2023 November Report of the Auditor General of Canada to the Parliament of CanadaEnvironmental and Social Review Directive—Export Development Canada

Independent Auditor’s Report

Table of Contents

- Introduction

- Findings and Recommendations

- Export Development Canada implemented most of the requirements of the directive, but project risk monitoring was incomplete

- The directive was not often applied, supporting transactions through other review processes with varying due diligence

- Public reporting on projects reviewed under the directive lacked transparency

- Conclusion

- About the Audit

- Recommendations and Responses

- Exhibits:

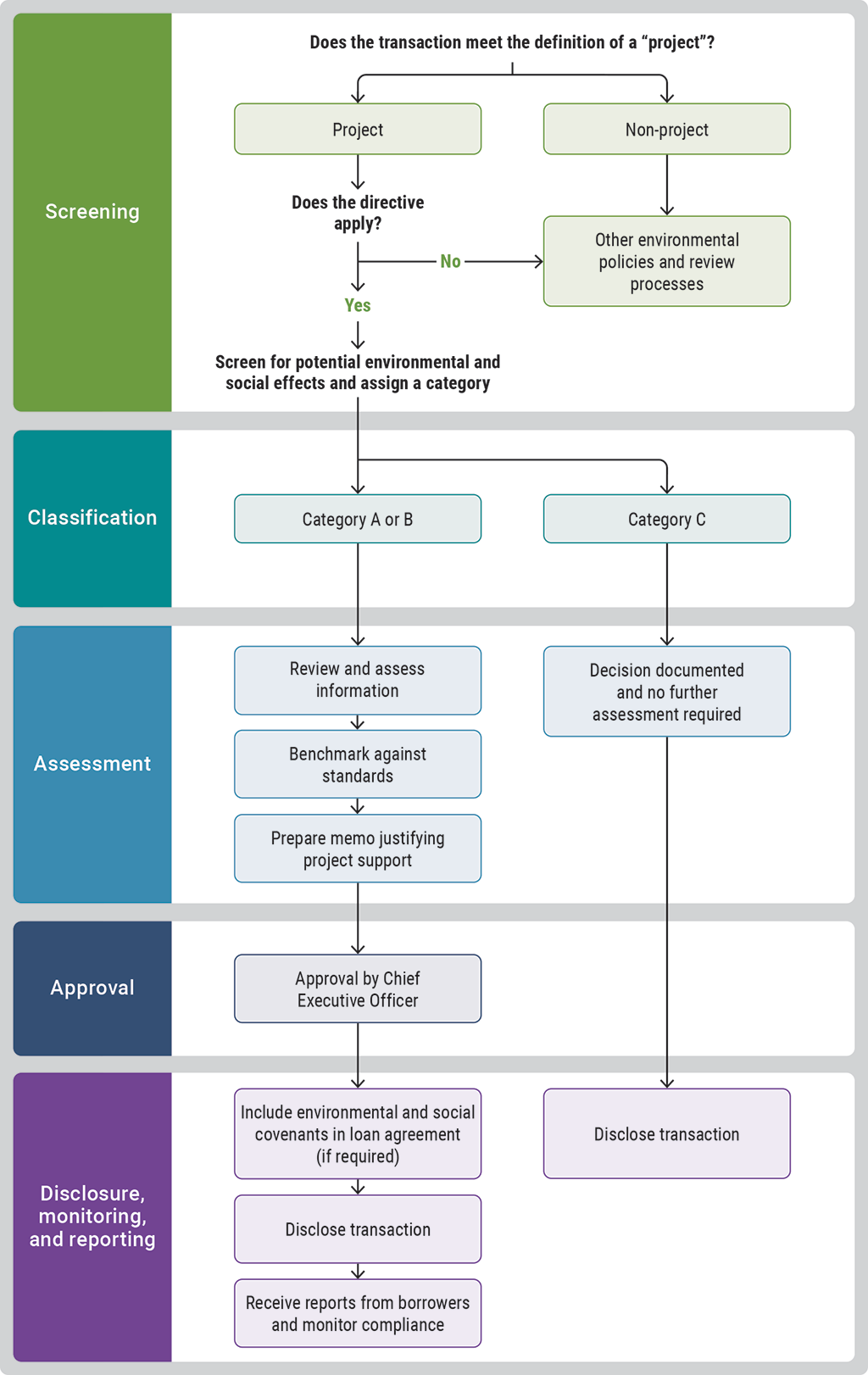

- 1—How Export Development Canada applies the Environmental and Social Review Directive to transactions

