canadian subsidiaries. Exhibit 5.3 provides details on the loans made to Chrysler and GM.

Exhibit 5.3—Total loans to Chrysler and General Motors from Canada and Ontario

| Type of loan | Amount to borrower (CAN$ billions) | |||

|---|---|---|---|---|

| Chrysler Canada | Chrysler | GM Canada | GM | |

| Original financing1 | 1.2 | 0.0 | 2.8 | 0.0 |

| Debtor-in-possession2 | 0.0 | 1.3 | 0.0 | 3.5 |

| Exit financing3 | 0.4 | 0.0 | 0.0 | 4.5 |

| Total | 1.6 | 1.3 | 2.8 | 8.0 |

1 Loans provided to Canadian subsidiaries before and during the bankruptcy process of the parent companies in the United States.

2 Loans made to Chrysler LLC and General Motors Corporation after they had filed for bankruptcy in the United States.

3 Loans made after the parent companies emerged from bankruptcy. GM transferred $4 billion of this loan to GM Canada (for pension and health care).

Source: Data from Export Development Canada

5.27 This finding is important because in deciding whether to provide financial assistance for the companies’ restructuring, the Government of Canada needed to understand the companies’ prospects for recovery and the financial risks involved.

Industry Canada had limited information on the restructuring of Canadian operations

5.28 We reviewed Industry Canada’s documents on the companies’ restructuring plans, on concessions from stakeholders, and on health care and pension liabilities.

5.29 Restructuring of subsidiaries. One of the original conditions of the federal government’s financial assistance for the restructuring of Chrysler Canada and GM Canada was that each company would produce an acceptable restructuring plan. In March 2009, Canada, Ontario, and the United States rejected the plans presented by the companies and gave them deadlines to revise them. We found that Industry Canada did not require final plans from Chrysler or GM on the restructuring of their Canadian operations. Rather, the Department considered that various documents outlining particular elements, including the original draft plans, together constituted the final plans. Department officials told us that the federal government did not need to have final restructuring plans from the Canadian subsidiaries when it approved the financial assistance made available to each of them. The officials added that the government had set specific conditions for further financial assistance (such as concessions from stakeholders) when it rejected the companies’ initial restructuring plans, and that these conditions did not require new restructuring plans. Furthermore, the Department stated that the financial assistance from Canada focused on Chrysler and GM globally, rather than just on their Canadian subsidiaries.

5.30 Despite the absence of final restructuring plans, Industry Canada had high-level information on what the Canadian restructuring costs would be, how much government funding would be needed, and what the funds would be used for. The Department also had limited analysis showing how the restructuring actions would improve the financial situations of the Canadian subsidiaries, what concessions had been made by stakeholders, and how the companies would repay their loans.

5.31 Concessions from stakeholders. In a restructuring, concessions from stakeholders may be necessary to improve a company’s future prospects and help reduce the need for public funds. A condition of the federal government’s assistance was that stakeholders of Chrysler Canada and GM Canada would make concessions.

5.32 We found that Industry Canada did not assess the impact of the concessions to be made by unionized labour, suppliers, and dealerships on the companies’ costs or long-term viability. Industry Canada officials told us that the government had set an expectation regarding the labour costs of Canadian subsidiaries. They added that each company and the union were to determine the specific concessions to be made within the broad parameter set by the government. The federal government concluded that the concessions were sufficient, based on information the companies provided, which illustrated how the agreements the companies had reached with the union met the government’s expectation. We also found that Industry Canada had limited analysis on whether suppliers and dealerships had made concessions to help reduce the companies’ costs.

5.33 GM Canada’s health care and pension liabilities. Industry Canada had information from GM Canada stating that two significant factors jeopardized its future viability: the costs of providing health care benefits to its retirees, and the deficits of its two pension plans. As part of the financial assistance to the company, $1 billion was set aside for reducing the health care liabilities and $4 billion for reducing its pension deficits.

5.34 We found that Industry Canada had limited analysis performed on GM Canada’s liabilities for health care benefits for retired employees, and on the impact these liabilities would have on the company’s future viability. Although Industry Canada had an estimate of the liabilities, it had limited information and analysis regarding the nature of the benefits, the concessions made to reduce them, and GM Canada’s ability to pay for them.

5.35 Industry Canada officials told us that the details of the changes to benefits were to be negotiated between the company and the union. However, the Department had limited documentation outlining how it determined the amount of public funds to provide to GM Canada regarding these liabilities.

