2023 November Report of the Auditor General of Canada to the Parliament of Canada

Environmental and Social Review Directive—Export Development Canada

At a Glance

Export Development Canada’s mandate is to support and develop Canada’s export trade and respond to international business opportunities. In fulfilling its mandate, the corporation must also consider the environmental and social effects of the support it provides.

Overall, we found that the project definition applied under the Environmental and Social Review Directive is narrow, as it applies only to 0.4% of the transactions that the corporation supports. This allows for transactions with similar environmental and social risks to proceed under other review processes with varying levels of due diligence. This means that the corporation may not have a complete picture of the environmental and social risks for those other transactions.

In addition, we found that the screening processes for transactions further excludes some projects from in‑depth review and disclosure. For example, we found that exceptions outlined in the directive allowed up to $150 million of additional funding to be approved for an oil and gas project, which had previously been reviewed under the directive. This was considered an exception because the borrower requested the additional funding for an existing project; as such, the corporation determined that the project scope had not changed and that no further review or disclosure was required.

Although the corporation generally complied with the directive issued by its board, we identified gaps in the directive’s implementation, design, and transparency. Some of these gaps were noted in our previous audits and still persist. The design of the directive allowed for the corporation to finance projects with high greenhouse gas emissions, which may not align with the Government of Canada environmental and social commitments.

Key facts and findings

- In 2001, the corporation’s board of directors developed the Environmental Review Directive. In 2010, it became the Environmental and Social Review Directive, and it was last updated in 2022.

- The narrow definition of project-related financing means that a small number of transactions are subject to a review. Between 1 May 2019 and 31 March 2023, only 33 (0.4%) of 7,768 total completed transactions were subject to a review under the directive. This represented $4.6 billion (5.9%) of the $77.9 billion in total funding loaned to borrowers during this period.

- The directive allowed for transactions with similar environmental and social risks to proceed under other review processes with varying levels of due diligence. This means that the corporation may not have a complete picture of the environmental and social risks for those transactions.

- Although the corporation increased its support for transactions that aim to reduce negative environmental effects, the corporation still continues to support carbon‑intensive sectors, as it does not consistently identify them as posing a high environmental risk.

Why we did this audit

- As Canada’s export credit agency, Export Development Canada, depending on its course of action, can contribute to or detract from achieving Canada’s environmental and social commitments.

- Export Development Canada is required by legislation to implement the Environmental and Social Review Directive. Implementing it correctly is one of the critical processes through which the corporation can ensure that they manage the environmental and social risks of the projects they support.

- Environmental and social risks may only materialize once a project is underway, after loan agreements are finalized.

- When the Environmental and Social Review Directive is not applied, Export Development Canada could be providing funding for projects without being fully aware of their environmental and social risks. These could include human rights violations, increased greenhouse gas emissions, and loss of biodiversity.

Highlights of our recommendations

- Building on our previous 2019 recommendation, to minimize the environmental and social effects of transactions, Export Development Canada should expand the scope of its Environmental and Social Review Directive.

- To improve its environmental and social review processes, Export Development Canada should implement an integrated case management system and a quality assurance process to minimize errors.

- To increase transparency and facilitate the ability of stakeholders to analyze the corporation’s support of projects, Export Development Canada should disclose

- the initial and subsequent amounts of funding provided for projects on its listing of transactions reviewed under the Environmental and Social Review Directive

- information on Category B transactions prior to approving them and then a project review summary after approving them, as it does for Category A transactions

- greenhouse gas emissions and emission estimates for all projects reviewed under the directive

- data on individual transactions in a machine‑readable format that facilitates analysis

Please see the full report to read our complete findings, analysis, recommendations and the audited organizations’ responses.