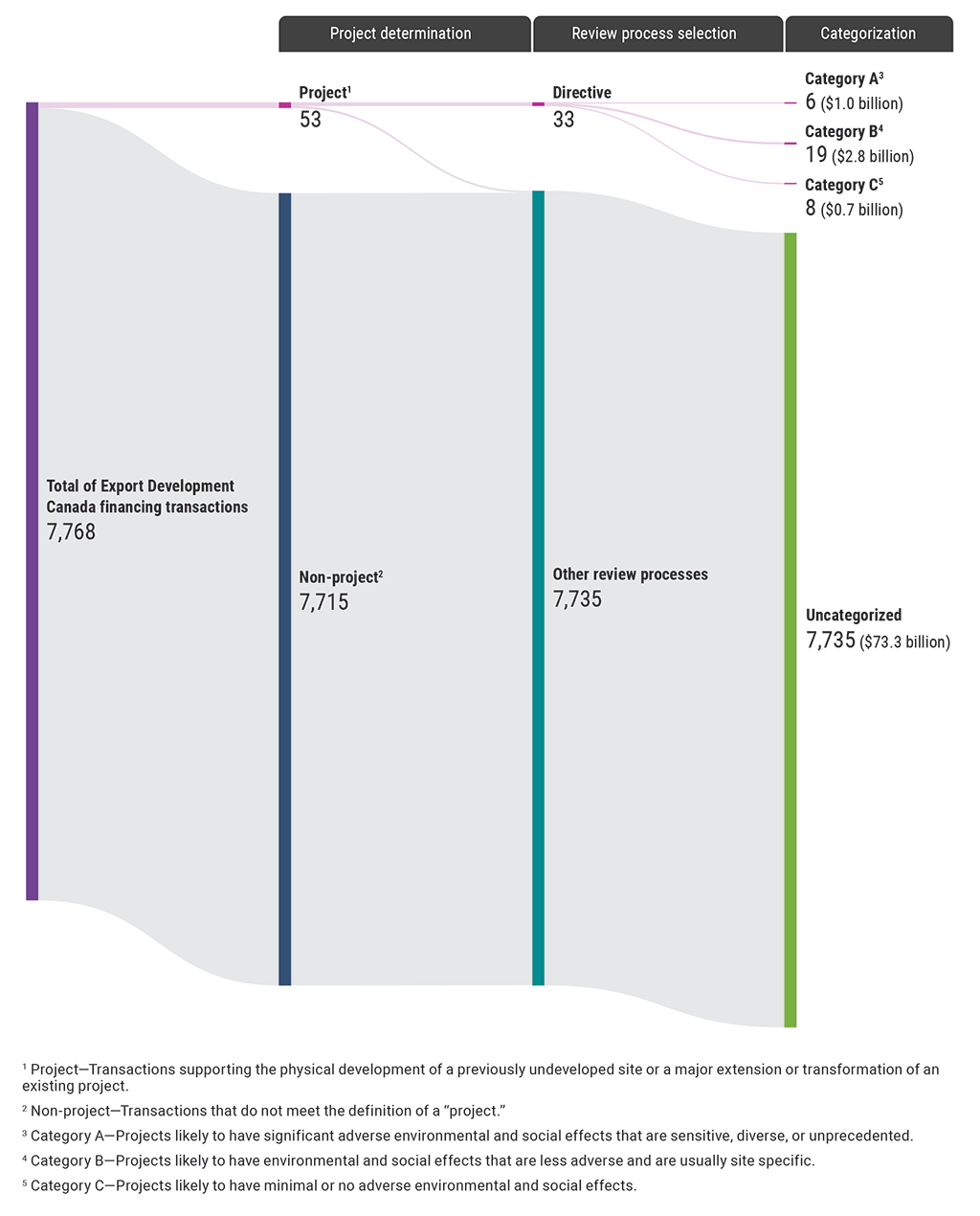

- 2—Only 33 out of 7,768 transactions were reviewed under the Environmental and Social Review Directive during our audit period

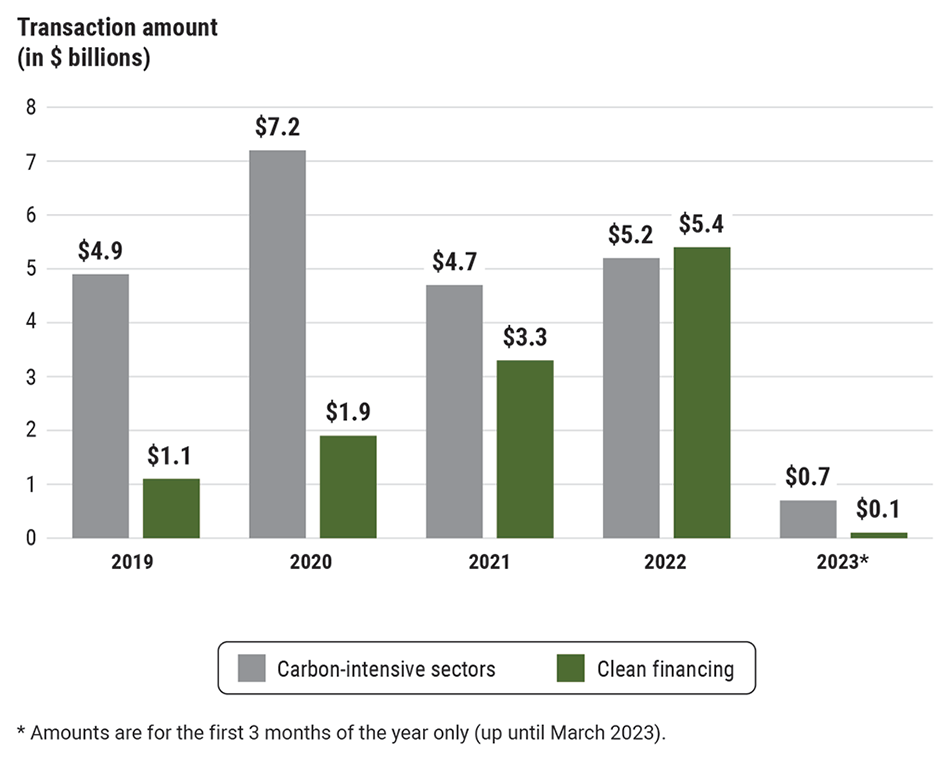

- 3—The corporation increased support for clean financing but continued to support carbon-intensive sectors

Introduction

Background

1. Export Development Canada is Canada’s official export credit agency. Established in 1969, the mandate of this Crown corporation is to support and develop Canada’s export trade and Canada’s capacity to respond to international business opportunities. The corporation does this by providing loans and insurance products.

2. The corporation operates under guidelines and principles similar to those used by other export credit agencies and financial institutions that provide similar services. These agencies are a major source of international public financing for large‑scale infrastructure and resource extraction projects. These projects have a high level of complexity and uncertainty, and borrowers often request support from multiple lenders at the early, conceptual stages of a project.