5.36 In the context of the restructuring of Chrysler Canada and GM Canada, the government presented amendments to the Income Tax Act to allow a new category of trust to take over the health care obligations of Canadian companies. In December 2010, the amendments came into force, and implementation of the trusts allowed Chrysler Canada and GM Canada to eliminate health care liabilities from their balance sheets.

5.37 Ontario has jurisdiction over pension matters, including the supervision of GM Canada pension plans. From November 1992 to August 2009, Ontario pension regulations contained a special provision that allowed GM Canada to delay the payments needed to eliminate the deficits of its pension plans. In August 2009, Ontario issued a new regulation covering GM Canada pension plans. The new regulation set out the applicable provisions and how the financial assistance provided to pension plans would be used.

5.38 Although more than a third of federal assistance provided to GM was dedicated to GM Canada pension deficits, we found that Industry Canada had limited documentation to show how it determined the amount of public funds allocated for this purpose. It also had limited analysis performed on the extent to which these funds would help reduce the pension plan deficits and improve the solvency of the pension plans. The Department also had limited information and analysis on the company’s pension liabilities, the effects of the pension plan deficits on the company’s viability, and the extent to which the company could pay to reduce the deficits.

5.39 Furthermore, Industry Canada had limited information on the types of benefits GM Canada’s pension plans provided, and on the concessions that had been negotiated by the union and the company to help reduce future pension costs and liabilities. Department officials told us that the government did not need this information to make decisions because the company and union negotiated changes to pension benefits to meet the government’s expectations regarding labour costs. They added that during the restructuring of GM Canada, the Government of Ontario was responsible for matters related to pensions. In our view, however, given the size of the federal assistance, the Department needed more analysis on how the assistance would affect the company’s pension plans and viability in the short and long terms.

5.40 These findings are important because the financial assistance was intended to restore the viability of Chrysler Canada and GM Canada, and their parent companies. Industry Canada did not require final restructuring plans for the Canadian operations. The Department had high-level information on how much funding would be needed to restore the viability of the Canadian subsidiaries. Paragraph 5.67 contains a recommendation related to reviewing the management of the financial assistance provided to Chrysler and GM. Appendix A includes suggested practices for planning the financial assistance provided to private firms.

Monitoring the restructuring assistance

5.41 We examined the loan documents and related materials of Export Development Canada, and Industry Canada’s documents related to

- the financial assistance to restructure Chrysler Canada and General Motors of Canada Limited (GM Canada),

- Industry Canada’s monitoring of the production commitments made by Chrysler Canada and GM Canada, and

- the amounts repaid by the companies or recovered by selling shares.

5.42 Overall, we found that while Industry Canada monitored the companies’ commitments, its information on the use of the funds was limited to broad categories, except for the assistance provided to GM Canada that was used to help cover its health care and pension costs. The Department of Finance Canada prudently estimated the financial risks of assisting the companies.

Industry Canada monitored the use of the financial assistance, but only at a high level

5.43 We reviewed the terms and conditions of the Export Development Canada loans, along with other documents that covered the financial assistance for restructuring Chrysler Canada and GM Canada. Our review focused on information related to the use of funds.

5.44 We found that with the exception of the financial assistance provided to GM Canada for health care costs and for pension liabilities—which were placed in separate accounts—the Department had limited information on how the funds were used. Industry Canada did not require the companies to submit specific reports on their use of the funds. However, between June 2009 and March 2010, the Department received regular reports from the parent company General Motors (GM) on the company’s projected cash flows. The Department used these reports to monitor GM Canada’s liquidity. The Department took a similar approach with Chrysler between May 2009 and February 2011. This process allowed monitoring of the companies’ short-term viability.

5.45 In our view, however, the monitoring provided only high-level information on how the public funds were used. For example, Industry Canada had limited documentation on the actual use of a $2.8 billion loan made to GM Canada for capital expenditures, warranty claims, and other general corporate purposes. Furthermore, the Department had no documentation on the use of more than $528 million for general corporate purposes that was part of the $4.5 billion loan made to GM in July 2009.