Exhibit highlights

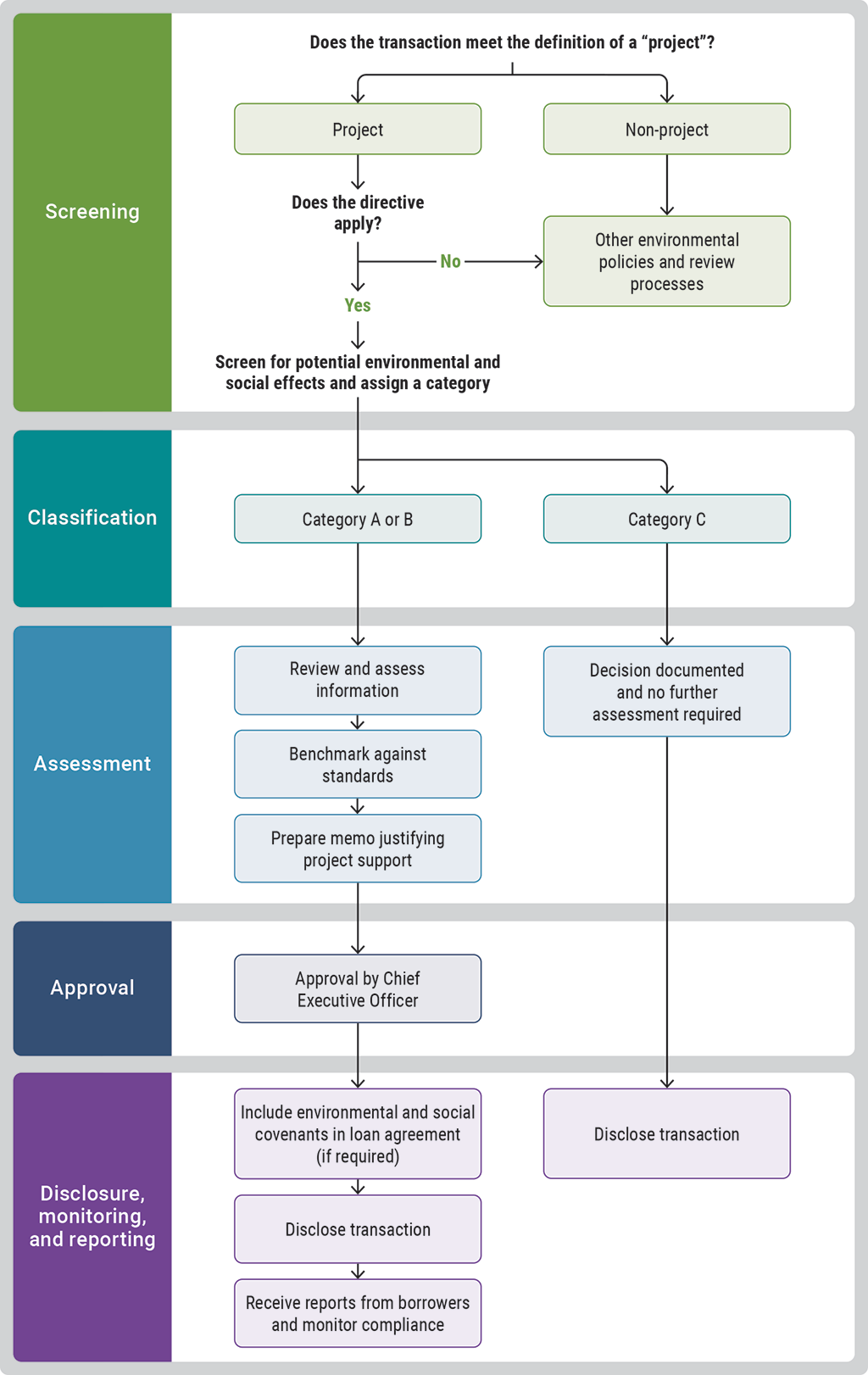

How Export Development Canada applies the Environmental and Social Review Directive to transactions

Source: Adapted from Export Development Canada’s Environmental and Social Review Directive

Text version

This flowchart shows the process that Export Development Canada uses to apply the Environmental and Social Review Directive to transactions. The process includes the following stages:

- screening

- classification

- assessment

- approval

- disclosure, monitoring, and reporting

At the screening stage, the corporation determines whether the transaction meets the definition of a “project.” If not, it determines which other environmental policies and review processes apply.

If the transaction meets the definition of a project, the corporation determines whether the directive applies. If the directive does not apply, the corporation determines which other environmental policies and review processes apply.

If the directive does apply to the transaction, the corporation screens for potential environmental and social effects and assigns a category.

At the classification stage, the transaction is assigned category A, B, or C. If category C, the decision is documented and no further assessment is required.

If the transaction is assigned category A or B, then the corporation

- reviews and assesses information

- benchmarks against standards

- prepares a memo justifying its support for the project

The transaction is then sent for approval by the Chief Executive Officer.

The next stage is disclosure, monitoring, and reporting. At this stage, the corporation

- includes environmental covenants in the loan agreement (if required)

- discloses the transaction

- receives reports from borrowers and monitors compliance

The corporation discloses transactions for category A, B, and C transactions.