3. As a Crown corporation, Export Development Canada is owned by the Government of Canada and backed by the federal government’s credit rating. However, it is financially self‑sustaining and does not receive ongoing government funding. To achieve its business objectives, the corporation prices its products and services on the global market and manages its own risks. Its purposes and powers are established by the Export Development Act and the Export Development Canada Exercise of Certain Powers Regulations.

4. Since 2001, the Export Development Act has required the corporation to carry out environmental reviews of the projects it supports. The first Environmental Review Directive was issued by the corporation’s Board of Directors in 2001. It was amended in 2010 to become the Environmental and Social Review Directive and revised again in February 2019 and October 2022.

5. This directive sets out the process, as seen in Exhibit 1, through which the corporation determines whether there are adverse environmental and social (human rights) effects that may result from a transaction, and if so, whether the corporation is justified in supporting it. The directive does not apply to all transactions. Only transactions that meet the definition of a “project” are considered for review under the directive. The directive defines a project as one of the following:

- a transaction supporting the physical development of a previously undeveloped site

- a major extension or transformation of an existing project

The directive then only applies to projects that have a repayment or coverage term of 2 years or more, and that either have a value of more than American dollarsUS$10 million or that are located in or near a sensitive area. Sensitive areas include national parks and other protected areas and locations such as wetlands, forests with high biodiversity, and areas of importance for Indigenous peoples.

Exhibit 1—How Export Development Canada applies the Environmental and Social Review Directive to transactions

Source: Adapted from Export Development Canada’s Environmental and Social Review Directive

Exhibit 1—text version

This flowchart shows the process that Export Development Canada uses to apply the Environmental and Social Review Directive to transactions. The process includes the following stages:

- screening

- classification

- assessment

- approval

- disclosure, monitoring, and reporting

At the screening stage, the corporation determines whether the transaction meets the definition of a “project.” If not, it determines which other environmental policies and review processes apply.

If the transaction meets the definition of a project, the corporation determines whether the directive applies. If the directive does not apply, the corporation determines which other environmental policies and review processes apply.

If the directive does apply to the transaction, the corporation screens for potential environmental and social effects and assigns a category.

At the classification stage, the transaction is assigned category A, B, or C. If category C, the decision is documented and no further assessment is required.

If the transaction is assigned category A or B, then the corporation

- reviews and assesses information

- benchmarks against standards

- prepares a memo justifying its support for the project

The transaction is then sent for approval by the Chief Executive Officer.

The next stage is disclosure, monitoring, and reporting. At this stage, the corporation

- includes environmental covenants in the loan agreement (if required)

- discloses the transaction

- receives reports from borrowers and monitors compliance

The corporation discloses transactions for category A, B, and C transactions.

6. On the basis of the preliminary information the corporation gathers, it categorizes projects according to their potential adverse environmental and social effects:

- Category A. Projects likely to have significant adverse environmental and social effects that are sensitive, diverse, or unprecedented. The effects may extend beyond the project site and be irreversible.

- Category B. Projects likely to have environmental and social effects that are less adverse and usually site specific. Few if any of the effects are irreversible, and in most cases, mitigation measures can be designed to address them.

- Category C. Projects likely to have minimal or no adverse environmental and social effects.

These categories are based on international standards and determine whether further information, assessment, and justification are required.

7. Under the Export Development Act, the Auditor General of Canada must audit the design and implementation of the corporation’s Environmental and Social Review Directive at least once every 5 years. This is our sixth audit report on the directive.

8. Since our 2019 audit, the Government of Canada has taken additional steps toward meeting the requirements of the Paris Agreement, which it ratified in 2016. This agreement seeks to limit global average temperature rise to well below 2 degrees Celsius, and preferably to 1.5 degrees Celsius, compared with pre‑industrial levels. The federal government has also signed on to the United Nations’ 2030 Agenda for Sustainable Development in 2015, which is a global call to action to contribute to the United Nations’ Sustainable Development Goals.

9. In both 2021 and 2022, the Minister of International Trade, Export Promotion, Small Business and Economic Development (2021 title) provided guidance to the corporation through the annual Statement of Priorities and Accountabilities. This guidance emphasized that the corporation must consider the environmental impact of all of its business decisions to have them better align with Government of Canada commitments related to climate change. The guidance also encouraged the corporation to take a more ambitious approach to reducing support for carbon-intensive projects by considering the emissions of its entire portfolio and by providing financial support only to fossil fuel transactions involving Canadian companies. The federal government also requested that Crown corporations adopt the recommendations of the Task Force on Climate-Related Financial Disclosures. The corporation is expected to disclose its financial risks, strategy, governance, and measurements related to climate change.

10. The corporation developed the following additional strategies to align itself with federal and international commitments:

- Climate Change Policy. In 2022, the corporation adopted its latest Climate Change Policy, which guides its approach to its climate-change-related risks and opportunities.

- Net-zero commitment. The corporation aims to achieve net‑zero emissions across its business lines and operations by 2050, a goal aligned with the Government of Canada and the Paris Agreement. It has set an early target to contribute to this goal—the reduction of the funding it provides to its 6 most carbon-intensive sectors by 40% below 2018 levels by 2023.

11. The corporation also has procedural guidance and tools for performing due diligence, a process in which it identifies potential environmental and social risks and works with borrowers to help mitigate these risks. Many of its policies, procedures, and tools were updated or only began to be used during our audit period. In 2019, the corporation began using new forms for early identification and assessment of risk factors. It implemented a pre‑screening tool to flag transactions that may require additional due diligence for environmental and social risk management. The corporation’s Environmental, Social and Governance team also began using a tool to assess corporate- and industry-specific environmental and social risks.