5.46 We also found that $1 billion of the $4 billion that had been earmarked for GM Canada’s pension plans and placed in a separate account was paid instead to the US parent company in September 2009. Neither Industry Canada nor Export Development Canada had documents related to the use of these funds. Industry Canada officials told us that the funds had been set aside in case GM Canada could not meet its commitment to contribute $1 billion to its pension plans. Once Export Development Canada received confirmation from Ontario that GM Canada had contributed to its pension plans, the Corporation authorized the release of the funds to the parent company.

5.47 This finding is important because in the absence of detailed information on the use of the funds, Industry Canada does not know to what extent the federal government’s financial assistance contributed to the viability of Chrysler Canada and GM Canada.

Industry Canada adequately monitored production commitments

5.48 In exchange for financial assistance, Chrysler Canada committed to producing a specific volume of vehicles. GM Canada committed to meeting certain production targets for vehicles, engines, and transmissions. It also committed to reaching set annual capital expenditure levels and research and development expenditures. We reviewed Industry Canada’s monitoring of these commitments.

5.49 We found that Industry Canada received from Chrysler Canada and GM Canada reports and other documents regarding their production commitments. Having analyzed this information, the Department considers that these commitments have been met. The Department maintains contact with the companies to ensure that they continue to interpret all aspects of the commitments correctly, and it takes steps to clarify potential differences in interpretation when necessary. Chrysler Canada’s production commitment ended in 2011. For GM Canada, all commitments remain valid until December 2016.

5.50 This finding is important because Chrysler and GM production volume commitments were an important factor in the government’s decision to provide financial assistance to these companies. Maintaining Canada’s share of production in exchange for the financial assistance was a key government objective.

The governments have so far recovered about $5.4 billion of their funds

5.51 We examined whether the Department of Finance Canada assessed the risk that the funds would not be recovered. In addition, we reviewed the amounts repaid or recovered, and we examined the final costs of the assistance. Unless otherwise noted, the amounts in this section represent the combined portions of Canada and Ontario.

5.52 Conversion of loans into GM shares. When the Government of Canada announced that it would provide financial assistance to GM and GM Canada, it had already reached an agreement with GM that most of the loans provided from the Canada Account would be converted into shares of GM. Loans valued at approximately $9.8 billion were converted into 16 million preferred shares and 175 million common shares. A portion of a loan to GM Canada, $1.5 billion, was repayable.

5.53 Loan repayment. In April 2010, GM Canada repaid the government in full for its $1.5 billion loan. In May 2011, the government received Chrysler Canada’s repayment of its $1.6 billion loan.

5.54 Interest and other revenues. Loans made to Chrysler Canada and GM Canada carried interest and other compensation. Chrysler Canada paid approximately $320 million in interest and other compensation, and GM Canada paid approximately $83 million in interest. In addition, GM’s preferred shares generated $162 million in dividends between 2009 and the end of 2013. During 2014, GM continued to pay dividends on the preferred shares and began paying dividends on the common shares.

5.55 Sales of shares. In November 2010 and in September 2013, the Government of Canada sold about 65 million common shares of GM for about $2.3 billion. The governments of Canada and Ontario still own the remaining 110 million common shares and 16 million preferred shares. In Budget 2014, the government reiterated its intention to sell all the shares in an expeditious manner and maximize value for Canadian taxpayers.

Debtor-in-possession loan—Under US bankruptcy law, a loan made to a company that has filed for bankruptcy, but continues to operate its business.

5.56 Costs. We found that the financial risks of providing assistance to Chrysler were properly estimated. Chrysler Canada repaid its loan, although Chrysler’s debtor-in-possession loan of $1.28 billion, made in support of its bankruptcy, has not been repaid. However, the Government of Canada obtained approximately two percent of new Chrysler equity as compensation in the loan transaction. The government sold this entire equity to Fiat in 2011 for $132 million. This transaction reduced the total cost of Chrysler’s debtor-in-possession loan to $1.148 billion.

5.57 We found that the estimated financial risk of the assistance provided to GM has declined over time. When the federal government approved the financial assistance, the Department of Finance Canada estimated that all loans converted into shares were likely to be lost. After the loans, totalling $9.8 billion, were converted into shares, the total value of the preferred and common shares was estimated to be $3.2 billion. The difference between the original value of the loans and the estimated value of the shares—$6.6 billion—was considered lost. The federal government recorded two thirds of this loss, $4.4 billion, as an expense in the Public Accounts of Canada, 2009–10.