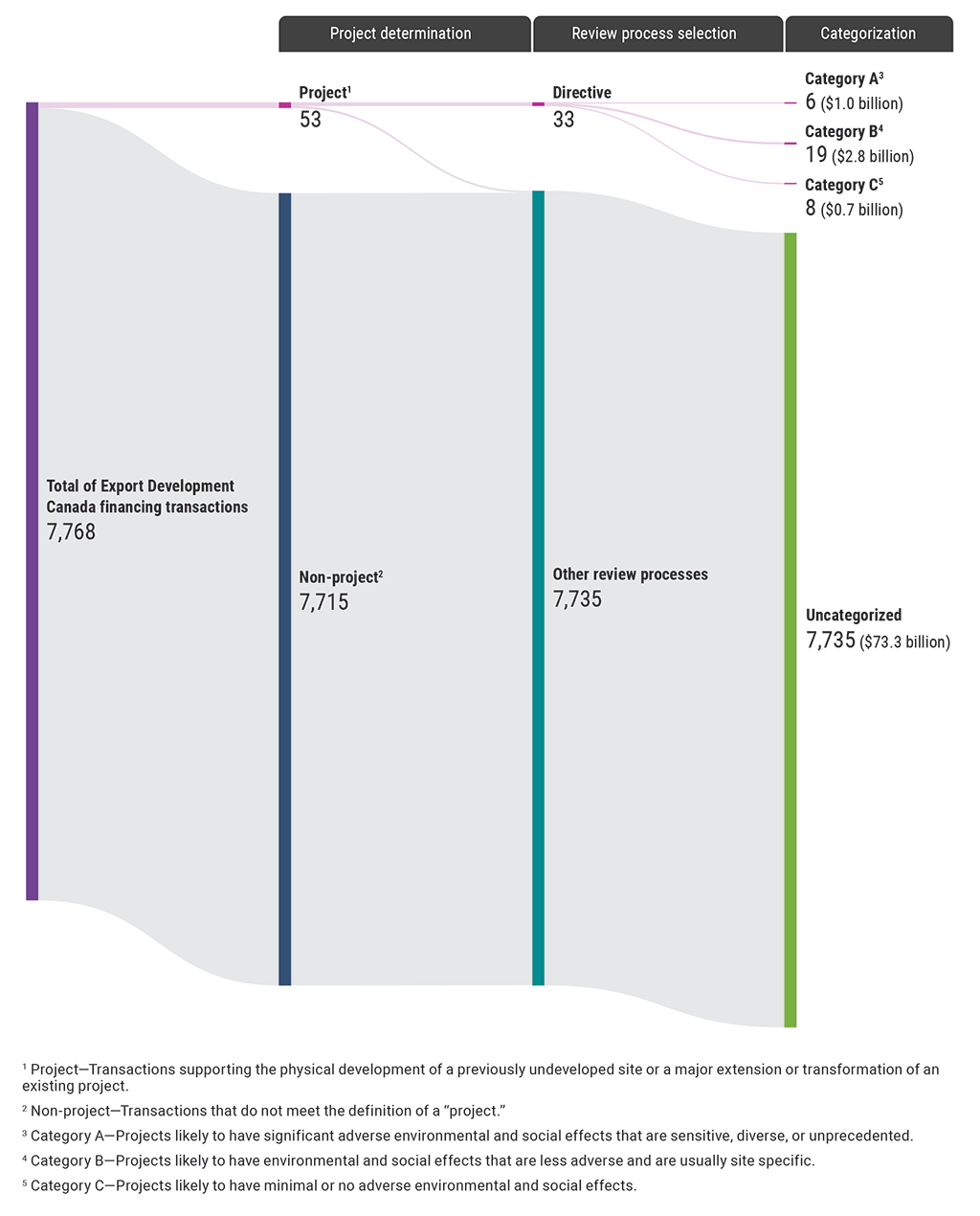

Only 33 out of 7,768 transactions were reviewed under the Environmental and Social Review Directive during our audit period

Text version

This chart shows how the corporation’s assessment process resulted in most of the 7,768 financing transactions being excluded from review under the Environmental and Social Review Directive. The corporation determined that only 53 transactions met the definition of a project. A project is a transaction supporting the physical development of a previously undeveloped site or a major extension or transformation of an existing project. The corporation then determined that the directive applied to only 33 projects. It classified these 33 projects as follows:

- 6 were classified as Category A and were valued at $1.0 billion. Category A projects are likely to have significant adverse environmental and social effects that are sensitive, diverse, or unprecedented.