Focus of the audit

12. This audit focused on whether the design of Export Development Canada’s Environmental and Social Review Directive was suitable, whether its requirements are being implemented, and whether it is aligned with Government of Canada environmental and social commitments.

13. This audit is important because, as Canada’s export credit agency, the corporation, depending on its course of action, can contribute to or detract from achieving Canada’s environmental and social commitments. This includes efforts to keep global temperature rise below 2 degrees Celsius, and preferably to 1.5 degrees Celsius, compared with pre‑industrial levels. By complying with internationally recognized environmental and social standards, which are increasingly emphasizing sustainable economic activity, the corporation can contribute to these efforts.

14. More details about the audit objective, scope, approach, and criteria are in About the Audit at the end of this report.

Findings and Recommendations

Export Development Canada implemented most of the requirements of the directive, but project risk monitoring was incomplete

15. This finding matters because Export Development Canada is required by legislation to implement the Environmental and Social Review Directive. Implementing it correctly is one of the critical processes through which the corporation can ensure that it manages the environmental and social risks of the projects it supports.

16. This finding also matters because environmental and social risks may only materialize once a project is underway, after loan agreements are finalized. Project risk monitoring helps mitigate any emerging environmental and social risks that may result from a project.

17. The Environmental and Social Review Directive exists within the corporation’s broader Environmental and Social Risk Management Policy Framework, which has the following policies:

- Environmental and Social Risk Management Policy

- Climate Change Policy

- Human Rights Policy

- Transparency and Disclosure Policy

18. The directive outlines the process the corporation must follow when assessing the environmental and social effects of its projects. Exhibit 1 shows the steps performed when the corporation conducts a review of a project under the directive.

Compliant implementation of the directive requirements

19. We found that the corporation implemented the requirements of the directive. We examined a random sample of 22 projects that underwent a review under the directive. We also examined 11 projects and 20 non‑projects that did not meet the criteria for a directive review and that were assessed through a non‑directive review process.

20. We found that in our sample of 22 projects reviewed under the directive, the following steps were correctly implemented:

- The screening process was followed to identify projects within the scope of the directive.

- Projects were assigned a category, and a rationale for the category was documented.

- Projects included the environmental and social impact assessments or other documentation as required and showed additional due diligence taken with a final assessment decision documented.

- Approvals were signed by the Chief Executive Officer or delegated authority.

- Projects that were assigned a category were disclosed on the corporation’s website.

21. The corporation’s procedure guide stated that site visits are generally expected for Category A projects and recommended for Category B projects. Site visits are a method for obtaining assurance that the projects complied with host country or international standards during the review process. In our sample of 17 Category A and B projects, we found that only 1 site visit was conducted during the audit period because of COVID‑19Definition 1 restrictions. The corporation told us that it also undertook virtual site visits while the pandemic restrictions were in place.

Incomplete monitoring of projects’ environmental and social risks

22. The corporation can negotiate loan conditions that require borrowers to establish and report on environmental or social commitments. In turn, the corporation monitors the borrowers’ reports and takes corrective action when necessary. We found that the corporation generally received the required reports from borrowers but did not always monitor them. This posed the risk that emerging adverse effects from projects disclosed in borrower reporting would not be mitigated through corrective action.

23. Our previous audit reports also noted this weakness. The corporation told us that it continued to lack the capacity to prioritize monitoring borrower reports. For this review, our previous recommendations remain relevant.

No integrated case management system

24. We found that the corporation did not use an integrated case management system to manage its environmental and social reviews. Information was housed in different databases and applications or on shared drives in folders that were not integrated. This resulted in gaps and inconsistencies in the data.

25. In the transactions we examined in our sample, we found that the corporation continued to use manual inputting for entering covenants from loan agreements and borrower reports into various tracking systems. In some cases, this resulted in reports being received late with limited follow‑up by the corporation. For example, we found 1 instance where the corporation’s Environmental, Social and Governance Advisory team had received reporting from a borrower, but the Covenants Officer responsible for monitoring loan compliance was not aware of it.

26. Our 2014 audit also pointed out that manual inputting made the corporation’s tracking subject to human errors or omissions. In our view, an integrated case management system would allow the corporation to store all documents related to transactions in 1 place and conduct quality assurance. It would also facilitate better collaboration, provide better access to information, increase efficiency, and improve oversight of the transaction review process.

27. To improve its environmental and social review processes, Export Development Canada should implement an integrated case management system and a quality assurance process to minimize errors.

The corporation’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

The directive was not often applied, supporting transactions through other review processes with varying due diligence

28. This finding matters because when the Environmental and Social Review Directive is not applied, Export Development Canada could be providing funding for projects without being fully aware of their environmental and social risks. These risks could include human rights violations, increased greenhouse gas emissions, and loss of biodiversity.

29. The corporation designed the directive using the Organisation for Economic Co‑operation and Development’s Recommendation of the Council on Common Approaches for Officially Supported Export Credits and Environmental and Social Due Diligence (generally referred to as the “Common Approaches”) and the Equator Principles. These are internationally recognized standards used by other export credit agencies to provide the minimum guidance for safeguards against environmental and social risks, allowing for a common baseline.