5.58 The final cost of the financial assistance provided to GM will be known only when all shares have been sold. At the end of our audit, $2.3 billion had been recovered through the sale of 65 million common shares. The governments still own 16 million preferred shares and 110 million common shares, and their sale will probably bring a total value that exceeds the original estimate of $3.2 billion. In that case, the final cost to the federal government and taxpayers would be lower than the expense recorded in the 2009–10 fiscal year.

5.59 These findings are important because repayments of loans, and recoveries of financial assistance from the federal government, have a direct impact on Canada’s fiscal framework and on taxpayers. The final cost of the financial assistance provided to Chrysler is largely known. The final cost of assistance provided to GM now depends on the value obtained when the company shares are sold. Paragraph 5.67 contains a recommendation related to reviewing the management of the financial assistance provided to Chrysler and GM. Appendix A includes suggested practices for monitoring financial assistance provided to private firms.

Reporting on the restructuring assistance

5.60 We examined the information publicly reported by the responsible entities regarding the restructuring assistance provided to Chrysler and General Motors (GM).

5.61 Overall, we found that entities reported individually on the restructuring assistance they provided, but there was no comprehensive reporting of the information to Parliament. This is important because the lack of comprehensive reporting limits the usefulness of the information. As the information is scattered across a number of separate reports, it was impossible for us to gain a complete picture of the assistance provided, the difference the assistance made to the viability of the companies, and the amounts recovered and lost.

There was no comprehensive reporting to Parliament

5.62 We reviewed the information publicly reported to determine whether financial and non-financial information on the assistance provided to Chrysler and GM was available to Parliament and Canadians, in keeping with applicable privacy and confidentiality requirements.

5.63 Based on the information that is publicly available, we found it impossible to gain a complete picture of the assistance provided, the difference the assistance made to the viability of the companies, and the amounts recovered and lost. No single entity was in charge of reporting consolidated information on the financial assistance that would cover the use of the funds, the achievement of objectives, or the viability of the companies. Although each entity involved in the financial assistance reported separately, the information is scattered among reports from various perspectives, which limits its usefulness. In our view, Industry Canada would be in the best position to report on the assistance.

5.64 This finding is important because it identifies gaps in the information publicly reported on the financial assistance provided to Chrysler and GM. Clear, complete information is essential for ensuring transparency and accountability of results. Appendix A includes suggested practices for reporting on financial assistance provided to private firms.

5.65 Recommendation. Industry Canada, in collaboration with the Department of Finance Canada, Export Development Canada, and other relevant entities, should publish a report with clear information on the financial assistance provided to Chrysler and General Motors, and on the impact the assistance had on the viability of the companies. Information on the financial assistance should include the total amounts disbursed, the use of the funds, the amounts recovered so far, the value of shares outstanding, and the cost of the financial assistance.

The Department’s response. Agreed. While the various Government of Canada departments involved in the restructuring of General Motors (GM) and Chrysler have met all formal reporting requirements, Industry Canada, in collaboration with the Department of Finance Canada and Export Development Canada will complete and publish a final report on the financial assistance provided to GM and Chrysler by the end of 2014.

Looking forward

Learning from the assistance provided to Chrysler and General Motors

5.66 In the future, the Government of Canada may again be required to provide financial assistance to a large private company or an entire economic sector. For this reason, we believe that it is important to learn from the experience of the federal government’s financial support to Chrysler and General Motors (GM).

5.67 Recommendation. Industry Canada, in cooperation with the other entities involved, should conduct a review of the management of the financial assistance provided to restructure Chrysler and General Motors and should identify lessons learned.

The Department’s response. Agreed. In the immediate aftermath of the restructurings, Industry Canada undertook to identify factors that led to our success in preventing the collapse of the automotive sector. These specific actions were recognized by the Institute of Public Administration of Canada in awarding the 2010 Silver Innovative Management Award and by the Public Service Award of Excellence 2009 in the Exemplary Contribution under Extraordinary Circumstances category, both awarded to Industry Canada. With the benefit of time, Industry Canada, in cooperation with the other entities involved, will undertake, in 2015, a review of the management of the financial assistance to restructure Chrysler and GM with a focus on identifying lessons learned.

Managing the Automotive Innovation Fund

5.68 We examined whether Industry Canada manages the Automotive Innovation Fund in a manner that takes risks into account, and whether it monitors and reports measurements of the results against the program’s objectives.