- 19 were classified as Category B and were valued at $2.8 billion. Category B projects are likely to have environmental and social effects that are less adverse and are usually site specific.

- 8 were classified as Category C and were valued at $0.7 billion. Category C projects are likely to have minimal or no adverse environmental and social effects.

The total number of Export Development Canada financing transactions during our audit period was 7,768 transactions. During project determination, the corporation determined that 7,715 transactions were non-projects.

During review selection, the corporation determined that the directive did not apply to 7,735 transactions. For these transactions, the corporation determined that other review processes applied. Because the directive did not apply to these transactions, they were not categorized. These transactions were valued at $73.3 billion. In comparison, the projects that were selected for review under the directive were valued at $4.5 billion.

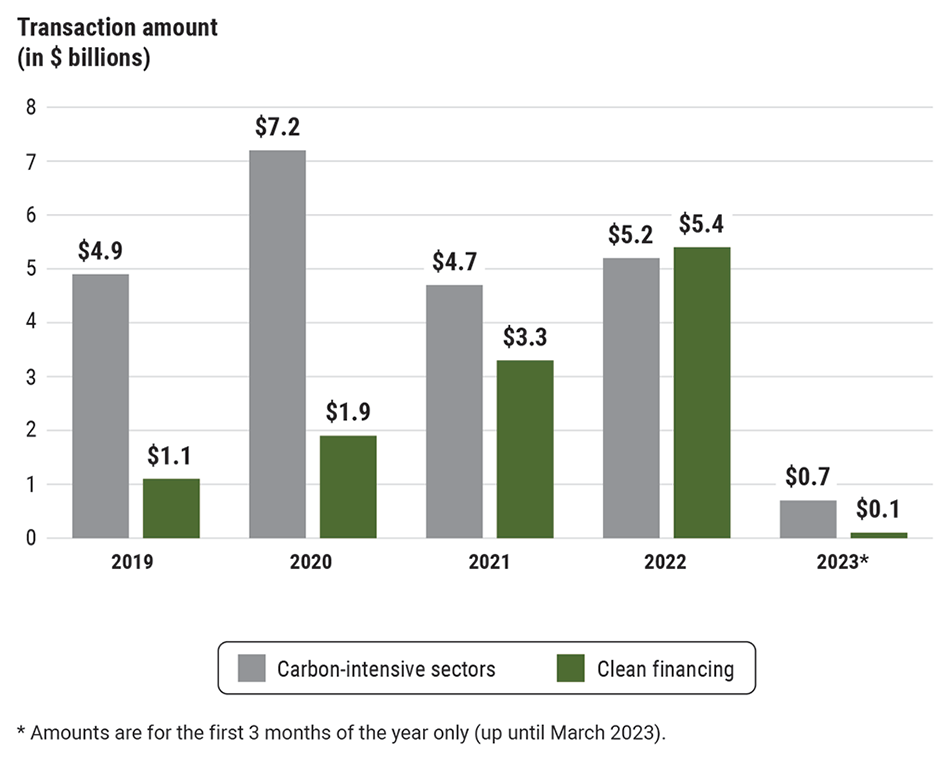

The corporation increased support for clean financing but continued to support carbon-intensive sectors

Text version

This bar chart shows support for carbon-intensive sectors and for clean financing in terms of transaction amounts from 2019 to March 2023. Overall, the carbon-intensive sectors received ongoing amounts of financial support, and the support for clean financing increased consistently since 2019.

In 2019, the corporation provided $4.9 billion to carbon-intensive sectors and $1.1 billion to clean financing.

In 2020, the corporation increased its financing to $7.2 billion to carbon-intensive sectors and provided $1.9 billion to clean financing.

In 2021, the corporation decreased its financing to $4.7 billion to carbon-intensive sectors and increased its support to $3.3 billion for clean financing.

In 2022, the corporation provided $5.2 billion to carbon-intensive sectors and increased its support to $5.4 billion for clean financing.

In the first 3 months of 2023, the corporation provided $0.7 billion to carbon-intensive sectors and $0.1 billion to clean financing.

Related information

Entities

Tabling date

- 2 November 2023

Related audits

- 2019 December Report of the Auditor General of Canada to the Parliament of Canada

Export Development Canada’s Environmental and Social Review Directive