30. As shown in Exhibit 1, the screening process includes

- determining whether the transaction is a project or non‑project

- determining whether the project meets the screening criteria for a review under the directive

- reviewing sector, country, and media search results for any environmental and social risks associated with the borrowers

- assessing whether social or environmental risks need further consideration

Narrow screening requirements for the directive

31. We found that the scope of the directive was narrow and applied to only a small percentage of the transactions the corporation supported. This was partly because the corporation used a narrow definition of “project” in the directive. As shown in Exhibit 2, this resulted in only 33 completed transactions being reviewed under the directive. In our 2019 audit, we pointed out ways to broaden the scope of the directive by more closely aligning it with the Common Approaches and the Equator Principles. In our review of the Common Approaches and the Equator Principles for this audit, we still found that the definitions of “project” in international standards were broader than the definition in the directive. The broader definitions in the standards included other types of transactions that could have environmental and social risks, such as

- export of capital goods or services or both

- construction at developed sites, not just previously undeveloped sites

- any type of project extension, not just major project extensions

Exhibit 2—Only 33 out of 7,768 transactions were reviewed under the Environmental and Social Review Directive during our audit period

Exhibit 2—text version

This chart shows how the corporation’s assessment process resulted in most of the 7,768 financing transactions being excluded from review under the Environmental and Social Review Directive. The corporation determined that only 53 transactions met the definition of a project. A project is a transaction supporting the physical development of a previously undeveloped site or a major extension or transformation of an existing project. The corporation then determined that the directive applied to only 33 projects. It classified these 33 projects as follows:

- 6 were classified as Category A and were valued at $1.0 billion. Category A projects are likely to have significant adverse environmental and social effects that are sensitive, diverse, or unprecedented.

- 19 were classified as Category B and were valued at $2.8 billion. Category B projects are likely to have environmental and social effects that are less adverse and are usually site specific.

- 8 were classified as Category C and were valued at $0.7 billion. Category C projects are likely to have minimal or no adverse environmental and social effects.

The total number of Export Development Canada financing transactions during our audit period was 7,768 transactions. During project determination, the corporation determined that 7,715 transactions were non-projects.

During review selection, the corporation determined that the directive did not apply to 7,735 transactions. For these transactions, the corporation determined that other review processes applied. Because the directive did not apply to these transactions, they were not categorized. These transactions were valued at $73.3 billion. In comparison, the projects that were selected for review under the directive were valued at $4.5 billion.

32. We found that the corporation used a list of non‑projects (transactions that do not meet the definition of “project”) to determine whether to exclude a transaction from a review under the directive. In our sample of 20 non‑projects, we observed transactions with environmental and social risks that were excluded from a review under the directive. For example, more than $300 million was given to a company purchasing aircrafts, which emit greenhouse gases. However, the transaction was not reviewed under the directive because the purchasing of equipment was included in the corporation’s non‑project list.

33. When a transaction was determined to be a project, the application of the directive was further narrowed. Although a transaction may have had environmental and social risks, if it did not meet one of the screening criteria, it would still be excluded from a review under the directive. As a result, a small number of completed transactions were subject to the environmental and social review directive. Between 1 May 2019 and 31 March 2023, out of 7,768 total transactions, 53 were initially identified as projects, but only 33 (0.4%) were subject to a review under the directive. Of the 33 approved transactions, 6 were Category A, 19 were Category B, and 8 were Category C projects. These reviewed transactions represented $4.5 billion (5.9%) of the $77.9 billion in total funding loaned to borrowers during this period (Exhibit 2).

34. The directive also included the following exceptions that would exclude a project from a review:

- The funding is for preliminary design work, a review, or a study, even if it is related to a project.

- The project is a Category C project.

- The project was previously reviewed and justified under the directive, there have been no significant changes to its scope, and there are no indications that the project is significantly non‑compliant with the environmental and social commitments in the borrower’s contract.

- The funding for the project is related to a Canada Account transactionDefinition 2, and the Government of Canada is satisfied that the requirements of the Canadian Environmental Assessment Act, 2012 have been met.

35. We found that these exceptions allowed for projects with documented environmental and social risks to be screened out from a review under the directive. For example, up to $150 million of additional funding was approved for an oil and gas project without a new review under the directive. Despite the additional funding, this was considered an exception because the corporation determined that the project scope had not changed and there was no significant non‑compliance with environmental and social commitments.

36. The directive sets out the conditions that allow the corporation to justify approving a project after the project is assessed and mitigation measures are documented. The corporation can use any of the 3 following conditions:

- adverse environmental and social effects are not significant in the corporation’s view

- the corporation is satisfied that the project meets or exceeds internationally recognized good practices, guidelines, or standards

- the project represents an opportunity to improve environmental conditions above baseline conditions.

We found that the conditions to approve a project had undergone minimal revisions since the first version of the directive in 2001. As a result, the corporation could still justify support for Category A or B projects under the directive with potential adverse environmental and social effects.

37. Building on our previous 2019 recommendation, to minimize the environmental and social effects of transactions, Export Development Canada should expand the scope of its Environmental and Social Review Directive by

- broadening its definition of a project to better align with the Organisation for Economic Co‑operation and Development Common Approaches and with the Equator Principles

- revising the exceptions in the directive to ensure that high‑risk transactions (for example, additional funding for existing projects) are not excluded from a directive review

- reassessing the justifications permitted in the directive to enter into a transaction with a high risk of adverse social or environmental effects, despite the implementation of mitigation measures

The corporation’s response. Partially agreed.

See Recommendations and Responses at the end of this report for detailed responses.

Varying levels of due diligence for transactions

38. For Category A and B projects, the directive requires specific due diligence. This includes identifying and assessing project risks related to human rights, climate, and specific sectors. This process is supported by gathering documentation, benchmarking (evaluating against a set standard), site visits, and work by independent consultants. In our sample of 22 projects reviewed under the directive, we found that the required due diligence was completed.

39. At the benchmarking stage (Exhibit 1), the corporation may apply the International Finance Corporation Performance Standards. These are 8 standards for identifying, evaluating, and mitigating environmental and social risks related to labour and working conditions, biodiversity, heritage, and Indigenous peoples. These standards are often more stringent than a host country’s standards, so projects benchmarked against them are more rigorously reviewed. However, we found that the corporation benchmarked projects against the International Finance Corporation Performance Standards in only a small number of cases and most often applied the host country standards. This concern was also raised in our 2019 audit. The areas where host country standards may be less stringent include

- environmental and social management systems, plans, and assessments

- grievance mechanisms

- free, prior, and informed consent, informed consultation, and participation with Indigenous peoples throughout the project process

40. Since our last audit, the corporation has implemented new screening tools to assess transactions. We found errors made in the parts of the screening process aimed at identifying

- projects in sensitive areas (such as wetlands or forests with high biodiversity value)

- industrial sectors

- countries

- media search results

For example, through our sampling, we identified transactions for which the corporation had documentation to demonstrate that these were located in a sensitive area. However, this was not indicated in the corporation’s screening process or documented in its information system. Without proper screening and documentation, the corporation cannot have a full picture of the risks of a transaction. An incomplete picture of risks can lead to not applying the required due diligence to a transaction.

41. When a transaction did not meet the criteria for review under the directive, the corporation had a number of other environmental and social review processes, or non‑directive reviews, it could use to evaluate risks. As described in paragraph 19, we examined the 11 projects and 20 non‑projects that were not reviewed under the directive. We found that, even when risks were identified, varying levels of due diligence were conducted under these other processes than what would have been applied under the directive. For example, the corporation had identified high environmental and social risks for a $500 million loan to a borrower in the mining sector. However, the loan did not require the due diligence processes specified under the directive, such as an independent assessment or disclosure requirements, because it did not meet the definition of a project.

42. We found that the documentation to help guide the corporation’s assessment officers in conducting reviews was outdated, inconsistent, and unclear. In our examination of sample transactions, we found examples where this resulted in changes to the review procedure being used, potentially requiring the environmental and social risk assessment to begin over again. Furthermore, we found that the use of risk assessment tools was inconsistent and not coordinated.

43. In order to strengthen due diligence for transactions and projects and to ensure that decisions on project financing align with Government of Canada commitments, Export Development Canada should

- update its guidance, processes, and procedures, including the assessment of climate change risks, to better align with its environmental and social policies

- strengthen the documentation requirements for sensitive area verification, including biodiversity assessments

- when benchmarking using host country standards, document how the host country standard meets or exceeds the requirements of all relevant International Finance Corporation Performance Standards for all Category A and B projects

The corporation’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

Inconsistent project categorization for carbon-intensive sectors

44. As noted in paragraphs 8 and 9, the federal government has made a number of commitments on climate action. In our 2014 audit report, we noted that the corporation did not consistently document its assessment of greenhouse gas emission estimates for projects, making it unclear whether this environmental risk had been adequately considered in project reviews. In this audit, we found that even when greenhouse gas emission estimates were documented, the categorization assessment of projects with significant greenhouse gas emissions was inconsistent. For example, 2 transactions that had significant estimated annual greenhouse gas emissions, with more than 100,000 tonnes of carbon dioxide equivalentDefinition 3, were assessed as Category B since the effects were deemed to be site specific and not significant. Despite this high level of greenhouse gas emissions, these transactions required less due diligence compared with Category A transactions, and the full emission estimates were not disclosed.

45. We analyzed transactional data provided by the corporation and found that the corporation had increased its support for clean financing transactions. This refers to processes, products, or services that reduce negative environmental effects through significant energy efficiency improvements, the sustainable use of resources, or environmental protection activities. We also found that the corporation continued to support carbon-intensive sectors, such as aerospace, oil and gas, and mining and forestry (Exhibit 3). For this analysis, we reviewed the final industry of risk in carbon-intensive sectors for the transaction, rather than the exporter. Further information on this analysis is found in the About the Audit section.

Exhibit 3—The corporation increased support for clean financing but continued to support carbon-intensive sectors

Exhibit 3—text version

This bar chart shows support for carbon-intensive sectors and for clean financing in terms of transaction amounts from 2019 to March 2023. Overall, the carbon-intensive sectors received ongoing amounts of financial support, and the support for clean financing increased consistently since 2019.

In 2019, the corporation provided $4.9 billion to carbon-intensive sectors and $1.1 billion to clean financing.

In 2020, the corporation increased its financing to $7.2 billion to carbon-intensive sectors and provided $1.9 billion to clean financing.

In 2021, the corporation decreased its financing to $4.7 billion to carbon-intensive sectors and increased its support to $3.3 billion for clean financing.

In 2022, the corporation provided $5.2 billion to carbon-intensive sectors and increased its support to $5.4 billion for clean financing.

In the first 3 months of 2023, the corporation provided $0.7 billion to carbon-intensive sectors and $0.1 billion to clean financing.

46. Our recommendation for this section is at paragraph 43.

Public reporting on projects reviewed under the directive lacked transparency

47. This finding matters because Export Development Canada is a public entity. To have the trust of the public, its reporting must be clear and transparent in disclosing that it has adequately considered the environmental and social effects of all transactions reviewed under the Environmental and Social Review Directive.

Lack of information reported on projects

48. We noted that, in the public listing of transactions reviewed under the directive, the project value of Category A and B projects was not included. In our view, stakeholders and the public should be able to find comprehensive information on these projects in this 1 place. Instead, they must search for it in a separate individual transaction listing. Furthermore, we found that this information was not updated when funding was increased through a subsequent approval.

49. We also noted 2 areas where the corporation disclosed less information for Category B projects than for Category A projects. First, the corporation’s website did not list proposed Category B projects that were not yet approved. Doing so would give the public an opportunity to comment on them and their potential environmental and social effects. It did do this for proposed Category A projects, listing them at least 60 days before signing the approval contract. Second, the corporation did not provide the public the same detail on approved Category B projects as it did for approved Category A projects. For Category A, the corporation provided a project review summary on the directive review process, decision rationale, and key environmental and social risks identified, along with mitigation measures. These details were not disclosed for approved Category B projects. Doing so would improve transparency.

50. We found that the corporation did not disclose for all projects the estimates of greenhouse gas emissions that it had obtained during the directive review process. Reporting on greenhouse gas emissions is important for the Government of Canada to achieve its goal of net‑zero emissions by 2050 and its commitments under the Paris Agreement. The corporation’s Integrated Annual Report discloses the value of its investments in 6 carbon-intensive sectors; however, the corporation did not report the quantity of emissions resulting from the projects. In our view, reporting on these emissions would improve transparency and clearly indicate the greenhouse gas emissions related to the corporation’s investments.

51. The corporation’s website disclosed information about all individual financing transactions, including the transaction date and description; the country where the project was located; the purpose, borrower name, and industry sector; and the range of funding provided. Individual transactions were disclosed in separate portable document formatPDF files for each year, and the information tables could not be filtered, nor were original data sets available. This makes data analysis difficult for interested stakeholders.

52. To increase transparency and facilitate the ability of stakeholders to analyze the corporation’s support of projects, Export Development Canada should disclose

- the initial and subsequent amounts of funding provided for projects on its listing of transactions reviewed under the Environmental and Social Review Directive

- information on Category B transactions prior to approving them and then a project review summary after approving them, as it does for Category A transactions

- greenhouse gas emissions and emission estimates for all projects reviewed under the directive

- data on individual transactions in a machine-readable format that facilitates analysis

The corporation’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

Conclusion

53. We concluded that the design of some elements of Export Development Canada’s Environmental and Social Review Directive were not suitable. The directive was narrow in its application and allowed for transactions with similar environmental and social risks to be approved with varying levels of due diligence. In addition, the financing of projects with high greenhouse gas emissions may not align with Government of Canada commitments.

54. We also concluded that Export Development Canada implemented the Environmental and Social Review Directive as designed; however, project monitoring remains an issue to ensure necessary corrective action.

About the Audit

This independent assurance report was prepared by the Office of the Auditor General of Canada on the design and implementation of Export Development Canada’s Environmental and Social Review Directive. Our responsibility was to provide objective information, advice, and assurance to assist Parliament in its scrutiny of the government’s management of resources and programs and to conclude on whether the directive complied in all significant respects with the applicable criteria.

All work in this audit was performed to a reasonable level of assurance in accordance with the Canadian Standard on Assurance Engagements (CSAE) 3001—Direct Engagements, set out by the Chartered Professional Accountants of Canada (CPA Canada) in the CPA Canada Handbook—Assurance.

The Office of the Auditor General of Canada applies the Canadian Standard on Quality Management 1—Quality Management for Firms That Perform Audits or Reviews of Financial Statements, or Other Assurance or Related Services Engagements. This standard requires our office to design, implement, and operate a system of quality management, including policies or procedures regarding compliance with ethical requirements, professional standards, and applicable legal and regulatory requirements.

In conducting the audit work, we complied with the independence and other ethical requirements of the relevant rules of professional conduct applicable to the practice of public accounting in Canada, which are founded on fundamental principles of integrity, objectivity, professional competence and due care, confidentiality, and professional behaviour.

In accordance with our regular audit process, we obtained the following from entity management:

- confirmation of management’s responsibility for the subject under audit

- acknowledgement of the suitability of the criteria used in the audit

- confirmation that all known information that has been requested, or that could affect the findings or audit conclusion, has been provided

- confirmation that the audit report is factually accurate

Audit objective

The objective of this audit was to determine whether the design of Export Development Canada’s Environmental and Social Review Directive was suitable, if the directive’s requirements were implemented, and if the directive aligned with the Government of Canada’s environmental and social commitments.

Scope and approach

The audit examined the design and implementation of Export Development Canada’s Environmental and Social Review Directive. The audit also examined whether the directive aligned with the Government of Canada’s environmental and social commitments. To assess the suitability of the design, we examined whether the directive was based on suitable international standards, whether the directive aligned with those standards, and whether the design of the directive supported the Government of Canada’s environmental and social commitments.

To assess whether the requirements of the directive were implemented, we conducted interviews and reviewed documents, including policies and procedures. We extracted data from Export Development Canada’s system of record of guarantees, loans, and limited recourse / project financing transactions where an environmental and/or social review was completed within our audit period. From this population of 11,193 transactions, we selected

- a representative sample of 33 out of 66 transactions that met the definition of a project, that had a completed environmental review, and that was assigned a category, all within our audit period. We used a confidence level of 90% and a margin of error of +10% to select these samples.

- 20 targeted non‑project transactions where other environmental and social review processes were completed but did not meet the definition of a project

- 7,768 financially completed transactions, identifying those in carbon-intensive industries (such as aerospace, oil and gas, and mining and forestry) and those that had Export Development Canada clean financing indicators (such as cleantech, climate-change financing eligibility, and environmental industry). The industry identifier used was the borrower’s industry of risk, which is a high‑level identifier for the industry in which the transaction occurs.

Criteria

We used the following criteria to conclude against our audit objective:

| Criteria | Sources |

|---|---|

|

The design of Export Development Canada’s Environmental and Social Review Directive is suitable:

|

|

|

Export Development Canada implements the requirements of its Environmental and Social Review Directive. |

|

Period covered by the audit

The audit covered the period from 1 May 2019 to 31 March 2023. This is the period to which the audit conclusion applies. However, to gain a more complete understanding of the subject matter of the audit, we also examined certain matters outside of these dates.

Date of the report

We obtained sufficient and appropriate audit evidence on which to base our conclusion on 11 September 2023, in Ottawa, Canada.

Audit team

This audit was completed by a multidisciplinary team from across the Office of the Auditor General of Canada led by Elsa Da Costa, Principal. The principal has overall responsibility for audit quality, including conducting the audit in accordance with professional standards, applicable legal and regulatory requirements, and the office’s policies and system of quality management.

Recommendations and Responses

In the following table, the paragraph number preceding the recommendation indicates the location of the recommendation in the report.

| Recommendation | Response |

|---|---|

|

27. To improve its environmental and social review processes, Export Development Canada should implement an integrated case management system and a quality assurance process to minimize errors. |

The corporation’s response. Agreed. Throughout 2023, Export Development Canada has been taking action to improve environmental, social, and governance (ESG) data quality and completeness assessments through the implementation of new controls, including the introduction of additional formal oversight and quality assurance reviews. In addition, the corporation is currently exploring opportunities for technology and system upgrades to improve the multi‑stakeholder user experience, including for those performing ESG‑related due diligence. The corporation will leverage this ongoing work to explore options to implement an integrated case management system as it pertains to ESG transaction reviews. |

|

37. Building on our previous 2019 recommendation, to minimize the environmental and social effects of transactions, Export Development Canada should expand the scope of its Environmental and Social Review Directive by

|

The corporation’s response. Partially agreed. Export Development Canada disagrees that the current definition of a project under the Environmental and Social Review Directive is misaligned with the Organisation for Economic Co‑operation and Development Common Approaches and the Equator Principles, as the definition includes

However, the corporation does agree to find ways to further clarify how the directive’s definition of a project is consistent with the definitions embedded in the Common Approaches and the Equator Principles, including replacing terminology such as “major” extensions with “material” while ensuring alignment with the scope of the directive as set forth in the Export Development Act. The exceptions list in the directive was reviewed during the 2022 Environmental and Social Risk Management Policy Framework update, which included stakeholder consultation with Environment and Climate Change Canada, Global Affairs Canada, and Natural Resources Canada, and no significant concerns or issues were noted with the current identified exceptions. The corporation commits to reviewing the exceptions list and the conditions that justify the corporation entering into a project in 2024. Should gaps with international standards and norms be identified, the corporation will prioritize actions to address them accordingly. For project re‑finance exceptions, additional financing does not necessarily equate with new or changed environmental and social risks. All existing environmental and social obligations are included in the new financing documentation, including monitoring requirements. Where it has been determined that there is a significant change in the project’s scale or scope, a new determination under the directive is required. The corporation’s approach is aligned with Equator Principles IV. As noted in the audit, a large majority of Export Development Canada transactions do not relate to projects given the corporation’s broad mandate, varied product offerings, and the non‑project nature of most international trade transactions. The corporation maintains a robust suite of due diligence processes to ensure transactions not covered under the scope of the directive are reviewed. These risk based reviews can also be extensive in nature. |

|

43. In order to strengthen due diligence for transactions and projects and to ensure that decisions on project financing align with Government of Canada commitments, Export Development Canada should

|

The corporation’s response. Agreed. Export Development Canada’s existing Climate Change Procedure outlines due diligence requirements for transactions within and out of scope of the Environmental and Social Review Directive. For in‑scope project-based transactions, the procedure outlines requirements of the Organisation for Economic Co‑operation and Development and the Equator Principles, including a Climate Change Risk Assessment for Category A and B projects. The risk assessment can include an analysis of physical and transition risks, an alternatives analysis to identify options to reduce greenhouse gas emissions, and alignment with the host country climate commitments. The corporation commits to a review of the Climate Change Procedure in 2024 to ensure continued alignment with the corporation’s internal and external commitments and Government of Canada expectations. Should any gaps be identified, corrective actions will be prioritized by the corporation. The corporation’s current approach recognizes that the sensitive site verification includes assessment of risks such as biodiversity and other sensitive factors (for example, areas of importance for Indigenous peoples). The corporation commits to reviewing processes in 2024 to strengthen documentation requirements relating to sensitive area verification. Aligned with industry practice, the corporation determines if there is a high likelihood of significant residual adverse environmental and social effects after the application of mitigation measures required by host country requirements. If host country standards are determined to be insufficient, the corporation elects to benchmark to international standards or frameworks, including the International Finance Corporation Performance Standards. The corporation agrees in 2024 to strengthen documentation of the relevant International Finance Corporation Performance Standards that are benchmarked during project review. |

|

52. To increase transparency and facilitate the ability of stakeholders to analyze the corporation’s support of projects, Export Development Canada should disclose

|

The corporation’s response. Agreed. Export Development Canada would like to clarify that it discloses the dollar ranges for all signed financing transactions, including Category A and B projects, on its individual transaction page on its website (known as D2 reporting). Additionally, the corporation publishes a new disclosure for subsequent financing when the dollar amount has exceeded the previous disclosure’s dollar range or 2 years have elapsed since the previous disclosure. The corporation implements a robust Transparency and Disclosure Policy that goes beyond the disclosure obligations set out in the Organisation for Economic Co‑operation and Development Common Approaches and the Equator Principles and is informed by public consultation. The corporation agrees to revisit the Office of the Auditor General of Canada’s recommendations during the next formal review period (2025). With respect to the disclosure of greenhouse gas emissions and emission estimates for projects, commencing in 2024, the corporation will

The corporation agrees to make data on individual transactions available in a machine readable format on a go‑forward basis and has begun work to do so. |