5.69 Overall, we found that Industry Canada’s assessment of each project proposal was consistent with the program’s terms and conditions, but in our opinion, its risk assessment framework is more comprehensive than required. Industry Canada has adequate information coming from progress reports and site visits to allow the progress of each project to be tracked. We found that Industry Canada has yet to use this information to determine whether the program is achieving its objectives.

Industry Canada’s risk assessments were consistent with the program’s requirements

5.70 According to the Treasury Board’s Policy on Transfer Payments, departments need to design, deliver, and manage transfer payment programs in a manner that takes risks into account. In particular, administrative requirements on applicants and recipients need to be proportionate to the level of risks specific to the program, the materiality of the funding, and the risk profile of the applicants and recipients.

5.71 For the Automotive Innovation Fund and the six projects funded to date, we examined whether the process that Industry Canada has in place to assess projects takes risks into account. We did not examine the negotiations between the Department and potential recipients to determine the percentage of reimbursement and the total amount of assistance provided by the program.

5.72 The project proposals originate with the companies. Industry Canada receives applications and assesses them according to the program’s terms and conditions. This assessment covers each project’s financial and technical risks as well as its potential environmental, economic, and innovation benefits to Canada.

5.73 Industry Canada assessed one of the project proposals with the assistance of officials from other federal entities, and it hired contractors to assess the other five proposals. We found that these assessments were consistent with the Automotive Innovation Fund’s terms and conditions. However, in our opinion, these terms and conditions, and the supporting assessment process for determining the suitability of a project, covered risks that were already covered by the program’s design.

5.74 The Automotive Innovation Fund is proposal-driven and requires a minimum investment of $75 million over five years. So far, the projects have been proposed by large and well-established companies that already determined that their projects were technically feasible and financially viable. In addition, the program reimburses a defined percentage of actual eligible costs based on progress made and supporting documents. Therefore, funds are disbursed only after the recipient has invested its own money. Furthermore, the support is unconditionally repayable. This means that the repayment of the contribution does not depend on the success of the proposed project. Finally, for projects presented by Canadian subsidiaries, the repayment is guaranteed by larger affiliated companies, which minimizes the government’s risk of not being repaid.

5.75 This finding is important because project assessments must take into account the risk profile of the projects and the potential recipients. The Department could streamline its risk analysis, given that potential recipients assume all of the technical risks, and most of the financial risks, associated with their projects.

5.76 Recommendation. Industry Canada should review its management procedures for the Automotive Innovation Fund to ensure that risk profiles of projects and applicants are taken into account during project assessment.

The Department’s response. Agreed. Industry Canada will continue to assess project proposals to the Automotive Innovation Fund as outlined in the program’s terms and conditions, including risks to government and risks inherent to funding automotive projects. The Department has reviewed its risk framework for assessing projects and will use this framework to ensure the risk profiles of projects and applicants are taken into account during project assessments.

Industry Canada adequately monitors projects, but has yet to use this information to assess program performance and report on results

5.77 According to the Treasury Board’s Policy on Transfer Payments, departments must have performance measurement and reporting systems in place to manage transfer payments.

5.78 We examined whether Industry Canada collected information to assess whether the Automotive Innovation Fund was meeting its stated objectives related to environmental, economic, and innovation benefits. We looked at the first five projects for which reports are currently provided to the Department. We focused on the progress reports submitted with payment claims, the annual performance reports provided by the companies, and the site visit reports prepared by the Department. We also examined whether Industry Canada has reported publicly on the program’s performance against the program’s objectives.

5.79 Monitoring. We found that Industry Canada has adequate information coming from progress reports and site visits to track the progress of each project. However, we also found that the Department has limited information on the results of the Automotive Innovation Fund measured against its objectives, which focus on the environmental, economic, and innovation benefits expected from the projects and on Canadian competitiveness.

5.80 Industry Canada monitors the results of individual projects through various means. As required in the contribution agreements, recipients send the Department annual performance reports on specific areas, such as environmental benefits, jobs, intellectual property rights, and collaboration with universities and research institutions. To report this information, recipients use templates provided by the Department. However, except for the 2012 program evaluation, the Department has not consolidated the information it receives to determine whether the program is achieving its objectives.

5.81 In 2012, Industry Canada completed an evaluation of the Automotive Innovation Fund. Although the evaluation had limitations, it concluded that the program had largely achieved the immediate outcomes, such as awareness of the program among eligible companies and improved coordination with Ontario. The evaluation also concluded that the program was on track to achieve its intermediate outcomes, which include having a positive impact on economic activity and fuel efficiency. However, it was too early to conclude on the program’s final outcomes related to environmental, economic, and innovation benefits and the competitiveness of the automotive sector in Canada.

5.82 Reporting. We found that Industry Canada did not publicly report on the environmental, economic, and innovation benefits of the Automotive Innovation Fund or on how the program contributes to the competitiveness of the automotive sector in Canada.

5.83 The Department reports on two performance indicators for the program: the number of projects funded, and the leverage of private sector investment. Reporting on the number of projects funded does not indicate whether the program and projects are bringing the expected benefits to Canada, or whether they contribute to the competitiveness of the automotive sector. Furthermore, Industry Canada reports leverage as dollars of private sector investment per dollar of project funding. However, this leverage is directly linked to the negotiated percentage of investment to be reimbursed by the Automotive Innovation Fund. It also assumes that all project investments are attributable to the program’s money, whereas investments actually depend on various factors. These two indicators reported by Industry Canada provide little information on the program’s economic benefits, and no information on its environmental or innovation benefits, or on its contributions to the competitiveness of the automotive sector.

5.84 In summary. Industry Canada has adequate information to track the progress of each project. However, the Department has limited information on the results of the Automotive Innovation Fund measured against its objectives. The two indicators used for public reporting provide little information on the program’s economic benefits, and no information on its innovation or environmental benefits, or on its impact on the competitiveness of the automotive sector.

5.85 These findings are important because Industry Canada collected information on indicators, but has not used it systematically to determine whether the program is meeting its objectives. Furthermore, the program is based on the fact that environmental, economic, and innovation benefits, and competitiveness of the automotive sector, are significant to the Canadian economy, but the information that Industry Canada currently reports publicly is not related to these expected benefits.

5.86 Recommendation. Industry Canada should continue to monitor the performance of the projects and should use this information to determine whether the Automotive Innovation Fund is achieving its objectives of bringing environmental, economic, and innovation benefits to Canada and fostering competitiveness of the automotive sector. It should also report on the program’s results.

The Department’s response. Agreed. While the 2012 evaluation found that the Automotive Innovation Fund was on track to achieve its intermediate outcomes, it was too early to assess whether the program was meeting its long-term objectives. Industry Canada has monitored, and will continue to monitor, the performance of the Automotive Innovation Fund projects, and will use the information to determine whether the program is achieving its long-term objectives of bringing environmental, economic, and innovation benefits to Canada and fostering competitiveness of the automotive sector. Industry Canada will report on program results once it has the information to do so in a comprehensive manner, as part of the program evaluation currently scheduled in its departmental evaluation plan for 2017–18.

Conclusion

5.87 The financial assistance provided to Chrysler and General Motors (GM) for their restructuring involved complex transactions, high uncertainty, and tight time frames during its development and execution. These circumstances had an impact on what Industry Canada could do to manage this assistance.

5.88 Nonetheless, we concluded that Industry Canada, the Department of Finance Canada, and Export Development Canada managed the financial support to the automotive sector in a way that contributed to the viability of the companies and the competitiveness of the sector in Canada over the short and medium terms. Industry Canada adequately assessed the recovery prospects of Chrysler and GM and monitored the companies’ production commitments in Canada. It also adequately tracked the progress of projects funded through the Automotive Innovation Fund. However, we did identify some weaknesses in the management and reporting of assistance. For example, Industry Canada did not have final restructuring plans for the companies in Canada and there was no comprehensive reporting of restructuring assistance information to Parliament.

5.89 The Department of Finance Canada adequately estimated the financial risks of providing financial assistance to Chrysler and GM. Export Development Canada adequately administered and executed the loans and associated documents for the financial assistance.

About the Audit

The Office of the Auditor General’s responsibility was to conduct an independent examination of support to the automotive sector to provide objective information, advice, and assurance to assist Parliament in its scrutiny of the government’s management of resources and programs.

All of the audit work in this chapter was conducted in accordance with the standards for assurance engagements set out by the Chartered Professional Accountants of Canada (CPA) in the CPA Canada Handbook—Assurance. While the Office adopts these standards as the minimum requirement for our audits, we also draw upon the standards and practices of other disciplines.

As part of our regular audit process, we obtained management’s confirmation that the findings reported in this chapter are factually based.

Objectives

The audit examined whether Industry Canada, the Department of Finance Canada, and Export Development Canada, consistent with their respective responsibilities, managed the financial support to the automotive sector in a way that contributed to the viability of the companies and the competitiveness of the sector in Canada. The audit had the following sub-objectives:

- to determine whether Industry Canada, the Department of Finance Canada, and Export Development Canada, consistent with their respective responsibilities, have adequately managed and reported on the financial assistance provided for Chrysler’s and General Motors’ (GM’s) restructuring; and

- to determine whether Industry Canada manages the Automotive Innovation Fund in a risk-based manner that demonstrates results and is transparent.

Scope and approach

To examine how Industry Canada, the Department of Finance Canada, and Export Development Canada managed the financial assistance to restructure Chrysler and GM, according to their respective responsibilities, we examined

- the analysis of risks,

- the setting of the loans’ terms and conditions in accordance with objectives and risks of restructuring,

- the overseeing of the loans, and

- the monitoring of conditions.

To examine the reporting of financial assistance, we observed whether sound financial and non-financial performance information was available to Parliament and the Canadian public, within the context of applicable privacy and confidentiality requirements.

The audit examined the Automotive Innovation Fund program as a whole and the six projects funded to date. It included the role of Industry Canada and, more specifically, the Automotive and Transportation Industries Branch and the Industrial Technologies Office within Industry Canada. We did not examine the negotiations between the Department and the potential recipients in which the amount of assistance and the percentage of reimbursement were determined.

The audit included an examination of documents related to restructuring plans, loans, and the monitoring of commitments, as well as interviews with entity officials. It also included an examination of key documents and correspondence related to the Automotive Innovation Fund, and interviews with Department officials and representatives of some of the program’s recipients. We interviewed representatives of Chrysler Canada, GM Canada, and the union (CAW/Unifor), as well as two recipients of the Automotive Innovation Fund.

Our conclusions regarding management practices and actions apply only to public servants in the federal government. We did not audit the records of the private sector companies, the Government of Ontario, or the US Government. Consequently, our conclusions cannot and do not pertain to the companies’ practices or performance, or to the work of other governments.

Criteria

To determine whether Industry Canada, the Department of Finance Canada, and Export Development Canada, consistent with their respective responsibilities, have adequately managed and reported on the financial assistance provided for Chrysler’s and General Motors’ restructuring, we used the following criteria:

| Criteria | Sources |

|---|---|

|

Industry Canada, the Department of Finance Canada, and Export Development Canada make decisions based on review and analysis of relevant information. |

|

|

Industry Canada, the Department of Finance Canada, and Export Development Canada identify risks and implement mechanisms to mitigate them. |

|

|

Industry Canada and Export Development Canada monitor the implementation of terms and conditions of loan agreements to ensure compliance. |

|

|

Industry Canada and the Department of Finance Canada publicly report relevant information in a timely manner. |

|

To determine whether Industry Canada manages the Automotive Innovation Fund in a risk-based manner that demonstrates results and is transparent, we used the following criteria:

| Criteria | Sources |

|---|---|

|

Industry Canada has an appropriate process to select the projects to fund under the Automotive Innovation Fund. |

|

|

Industry Canada manages the Automotive Innovation Fund in a manner that takes risks into account. |

|

|

Industry Canada has sufficient information to assess whether the Automotive Innovation Fund is meeting its stated objectives related to environmental, economic, and innovation benefits. |

|

|

Industry Canada reports publicly on the stated objectives of the Automotive Innovation Fund related to environmental, economic, and innovation benefits. |

|

Management reviewed and accepted the suitability of the criteria used in the audit.

Period covered by the audit

For restructuring support, the audit covered the period from December 2008 to May 2014 (the end of the examination phase).

For the Automotive Innovation Fund, the audit covered the period from February 2008, when the program began, to May 2014, when the examination phase ended.

Audit work for this chapter was completed on 26 September 2014.

Audit team

Assistant Auditor General: Jerome Berthelette

Principal: Richard Domingue

Director: André Côté

Sophie Chen

Kathryn Nelson

Eric Provencher

Stephanie Taylor

For information, please contact Communications at 613-995-3708 or 1-888-761-5953 (toll-free).

Hearing impaired only TTY: 613-954-8042

Appendix A—Managing financial support to private sector firms

The following table outlines elements that should be present when the Government of Canada considers a request for financial assistance from a large private company, and when it monitors and reports on it.

| Element | Minimum requirements |

|---|---|

|

Planning |

When a private sector company in financial difficulty requests public assistance, federal government entities should ensure that the following conditions are in place:

|

|

Monitoring |

Government entities should monitor the implementation of the restructuring plan and the use of public funds to ensure that the actions considered necessary for restoring the company’s viability have been taken. They should also assess whether these actions are producing the expected results. Monitoring should include whether funds were used for their intended purposes. |

|

Public reporting |

Canadians and parliamentarians need to know

The responsibility for reporting this information should be clearly assigned, and the use of public funds reported transparently, so that government entities and the public understand the impact of the financial assistance on the company’s short- and long-term viability. |

Appendix B—List of recommendations

The following is a list of recommendations found in Chapter 5. The number in front of the recommendation indicates the paragraph where it appears in the chapter. The numbers in parentheses indicate the paragraphs where the topic is discussed.

Reporting on the restructuring assistance

| Recommendation | Response |

|---|---|

|

5.65 Industry Canada, in collaboration with the Department of Finance Canada, Export Development Canada, and other relevant entities, should publish a report with clear information on the financial assistance provided to Chrysler and General Motors, and on the impact the assistance had on the viability of the companies. Information on the financial assistance should include the total amounts disbursed, the use of the funds, the amounts recovered so far, the value of shares outstanding, and the cost of the financial assistance. (5.62–5.64) |

Agreed. While the various Government of Canada departments involved in the restructuring of General Motors (GM) and Chrysler have met all formal reporting requirements, Industry Canada, in collaboration with the Department of Finance Canada and Export Development Canada will complete and publish a final report on the financial assistance provided to GM and Chrysler by the end of 2014. |

Looking forward

| Recommendation | Response |

|---|---|

|

5.67 Industry Canada, in cooperation with the other entities involved, should conduct a review of the management of the financial assistance provided to restructure Chrysler and General Motors and should identify lessons learned. (5.66) |

Agreed. In the immediate aftermath of the restructurings, Industry Canada undertook to identify factors that led to our success in preventing the collapse of the automotive sector. These specific actions were recognized by the Institute of Public Administration of Canada in awarding the 2010 Silver Innovative Management Award and by the Public Service Award of Excellence 2009 in the Exemplary Contribution under Extraordinary Circumstances category, both awarded to Industry Canada. With the benefit of time, Industry Canada, in cooperation with the other entities involved, will undertake, in 2015, a review of the management of the financial assistance to restructure Chrysler and GM with a focus on identifying lessons learned. |

Managing the Automotive Innovation Fund

| Recommendation | Response |

|---|---|

|

5.76 Industry Canada should review its management procedures for the Automotive Innovation Fund to ensure that risk profiles of projects and applicants are taken into account during project assessment. (5.70–5.75) |

Agreed. Industry Canada will continue to assess project proposals to the Automotive Innovation Fund as outlined in the program’s terms and conditions, including risks to government and risks inherent to funding automotive projects. The Department has reviewed its risk framework for assessing projects and will use this framework to ensure the risk profiles of projects and applicants are taken into account during project assessments. |

|

5.86 Industry Canada should continue to monitor the performance of the projects and should use this information to determine whether the Automotive Innovation Fund is achieving its objectives of bringing environmental, economic, and innovation benefits to Canada and fostering competitiveness of the automotive sector. It should also report on the program’s results. (5.77–5.85) |

Agreed. While the 2012 evaluation found that the Automotive Innovation Fund was on track to achieve its intermediate outcomes, it was too early to assess whether the program was meeting its long-term objectives. Industry Canada has monitored, and will continue to monitor, the performance of the Automotive Innovation Fund projects, and will use the information to determine whether the program is achieving its long-term objectives of bringing environmental, economic, and innovation benefits to Canada and fostering competitiveness of the automotive sector. Industry Canada will report on program results once it has the information to do so in a comprehensive manner, as part of the program evaluation currently scheduled in its departmental evaluation plan for 2017–18. |

PDF Versions

To access the Portable Document Format (PDF) version you must have a PDF reader installed. If you do not already have such a reader, there are numerous PDF readers available for free download or for purchase on the Internet: