Office of the Auditor General of Canada2022–23 Departmental Results Report

Message from the Auditor General of Canada

Auditor General of Canada

I am pleased to present the 2022–23 Departmental Results Report for the Office of the Auditor General of Canada (OAG).

The first 3 years of my 10‑year mandate have shown that the OAG has the resilience and strength to adapt to the ongoing changes in our world today. By focusing on areas that matter to Canadians, our work plays a crucial role in promoting transparency in our public institutions and in supporting the accountability relationship between elected officials and government organizations in the spending of public funds, at both the federal and territorial levels.

In 2022–23, we initiated a review of our process for selecting the areas of focus for our performance audits to enhance the relevance of our work for Canadians, legislators, and the entities we audit. We also continued to advance our organizational-level transformation initiatives, which include transitioning to a hybrid workplace, modernizing our processes, reducing our environmental footprint, and supporting a healthy workplace culture.

We delivered audits that allowed us to engage Parliament and the territorial legislatures in dialogue on a variety of important topics, such as chronic homelessness, access to benefits for hard‑to‑reach populations, processing disability benefits for veterans, addictions prevention and recovery services, the just transition to a low‑carbon economy, and hydrogen’s potential to reduce greenhouse gas emissions.

The cost of federal initiatives relating to the coronavirus disease (COVID‑19) pandemic has amounted to billions of dollars. In 2022–23, our office continued to support parliamentarians in their role of holding the government to account for its pandemic-related expenditures. In December 2022, we issued our performance audit report on specific COVID‑19 benefits, which focused on the payment and recovery of benefits and the achievement of the objectives of 6 COVID‑19 benefit programs. In our Commentary on the 2021–2022 Financial Audits, we provided our observations on the federal government’s COVID‑19 economic response and its effects on the financial statements of the Government of Canada. We also drew attention to the process of identifying and recovering overpayments of ineligible benefits.

We have accomplished much in 2022–23, and I am proud to lead the OAG’s dedicated and professional employees, who are committed to doing their best work for all Canadians.

[Original signed by]

Karen Hogan, Fellow Chartered Professional AccountantFCPA

Auditor General of Canada

7 September 2023

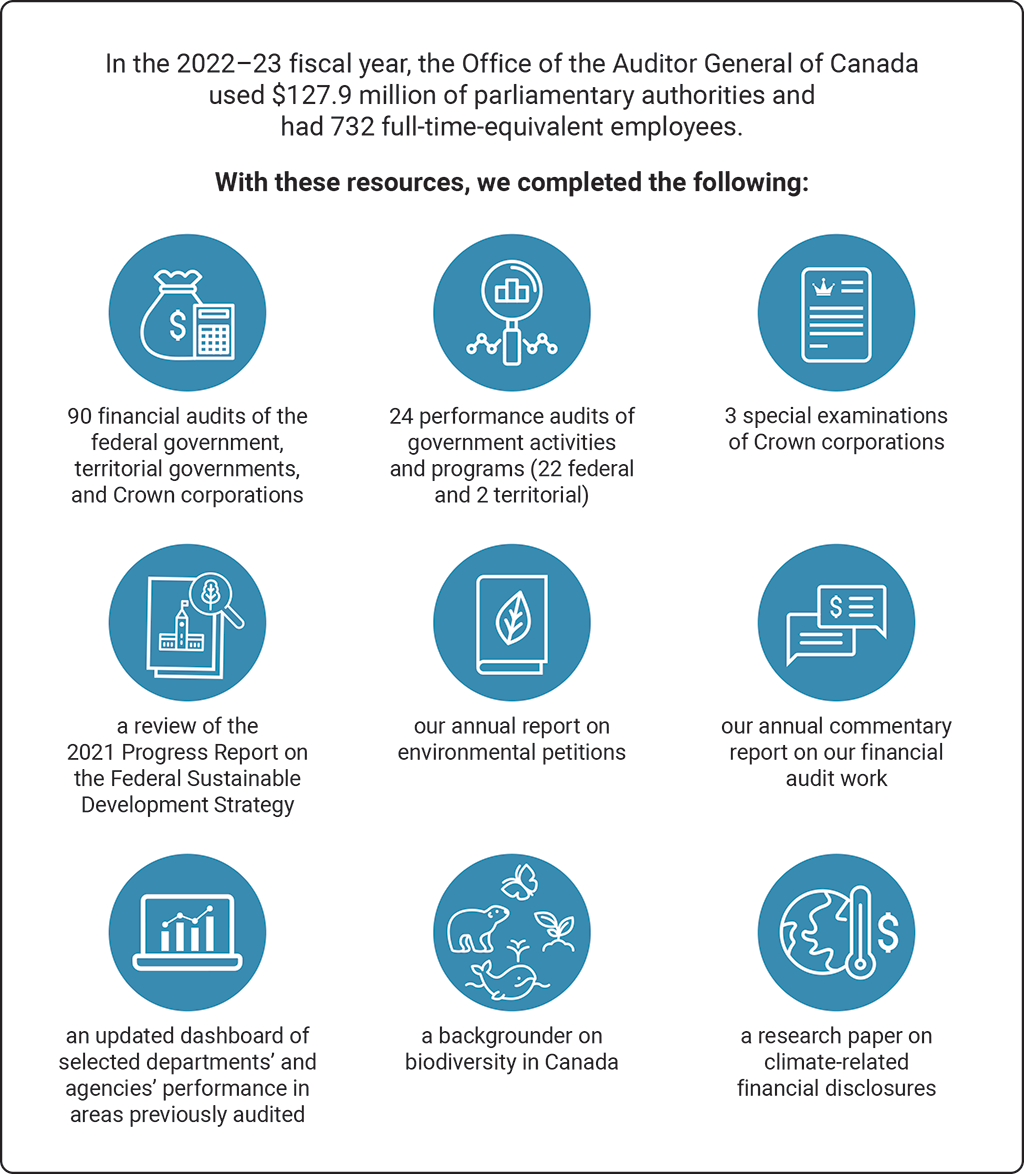

Results at a glance

Text version

In the 2022–23 fiscal year, the Office of the Auditor General of Canada used $127.9 million of parliamentary authorities and had 732 full-time-equivalent employees.

With these resources, we completed the following:

- 90 financial audits of the federal government, territorial governments, and Crown corporations

- 24 performance audits of government activities and programs (22 federal and 2 territorial)

- 3 special examinations of Crown corporations

- a review of the 2021 Progress Report on the Federal Sustainable Development Strategy

- our annual report on environmental petitions

- our annual commentary on our financial audit work

- an updated dashboard of selected departments’ and agencies’ performance in areas previously audited

- a backgrounder on biodiversity in Canada

- a research paper on climate-related financial disclosures

For more information on the OAG’s plans, priorities, and results achieved, see the “Results: What we achieved” section of this report.

Results: What we achieved

Our core responsibility: Legislative auditing

Description

Our audit reports provide objective, fact‑based information and advice on government programs and activities. With our audits, we assist Parliament in its authorization and oversight of government spending and operations.

Our audits also help territorial legislatures, boards of Crown corporations, and audit committees in their oversight of the management of government activities. Those charged with governance use our audit findings to hold their respective organizations to account for the handling of public funds.

Financial audits assess whether the annual financial statements of the Government of Canada, Crown corporations, and others are presented fairly, consistent with applicable accounting standards.

Performance audits assess whether government organizations manage programs with due regard for economy, efficiency, and environmental impact, and measure their effectiveness. We have also incorporated the assessment of equity, diversity, and inclusion as a priority area for our performance audits.

Special examinations assess whether Crown corporation systems and practices provide reasonable assurance that assets are safeguarded, resources are managed economically and efficiently, and operations are managed effectively.

Our current results

Audit operations

Our role in supporting well‑managed and accountable government is to deliver high‑quality audit work in a timely manner to Parliament, the territorial legislative assemblies, and the boards of the Crown corporations we audit. This work helps inform our stakeholders’ decision making and assists them in fulfilling their oversight responsibilities.

In the 2022–23 fiscal year, we met our internal targets for audit reporting, generating 100% of our statutory audit reports on time and 82% of our audit reports without statutory deadlines in line with our planned reporting dates.

Financial audits

In the 2022–23 fiscal year, we completed 90 financial audits. These include audits of the consolidated financial statements of the Government of Canada and each of the 3 territorial governments and audits of the financial statements of federal Crown corporations, territorial corporations, and other organizations.

The objectives of our financial audits are to opine on whether the financial statements of the auditee achieve fair presentation in accordance with their applicable financial reporting framework and to opine on the entity’s compliance with specified authorities. Unmodified audit opinions indicate that in all material respects, the entity’s financial statements are fairly presented, in accordance with the applicable financial reporting framework. They also indicate that the transactions that came to our notice during the financial audit have complied, in all material respects, with the specified authorities. While control over this rests with the entities, we support and encourage their adoption of accounting standards by working with them to identify opportunities for continuous improvement in their systems of financial reporting and internal control. With this in mind, our target for financial audit reports to be issued with an unmodified opinion is 100%.

During the 2022–23 fiscal year, 97% of our financial audit opinions were issued on an unmodified basis. Of the 4 modified opinions reported in 2021–22, only 1 was resolved. All 3 of the modified audit opinions we noted in 2022–23 were recurring and related to our inability to observe physical inventory counts in the prior year because of pandemic-related travel restrictions.

We also presented our annual commentary on financial audits, which provides additional insights to Parliament on matters of significance raised during our financial audits. In this report, we presented information on the upcoming adoption of accounting standards on asset retirement obligations and on increasing environmental, social, and governance reporting. The commentary provided parliamentarians with a summary of the government’s COVID‑19 economic response and its effects on the financial statements of the Government of Canada, an initiative that has involved more than $375 billion over 3 years.

Performance audits

We presented 24 performance audit reports in the 2022–23 fiscal year: 22 to the Parliament of Canada, 1 to the Yukon Legislative Assembly, and 1 to the Northwest Territories Legislative Assembly. These reports appear in the “List of reports” section of this report and include findings on a variety of important subjects, such as chronic homelessness, access to benefits for hard‑to‑reach populations, processing disability benefits for veterans, and hydrogen’s potential to reduce greenhouse gas emissions. They also include our December 2022 performance audit report on specific COVID‑19 benefits, which focused on the payment and recovery of benefits and the achievement of the objectives of 6 COVID‑19 benefit programs.

The 2022–23 fiscal year also marked the second iteration of our Update on Past Audits tool. This dashboard, available on the OAG’s website, tracks the performance of selected departments and agencies in areas we previously audited. This iteration reviews selected performance measures that we previously reported on and expands on the previous edition to include the review of the implementation of past audit recommendations. The results of this analysis showed that 74% of recommendations reviewed during the 2022–23 update were fully implemented.

Special examinations

Special examinations are a type of performance audit that focuses on the operations of parent federal Crown corporations. Our target is for 100% of the corporations we audit to have no significant deficiencies identified, and for the significant deficiencies that are identified to be corrected by the time the next special examination is conducted. Although the entities control the outcome of this indicator, our target is based on our expectation that the work we do will promote effective management and governance practices.

For the 2022–23 fiscal year, we reported the special examination results of 3 Crown corporations: Jacques-Cartier and Champlain Bridges incorporatedInc., the Windsor-Detroit Bridge Authority, and the Canadian Broadcasting Corporation. One significant deficiency was identified for the period under review, relating to board oversight at the Windsor-Detroit Bridge Authority.

Our 2022–24 Strategic Plan

As outlined in our 2022–23 Departmental Plan, our strategic framework guides us in shaping our culture and improving the delivery of our legislative auditing program. Over the past year, we updated this framework to align with and focus on our priorities. We remain guided by principles under our pillars of care, connect, and modernize, and we focus on 2 priorities: a rallying call around a shared vision and building meaningful relationships with our stakeholders.

Priority 1: One office, one team, one vision

“One office, one team, one vision” is a rallying call that embodies the collective mindset we seek to adopt. This priority means consciously coordinating and integrating across all areas of activity and expertise. It calls for meaningfully engaging with colleagues on OAG culture, recognizing and leveraging the range of our people’s skills and expertise, and creating opportunities to exchange and engage with colleagues in other areas. As we work together to fulfill our mandate, we will be supported by renewed processes and tools, cohesion across operations, and a modernized work environment.

In the 2022–23 fiscal year, we worked on multiple initiatives to support this priority, such as the following:

- A big milestone in OAG FLEX, our transition to a hybrid work model, took place in January 2023, when we welcomed our management cadre back on site for 37.5 hours a month. All employees returned to in‑person work in June 2023.

- The first phase of our transformation initiative was completed in 2022. As a result of this initial discovery phase, the initiative has been divided into 3 streams that will transform our audits and internal services as well as our cybersecurity and aging information technologyIT systems. Work on all 3 streams continues in parallel, as each stream develops a roadmap to determine and implement next steps.

- Our employee engagement initiative was launched in 2022 with office‑wide consultations to gather input from employees. Once the consultations were complete, a working group of managers was struck to develop an action plan, with plans in place to engage non‑management employees in the future.

Priority 2: Meaningful relationships, trusted advice

A constructive, beneficial, and productive working relationship is built on mutual trust, respect, awareness, inclusion, and honest communication.

The OAG plays an important role in holding government accountable for financial responsibility, well‑managed programs, and transparency in public reporting. Our relevance is built on knowledge, recognized expertise, and the value we bring to stakeholders, including parliamentarians and other elected representatives, government officials, public servants and administrators, and Canadians.

To inform our work and remain relevant through value realization, we will purposefully engage and foster trust with key stakeholders.

In 2022–23, we supported Priority 2 with the following initiatives:

- Our departmental results framework was updated in 2022–23 to better align with our renewed mission and vision. This new framework reflects our continued focus on productive and collaborative relationships with our stakeholders.

- We developed guidance for our employees for establishing a clear and coordinated approach as we finalize our stakeholder engagement plan.

- We modernized our post‑audit survey tools and can now better collect, analyze, and report feedback from our financial audit and special examination clients.

Gender-based analysis plus

The OAG incorporates gender-based analysis plus (GBA Plus) in its audit work to provide elected officials and all Canadians with objective information on the government’s progress toward its gender, equity, diversity, and inclusion priorities. A summary of the activities to support the advancement of Canada’s GBA Plus commitments is included in a supplementary information table accompanying this report.

United Nations’ 2030 Agenda for Sustainable Development and the Sustainable Development Goals

The OAG is committed to aligning its audit work to support the United Nations’ 2030 Agenda for Sustainable Development and the underlying 17 Sustainable Development Goals. All of the OAG’s audits—financial audits, performance audits, and special examinations—contribute to the goal of peace, justice, and strong institutions (Goal 16). In addition, we consider the other goals when planning and reporting on our audit work (Exhibit 1).

Exhibit 1—The number of United Nations’ Sustainable Development Goal references in the OAG’s direct engagements for the 2022–23 fiscal year

Exhibit 1—text version

This image shows the number of United Nations’ Sustainable Development Goal references in the direct engagements of the Office of the Auditor General of Canada, or OAG, for the 2022–23 fiscal year.

The number of references includes mentions of any of the United Nations’ Sustainable Development Goals or the 2030 Agenda for Sustainable Development in the OAG’s performance audit reports presented to Parliament and northern legislative assemblies and in the OAG’s special examination reports transmitted to Crown corporations during the period from 1 April 2022 to 31 March 2023. Because a direct engagement report may refer to more than 1 goal, the total number of references is greater than the total number of reports presented or transmitted during the period.

The Sustainable Development Goals that are mentioned and the number of references are as follows.

| Sustainable Development Goal | Number of references |

|---|---|

| Goal 1: No poverty | 4 |

| Goal 3: Good health and well-being | 3 |

| Goal 5: Gender equality | 3 |

| Goal 6: Clean water and sanitation | 1 |

| Goal 8: Decent work and economic growth | 1 |

| Goal 9: Industry, innovation and infrastructure | 5 |

| Goal 10: Reduced inequalities | 5 |

| Goal 11: Sustainable cities and communities | 4 |

| Goal 12: Responsible consumption and production | 3 |

| Goal 13: Climate action | 5 |

| Goal 14: Life below water | 1 |

| Goal 15: Life on land | 2 |

| No specific goal | 5 |

The exhibit includes the Sustainable Development Goal icons. The source of these icons is the United Nations.

Notes:

- The number of references includes mentions of any of the United Nations’ Sustainable Development Goals or the 2030 Agenda for Sustainable Development in the OAG’s performance audit reports presented to Parliament and northern legislative assemblies and in the OAG’s special examination reports transmitted to Crown corporations during the period from 1 April 2022 to 31 March 2023. Because a direct engagement report may refer to more than 1 goal, the total number of references is greater than the total number of reports presented or transmitted during the period.

- The source of the Sustainable Development Goal icons is the United Nations.

We were pleased that our previous recommendations to government regarding better aligning the Federal Sustainable Development Strategy with the goals were acted on in the new 2022 to 2026 Federal Sustainable Development Strategy, which has a new structure focused on the goals.

Contracts awarded to Indigenous businesses

For the purposes of complying with the Directive on the Management of Procurement, the OAG is a Phase 3 organization and as such is aiming to achieve the minimum target of awarding 5% of the total value of contracts to Indigenous businesses by the end of the 2024–25 fiscal year.

- In 2022–23, the contract reporting fields were updated in the OAG’s financial system of record to better support the timely identification and disclosure of contracts awarded to Indigenous businesses.

- In 2023–24, the OAG will evaluate Indigenous business capacity and identify set‑aside opportunities in areas where there is significant contracting activity.

Results achieved

The OAG maintains a departmental results framework for reporting corporate results in accordance with the Treasury Board’s Policy on Results. Our new framework came into effect on 1 April 2023 and was included in our 2023–24 Departmental Plan.

Exhibit 2 presents the OAG’s indicators, targets, and results for the last 3 fiscal years for our departmental result: well‑managed and accountable government.

Exhibit 2—Departmental result indicators, targets, and actual results for the 2020–21, 2021–22, and 2022–23 fiscal years

| Departmental result indicators | Target | Date to achieve target | 2020–21 Actual results |

2021–22 Actual results |

2022–23 Actual results |

|---|---|---|---|---|---|

|

Percentage of audit reports on financial statements without qualifications or “other matters” raised |

100% |

Ongoing |

Target not met |

Target not met |

Target not met |

|

Percentage of special examination reports with no significant deficiencies |

100% |

Ongoing |

Target not met |

Target met |

Target not met |

|

Percentage of audit recommendations or opinions addressed by entities: For financial audits, percentage of qualifications and “other matters” addressed from one financial audit report to the next |

100% |

Ongoing |

Target not met |

Target not met |

Target not met |

|

Percentage of audit recommendations or opinions addressed by entities: For performance audits, percentage of recommendations examined for which progress is assessed as “substantial improvement” |

At least 75% |

Ongoing |

Not applicableNote 5 |

Not applicableNote 5 |

Target not met |

|

Percentage of audit recommendations or opinions addressed by entities: For special examinations, percentage of significant deficiencies reported in our special examination reports that are addressed from one examination to the next |

100% |

Ongoing |

Not applicableNote 7 |

Not applicableNote 8 |

Not applicableNote 9 |

|

Percentage of audits that meet statutory deadlines, where applicable, or our planned reporting dates |

|||||

|

100% |

Ongoing |

Target not met |

Target not met |

Target met |

|

At least 80% |

Ongoing |

Target not met |

Target met |

Target met |

Financial, human resources, and performance information for the OAG’s program inventory is available in GC InfoBase.

Resources used

The Office of the Auditor General of Canada (OAG) reports information about its expenditures on the Government of Canada’s Open Government portal. This information includes all contracts valued at more than $10,000 and all travel and hospitality expenses of the Auditor General, the Deputy Auditor General, the Commissioner of the Environment and Sustainable Development, the assistant auditors general, and our Senior General Counsel. The OAG also publishes quarterly financial reports and annual audited financial statements on its website.

Parliamentary authorities provided and used

Parliament provided the OAG with up to $135.6 million in parliamentary authorities, which consisted of $119.9 million in Main Estimates authorities, and $15.7 million in adjustments and transfers, which for the most part were routine in nature—for example, carry-forward funding from the previous year and an adjustment for retroactive wage increases (Exhibit 3).

Exhibit 3—Budgetary financial resources (in millions of dollars)

| 2022–23 Main Estimates |

2022–23 Planned spending |

2022–23 Total authorities available for use |

2022–23 Actual spending (authorities used) |

2022–23 Difference (actual spending minus planned spending) |

|---|---|---|---|---|

| 119.9 | 119.9 | 135.6 | 127.9 | 8.0 |

In the 2022–23 fiscal year, $127.9 million was charged against our total parliamentary authorities of $135.6 million. This resulted in the lapse of $7.7 million of the OAG’s parliamentary authorities provided in the 2022–23 fiscal year. The OAG requested the creation of a permanent frozen allotment of $4.1 million to fund projects related to the modernization of aging IT systems and to our transformation initiative, which reduces the lapse to $3.6 million. The OAG may carry forward up to 5% of its operating budget (on the basis of Main Estimates program expenditures) into the next fiscal year, subject to parliamentary approval. This carry forward comprises a combination of lapsed authorities ($3.6 million) and credits for certain pay‑related amounts ($1.9 million) for which authorities were not provided in the current year. We expect to carry forward $5.5 million into the 2023–24 fiscal year.

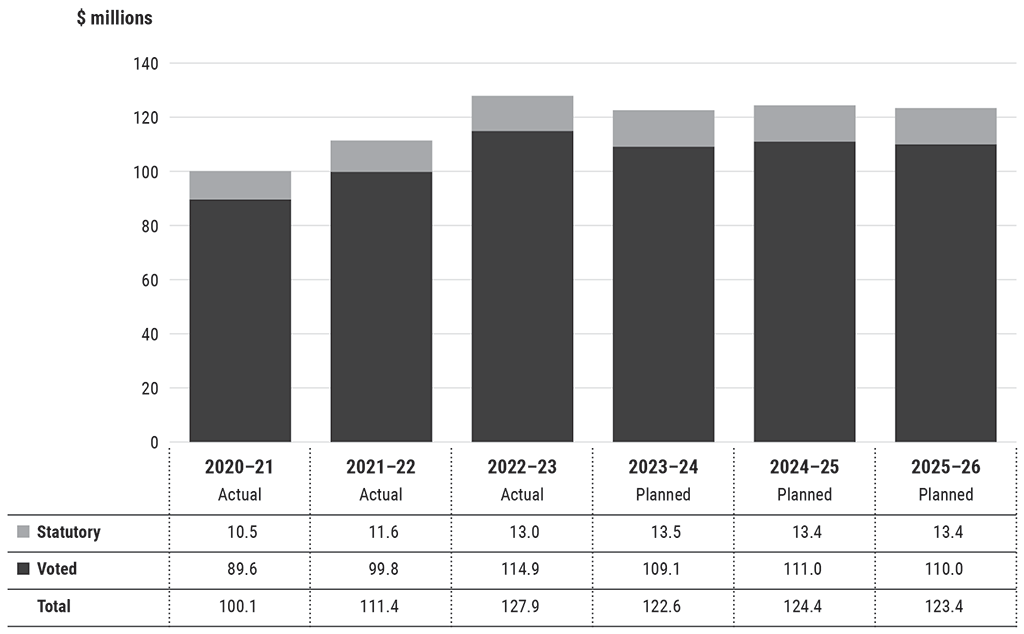

Exhibit 4 shows the trend in our spending based on parliamentary authorities used for the 2020–21 to 2025–26 fiscal years, and Exhibit 5 shows our budgetary performance summary for the 2020–21 to 2024–25 fiscal years.

Exhibit 4—Trend in authorities used (in millions of dollars)

Exhibit 4—text version

| 2020–21 Actual |

2021–22 Actual |

2022–23 Actual |

2023–24 Planned |

2024–25 Planned |

2025–26 Planned |

|

|---|---|---|---|---|---|---|

| Statutory | 10.5 | 11.6 | 13.0 | 13.5 | 13.4 | 13.4 |

| Voted | 89.6 | 99.8 | 114.9 | 109.1 | 111.0 | 110.0 |

| Total | 100.1 | 111.4 | 127.9 | 122.6 | 124.4 | 123.4 |

Exhibit 5—Budgetary performance summary (in millions of dollars)

| 2022–23 Main Estimates |

2022–23 Planned spending |

2023–24 Planned spending |

2024–25 Planned spending |

2022–23 Total authorities available for use |

2020–21 Actual spending (authorities used) |

2021–22 Actual spending (authorities used) |

2022–23 Actual spending (authorities used) |

|---|---|---|---|---|---|---|---|

| 119.9 | 119.9 | 122.6 | 124.4 | 135.6 | 100.1 | 111.4 | 127.9 |

Human resources

Exhibit 6 shows, in full‑time equivalents, the human resources the OAG needed to carry out its operations for the 2022–23 fiscal year.

Exhibit 6—Human resources (full-time equivalents)

| 2020–21 Actual |

2021–22 Actual |

2022–23 Actual |

2022–23 Planned |

2023–24 Planned |

2024–25 Planned |

|---|---|---|---|---|---|

| 632 | 727 | 732 | 747 | 765 | 780 |

Financial, human resources, and performance information for the OAG’s program inventory is available in GC InfoBase.

Expenditures by vote

For information on the OAG’s organizational voted and statutory expenditures, consult the Public Accounts of Canada 2023.

Government of Canada spending and activities

Information on the alignment of the OAG’s spending with the Government of Canada’s spending and activities is available in GC InfoBase.

Financial statements

Statement of Management Responsibility

Including Internal Control Over Financial Reporting

Management of the Office of the Auditor General of Canada (OAG) is responsible for the preparation of the accompanying financial statements for the year ended 31 March 2023, and for all information contained in these statements, in accordance with Canadian public sector accounting standards.

Management is responsible for the integrity and objectivity of the information in these financial statements. Some of the information in the financial statements is based on management’s best estimates and judgment and gives due consideration to materiality. To fulfill its accounting and reporting responsibilities, management maintains a set of accounts that provides a centralized record of the OAG’s financial transactions. Financial information submitted in the preparation of the Public Accounts of Canada, and included in the OAG’s Departmental Results Report, is consistent with these audited financial statements. In preparing the financial statements, management is responsible for assessing the OAG’s ability to continue as a going concern; disclosing matters related to going concern; and using the going concern basis of accounting, as applicable.

Management is also responsible for maintaining an effective system of internal control over financial reporting (ICFR), which is designed to provide reasonable assurance that financial information is reliable; that assets are safeguarded; and that transactions are properly authorized and recorded in accordance with the Financial Administration Act and other applicable legislation, regulations, authorities, and policies.

Management seeks to ensure the objectivity and integrity of data in its financial statements through the careful selection, training, and development of qualified staff; through organizational arrangements that provide appropriate divisions of responsibility; through communications aimed at ensuring that regulations, policies, standards, and managerial authorities are understood throughout the OAG; and through an annual assessment of the effectiveness of the system of ICFR.

The system of ICFR is designed to mitigate risks to a reasonable level and may not prevent or detect all misstatements. It is based on an ongoing process designed to identify key risks, to assess the effectiveness of associated key controls, and to make any necessary adjustments.

The effectiveness and adequacy of the OAG’s system of internal control are reviewed through the work of internal audit staff, who conduct periodic audits of different areas of the OAG’s operations. Also, financial services staff annually monitor ICFR. As a basis for recommending approval of the financial statements to the Auditor General, the OAG’s Audit Committee reviews management’s arrangements for internal controls and the accounting policies employed by the OAG for financial reporting purposes. The Audit Committee also meets independently with the OAG’s internal and external auditors to consider the results of their work.

A risk-based assessment of the system of ICFR for the year ended 31 March 2023 was completed in accordance with the Treasury Board’s Policy on Financial Management. The results and action plans are summarized in the 2022–23 Annex to the Statement of Management Responsibility Including Internal Control Over Financial Reporting.

Raymond Chabot Grant Thornton limited liability partnershipLLP Chartered Professional Accountants, Licensed Public Accountants, the independent auditor for the OAG, has expressed an opinion on the fair presentation of the financial statements of the OAG in conformity with Canadian public sector accounting standards, which does not include an audit opinion on the annual assessment of the effectiveness of the OAG’s ICFR.

[Original signed by]

Karen Hogan, Fellow Chartered Professional AccountantFCPA

Auditor General of Canada

[Original signed by]

Vicki Clement, Chartered Professional AccountantCPA, Chartered AccountantCA

Deputy Chief Financial Officer

Ottawa, Canada

18 July 2023

Independent Auditor’s Report

To the Speaker of the House of Commons:

Report on the Audit of the Financial Statements

Opinion

We have audited the financial statements of the Office of the Auditor General of Canada (the “Office”), which comprise the statement of financial position as at 31 March 2023, and the statements of operations, change in net debt and cash flow for the year then ended, and notes to the financial statements, including a summary of significant accounting policies.

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Office as at 31 March 2023, and the results of its operations, the change in its net debt and its cash flows for the year then ended in accordance with Canadian public sector accounting standards.

Basis for Opinion

We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under those standards are further described in the “Auditor’s responsibilities for the audit of the financial statements” section of our report. We are independent of the Office in accordance with the ethical requirements that are relevant to our audit of the financial statements in Canada, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with Canadian public sector accounting standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Office’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Office or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Office’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Canadian generally accepted auditing standards will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with Canadian generally accepted auditing standards, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

- Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control;

- Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Office’s internal control;

- Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management;

- Conclude on the appropriateness of management's use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Office’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor's report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor's report. However, future events or conditions may cause the Office to cease to continue as a going concern;

- Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Report on Compliance with Specified Authorities

Opinion

In conjunction with the audit of the financial statements, we have audited transactions of the Office coming to our notice for compliance with specified authorities. The specified authorities for which compliance was audited are the Financial Administration Act and its regulations and the Auditor General Act.

In our opinion, the transactions of the Office that came to our notice during the audit of the financial statements have complied, in all material respects, with the specified authorities referred to above.

Responsibilities of Management for Compliance with Specified Authorities

Management is responsible for the Office’s compliance with the specified authorities named above, and for such internal control as management determines is necessary to enable the Office to comply with the specified authorities.

Auditor’s Responsibilities for the Audit of Compliance with Specified Authorities

Our audit responsibilities include planning and performing procedures to provide an audit opinion and reporting on whether the transactions coming to our notice during the audit of the financial statements are in compliance with the specified authorities referred to above.

[Original signed by]

Raymond Chabot Grant Thornton Limited Liability PartnershipLLP

Chartered Professional Accountants,

Licensed Public Accountants

Ottawa, Canada

18 July 2023

Office of the Auditor General of Canada

Statement of Financial Position

as at March 31

| 2023 | 2022 | |

|---|---|---|

| Financial assets | ||

|

Due from the Consolidated Revenue Fund

|

14,926 | 6,619 |

|

Accounts receivable (note 4)

|

1,482 | 1,746 |

|

Accounts receivable held on behalf of the Government of Canada (note 4)

|

(203) | (86) |

| 16,205 | 8,279 | |

| Liabilities | ||

|

Vacation pay

|

8,992 | 9,100 |

|

Accounts payable and accrued liabilities (note 5)

|

15,984 | 7,713 |

|

Sick leave benefits (note 6b)

|

2,441 | 2,482 |

|

Severance benefits (note 6c)

|

1,603 | 1,678 |

|

Maternity/parental leave benefits (note 6d)

|

422 | 934 |

| 29,442 | 21,907 | |

| Net debt | (13,237) | (13,628) |

| Non-financial assets | ||

|

Tangible capital assets (note 7)

|

2,520 | 2,997 |

|

Prepaid expenses

|

483 | 598 |

| 3,003 | 3,595 | |

| Accumulated deficit | (10,234) | (10,033) |

Contractual obligations (note 11)

The accompanying notes are an integral part of these financial statements.

Approved by

[Original signed by]

Karen Hogan, Fellow Chartered Professional AccountantFCPA

Auditor General of Canada

[Original signed by]

Vicki Clement, Chartered Professional AccountantCPA, Chartered AccountantCA

Deputy Chief Financial Officer

Ottawa, Canada

18 July 2023

Office of the Auditor General of Canada

Statement of Operations

for the year ended March 31

| 2023 | 2023 | 2022 | |

|---|---|---|---|

| Planned results (note 13) |

Actual | Actual | |

| Expenses (note 8) | |||

|

Financial audits of Crown corporations, territorial governments, and other organizations, and of the consolidated financial statements of the Government of Canada

|

65,400 | 67,540 | 60,509 |

|

Performance audits and studies

|

54,200 | 58,264 | 49,794 |

|

Professional practices

|

6,500 | 12,085 | 9,207 |

|

Special examinations of Crown corporations

|

5,500 | 5,007 | 5,011 |

|

Sustainable development monitoring activities and environmental petitions

|

3,000 | 2,144 | 2,377 |

| Total cost of operations | 134,600 | 145,040 | 126,898 |

| Revenues | |||

|

International audits

|

1,100 | 1,292 | 780 |

|

Other

|

- | 227 | 90 |

|

Revenues earned on behalf of the Government of Canada

|

- | (236) | (97) |

| Net revenues | 1,100 | 1,283 | 773 |

| Net cost of operations before government funding and transfers | 133,500 | 143,757 | 126,125 |

| Government funding and transfers (note 3) | |||

|

Net cash provided by the Government of Canada

|

- | 118,770 | 112,697 |

|

Change in Due from the Consolidated Revenue Fund

|

- | 8,307 | (1,386) |

|

Services provided without charge (note 10b)

|

- | 16,479 | 15,453 |

| Total government funding and transfers | 135,655 | 143,556 | 126,764 |

| Annual (deficit)/surplus | 2,155 | (201) | 639 |

| Accumulated deficit, beginning of year | (10,033) | (10,033) | (10,672) |

| Accumulated deficit, end of year | (7,878) | (10,234) | (10,033) |

The accompanying notes are an integral part of these financial statements.

Office of the Auditor General of Canada

Statement of Change in Net Debt

for the year ended March 31

| 2023 | 2023 | 2022 | |

|---|---|---|---|

| Planned results (note 13) |

Actual | Actual | |

| Annual (deficit)/surplus | 2,155 | (201) | 639 |

| Acquisition of tangible capital assets (note 7) | (2,300) | (997) | (713) |

| Amortization of tangible capital assets (notes 7 and 8) | 850 | 751 | 674 |

| Write-off of tangible capital assets | - | 723 | - |

| 705 | 276 | 600 | |

| Decrease/(increase) in prepaid expenses | - | 115 | (45) |

| Decrease in net debt, during the year | 705 | 391 | 555 |

| Net debt, beginning of year | (13,628) | (13,628) | (14,183) |

| Net debt, end of year | (12,923) | (13,237) | (13,628) |

The accompanying notes are an integral part of these financial statements.

Office of the Auditor General of Canada

Statement of Cash Flow

for the year ended March 31

| 2023 | 2022 | |

|---|---|---|

| Operating transactions | ||

|

Cash paid for

|

||

|

Employee salaries, wages, and benefits

|

(90,937) | (83,593) |

|

Services, transportation, communication, and other expenses

|

(18,886) | (18,734) |

|

Statutory contributions to employee benefit plans

|

(11,957) | (13,210) |

| (121,780) | (115,537) | |

|

Cash received from

|

||

|

Sales tax recovered

|

1,546 | 1,793 |

|

Salaries and benefits recovered

|

1,155 | 536 |

|

International audits

|

653 | 980 |

|

Other

|

404 | 221 |

| 3,758 | 3,530 | |

|

Cash used by operating transactions

|

(118,022) | (112,007) |

| Capital transactions | ||

|

Cash used to acquire tangible capital assets

|

(748) | (690) |

|

Cash applied to capital transactions

|

(748) | (690) |

| Net cash provided by the Government of Canada (note 3c) | (118,770) | (112,697) |

The accompanying notes are an integral part of these financial statements.

Office of the Auditor General of Canada

Notes to the financial statements for the year ended 31 March 2023

1. Authority and objective

The Auditor General Act, the Financial Administration Act, and a variety of other acts and orders‑in‑council set out the duties of the Auditor General and the Commissioner of the Environment and Sustainable Development.

The core responsibility of the Office of the Auditor General of Canada (OAG) is legislative auditing and consists of performance audits and studies of departments and agencies; the audit of the consolidated financial statements of the Government of Canada; financial audits of Crown corporations, territorial governments, and other organizations; special examinations of Crown corporations; and sustainable development monitoring activities and environmental petitions.

Pursuant to the Financial Administration Act, the OAG is a department of the Government of Canada. It is listed in Schedule I.1 of the act as a division or a branch of the federal public administration, and in Schedule V of the act as a separate agency. The OAG is not subject to income taxes under the provisions of the Income Tax Act.

2. Significant accounting policies

a) Basis of presentation

The financial statements of the OAG have been prepared by management in accordance with Canadian public sector accounting standards (PSAS).

b) Parliamentary authorities

The OAG is funded by the Government of Canada through parliamentary authorities. Financial reporting of authorities provided to the OAG does not parallel financial reporting according to PSAS, since authorities are primarily based on cash flow requirements. Consequently, items recognized in the Statement of Operations and in the Statement of Financial Position are not necessarily the same as those provided through authorities from Parliament. Note 3a provides a reconciliation between the 2 bases of reporting.

c) Revenues

Revenues are from international audits and from other activities, such as audit professional services provided to members of the Canadian Council of Legislative Auditors.

Revenues are recognized in the period in which services are rendered or in the period in which the underlying transaction or event that gave rise to the revenue takes place.

Of those revenues, amounts that are considered to be earned on behalf of the Government of Canada are not available for discharging the OAG’s liabilities. Although the OAG is expected to maintain accounting control, it has no authority regarding the disposition of those revenues. As a result, revenues earned on behalf of the Government of Canada are presented as a reduction of the OAG’s gross revenues.

d) Net cash provided by the Government of Canada

The OAG operates within the Consolidated Revenue Fund (CRF), which is administered by the Receiver General for Canada. All cash received by the OAG is deposited to the CRF, and all cash disbursements made by the OAG are paid from the CRF. The net cash provided by the Government of Canada is the difference between all cash receipts and all cash disbursements, including transactions between departments of the Government of Canada.

e) Due from the Consolidated Revenue Fund

Amounts due from or to the CRF are the result of timing differences at year‑end between when a transaction affects authorities and when it is processed through the CRF. Amounts due from the CRF represent the net amount of cash that the OAG is entitled to draw from the CRF, without further parliamentary authorities to discharge its liabilities.

f) Accounts receivable and Accounts receivable held on behalf of the Government of Canada

Accounts receivable are stated at the lower of cost and net recoverable value. A valuation allowance is recorded for accounts receivable where recovery is considered uncertain.

Accounts receivable held on behalf of the Government of Canada are presented as a reduction to the financial assets on the Statement of Financial Position because they are not available to discharge the OAG’s liabilities.

g) Tangible capital assets

By nature, tangible capital assets are normally used to provide future services.

Tangible capital assets are recorded at historical cost less accumulated amortization. The OAG capitalizes the costs associated with the development of software used internally, such as installation costs, professional service contract costs, and salary costs of employees directly associated with these projects. The costs of software maintenance, project management and administration, data conversion, and training and development are expensed in the year incurred.

When conditions indicate that a tangible capital asset no longer contributes to the OAG’s ability to provide future services, or that the value of future economic benefits associated with the tangible capital asset is less than its net book value, the cost of the tangible capital asset is reduced to reflect the decline in the asset’s value. Any write‑downs of tangible capital assets are accounted for as expenses in the Statement of Operations and are not subsequently reversed.

The cost of work in progress is transferred to the applicable asset class in the year the assets are put into service.

Amortization of tangible capital assets begins when assets are put into use and is recorded using the straight‑line method over the estimated useful lives of the assets as follows:

| Tangible capital asset class | Useful life |

|---|---|

| Leasehold improvements | Lesser of the remaining term of the lease or the useful life of the improvements |

| Furniture and fixtures | 10 years |

| Informatics software | 5 years |

| Informatics hardware and infrastructure | 5 years |

| Office equipment | 4 to 10 years |

| Motor vehicle | 5 years |

| Work in progress | In accordance with asset class, once in service |

h) Accounts payable and accrued liabilities

Accounts payable and accrued liabilities represent obligations of the OAG for salaries and wages, for material and supply purchases, and for the cost of services rendered to the OAG.

Salary-related accrued liabilities are primarily determined using employees’ salaries at year‑end. Accounts payable and accrued liabilities are measured at cost.

i) Vacation pay

Vacation pay is accrued as the benefit is earned by the employees under their respective labour contracts and conditions of employment. The liability represents all unused vacation pay benefits accruing to employees. The employees’ salaries at year‑end determine the amount of these accrued vacation pay benefits.

j) Employee benefits

i) Pension benefits

All eligible employees participate in the Public Service Pension Plan, a plan administered by the Government of Canada. The OAG’s contributions are currently based on a multiple of an employee’s required contributions and may change over time, depending on the experience of the plan. The OAG’s contributions are expensed during the year in which the services are rendered and represent its total pension obligation. The OAG is not required to make contributions with respect to any actuarial deficiencies of the plan.

ii) Health and dental benefits

The Government of Canada sponsors employee benefit plans (health and dental) in which the OAG participates. Employees are entitled to health and dental benefits, as provided for under labour contracts and conditions of employment. The OAG’s contributions to the plans, which are provided without charge by the Treasury Board of Canada Secretariat, are recorded at cost based on a percentage of the salary expenses and charged to personnel expenses in the year incurred. They represent the OAG’s total obligation to the plans. Current legislation does not require the OAG to make contributions for any future unfunded liabilities of the plans.

iii) Sick leave benefits

Employees are eligible to accumulate sick leave benefits until the end of employment, according to their labour contracts and conditions of employment. Sick leave benefits are earned based on employee services rendered and are paid upon an illness or injury‑related absence. These are accumulating non‑vesting benefits that can be carried forward to future years, but are not eligible for payment on retirement or termination, nor can these be used for any other purpose. A liability is recorded for unused sick leave credits expected to be used in future years in excess of future allotments, based on an actuarial valuation using an accrued benefit method. Changes in actuarial assumptions and any variance between the expected and the actual experience of the sick leave benefit plan give rise to actuarial gains or losses. These gains or losses are amortized on a straight‑line basis over the expected average remaining service life of the employees, starting in the fiscal year following the one in which they arose.

iv) Severance benefits

The accumulation of severance benefits for employees ceased in the 2012–13 fiscal year. The accrued benefit obligation is determined using employees’ salaries at year‑end and the number of weeks earned but unpaid for employees who have elected to defer the receipt of their full or partial severance benefits payment.

v) Maternity/parental leave benefits

Employees are entitled to maternity/parental leave benefits as provided for under labour contracts and conditions of employment. The benefits earned are event‑driven, meaning that the OAG’s obligation for the cost of the entire benefit arises upon occurrence of a specific event, being the commencement of the maternity/parental leave. The accrued benefit obligation and benefit expenses are based on management’s best estimates.

k) Related party transactions

i) Inter-entity transactions

The OAG is related as a result of common ownership to all Government of Canada departments, agencies, and Crown corporations. The OAG enters into transactions with these organizations in the normal course of business. These transactions are measured as follows:

- Inter-entity transactions are measured at the exchange amount when undertaken on similar terms and conditions to those adopted if the entities were dealing at arm’s length, or where transactions are allocated costs and recoveries.

- Common services provided without charge by other government departments are recorded as operating expenses by the OAG at the carrying amount of the providing department. A corresponding amount is reported as government funding in the Statement of Operations.

- Other inter-entity transactions are measured at the carrying amount of the providing department.

ii) Other related party transactions

Related parties include key management personnel who have the authority and responsibility for planning, directing, and controlling the activities of the OAG. Related parties also include the close family members of these personnel. The OAG has defined its key management personnel to be the Executive Committee members and parties related to them.

The OAG is also related to parties subject to shared control.

Related party transactions, other than inter-entity transactions, are recorded at the exchange amount.

l) Allocation of expenses

All direct expenses related to the delivery of audits and professional practice projects, such as salary, professional services, travel, and other associated costs, are allocated to each audit and professional practice project. All other expenses, including services provided without charge, are treated as overhead and are allocated to audits and professional practice projects on the basis of the direct staff cost charged to them.

m) Measurement uncertainty

These financial statements are prepared in accordance with PSAS. These standards require management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues, government funding and transfers, and expenses during the reporting period. The amount of services provided without charge, the assumptions underlying the liability calculation for sick leave benefits, and the estimated useful lives of tangible capital assets are the most significant items for which estimates are used. Actual results could differ significantly from the estimates. These estimates are reviewed annually, and as adjustments become necessary, they are recognized in the financial statements in the period in which they become known.

3. Parliamentary authorities

The OAG is funded through annual parliamentary authorities. Items recognized in the Statement of Operations in one year may be funded through parliamentary authorities in prior, current, or future years. Accordingly, the OAG has different net results of operations for the year on a government funding basis than on an accrual accounting basis. The differences are reconciled in the following tables.

a) Reconciliation of net cost of operations to current year authorities used

| 2023 | 2022 | |

|---|---|---|

| Net cost of operations before government funding and transfers | 143,757 | 126,125 |

| Adjustments for items recorded as part of net cost of operations but not affecting current year authorities: | ||

|

Services provided without charge by other government departments

|

(16,479) | (15,453) |

|

Amortization of tangible capital assets

|

(751) | (674) |

|

Write-off of tangible capital assets

|

(723) | - |

|

(Decrease)/increase in prepaid expenses

|

(115) | 45 |

|

Revenues available for spending in future years/(Recoveries from prior year’s revenues)

|

647 | (173) |

|

Adjustment to previous year accruals

|

61 | 196 |

| Total items recorded as part of net cost of operations but not affecting current year authorities | (17,360) | (16,059) |

| Adjustments for items not recorded as part of net cost of operations but affecting current year authorities: | ||

|

Acquisition of tangible capital assets

|

997 | 713 |

|

Decrease in liabilities not charged to authorities

|

391 | 555 |

|

Other

|

71 | 37 |

| Total items not recorded as part of net cost of operations but affecting current year authorities | 1,459 | 1,305 |

| Current year authorities used | 127,856 | 111,371 |

b) Authorities provided and used

| 2023 | 2022 | |

|---|---|---|

| Main Estimates | ||

|

Vote 1—Program expenditures

|

107,013 | 104,834 |

|

Statutory amounts—Contributions to employee benefit plans

|

12,869 | 12,523 |

| Total Main Estimates | 119,882 | 117,357 |

| Supplementary Estimates—Vote 1c—Program expenditures | - | 1,500 |

| Supplementary voted authorities | 11,282 | 87 |

| Authorities carried forward from previous year | 4,302 | 3,179 |

| Adjustment to statutory contributions to employee benefit plans | 87 | (912) |

| Current year authorities provided | 135,553 | 121,211 |

| Less: Lapsed authorities | (7,697) | (9,840) |

| Current year authorities used | 127,856 | 111,371 |

The OAG may carry forward up to 5% of its operating budget (based on Main Estimates program expenditures) into the next fiscal year, subject to parliamentary approval. The OAG expects to carry forward $5.5 million ($5.4 million in 2021–22).

c) Reconciliation of net cash provided by the Government of Canada to current year authorities used

| 2023 | 2022 | |

|---|---|---|

| Net cash provided by the Government of Canada | 118,770 | 112,697 |

| Change in Due from the Consolidated Revenue Fund | ||

|

Decrease/(increase) in Accounts receivable and Accounts receivable held on behalf of the Government of Canada

|

381 | (837) |

|

Increase/(decrease) in liabilities charged to authorities

|

7,926 | (549) |

| Total—Change in Due from the Consolidated Revenue Fund | 8,307 | (1,386) |

|

Revenues available for spending in future years/(Recoveries from prior year’s revenues)

|

647 | (173) |

|

Adjustment to previous year accruals

|

61 | 196 |

|

Other

|

71 | 37 |

| Current year authorities used | 127,856 | 111,371 |

4. Accounts receivable

The following table presents details of the OAG’s accounts receivable:

| 2023 | 2022 | |

|---|---|---|

| International audits and audit‑related professional services | 1,023 | 312 |

| Other government departments and agencies | 327 | 1,352 |

| Other | 132 | 82 |

| Gross accounts receivable | 1,482 | 1,746 |

| Accounts receivable held on behalf of the Government of Canada | (203) | (86) |

| Net accounts receivable | 1,279 | 1,660 |

5. Accounts payable and accrued liabilities

The following table presents details of the OAG’s accounts payable and accrued liabilities:

| 2023 | 2022 | |

|---|---|---|

| Accrued employee salaries | 13,376 | 4,927 |

| Due to others | 2,608 | 2,786 |

| Total | 15,984 | 7,713 |

6. Employee benefits

a) Pension benefits

The OAG’s eligible employees participate in the Public Service Pension Plan, which is established and governed by the Public Service Superannuation Act, and sponsored and administered by the Government of Canada. Pension benefits accrue up to a maximum period of 35 years at a rate of 2% per year of pensionable service, times the average of the best 5 consecutive years of earnings. The benefits are integrated with Canada/Québec Pension Plan benefits, and they are indexed to inflation.

Both the employees and the OAG contribute to the cost of the Public Service Pension Plan. Because of the amendment of the Public Service Superannuation Act following the implementation of provisions related to Economic Action Plan 2012, employee contributors have been divided into 2 groups: Group 1 relates to existing plan members as of 31 December 2012, and Group 2 relates to members joining the Public Service Pension Plan as of 1 January 2013. Each group has a distinct contribution rate.

The 2022–23 expense amounts to $8.5 million ($7.8 million in 2021–22). For Group 1 members, the expense represents approximately 1.02 times (1.01 times in 2021–22) the employee contributions and, for Group 2 members, approximately 1.00 times (1.00 times in 2021–22) the employee contributions.

The OAG’s responsibility with regard to the Public Service Pension Plan is limited to its contributions. Actuarial surpluses or deficiencies are recognized in the financial statements of the Government of Canada, as the plan’s sponsor.

b) Sick leave benefits

Employees are credited, based on service, a maximum of 15 days annually for use as paid absences due to illness or injury. The sick leave benefit obligation is unfunded and will be paid from future parliamentary authorities.

The most recent actuarial valuation of the sick leave accrued benefit obligation performed for accounting purposes was done as at 31 March 2021 and extrapolated to 31 March 2023. Actuarial assumptions are used to determine the obligation. They are reviewed at March 31 of each year and are management’s best estimate based on an analysis of the historical data up to the reporting date. The key assumptions used are a discount rate of 3.05% (2.4% in 2021–22), which is based on an average yield of government borrowings over the expected average remaining service life of employees of 9 years (9 years in 2021–22); a rate of salary increase of 3.75% (3.75% in 2021–22); an average turnover rate of 8.3% (8.3% in 2021–22); an average retirement age of 58 (58 in 2021–22) for Group 1 members and 61 (61 in 2021–22) for Group 2 members; and the excess utilization and underutilization of sick leave credits, which are based on plan experience and representative of the different groups of employees covered.

Information about the sick leave benefits as at March 31 is as follows:

| 2023 | 2022 | |

|---|---|---|

| Accrued benefit obligation, beginning of year | 2,666 | 3,099 |

|

Current year benefit costNote 1

|

537 | 618 |

|

Interest on the accrued benefit obligationNote 1

|

70 | 55 |

|

Benefits paid

|

(613) | (959) |

|

Actuarial gain

|

(136) | (147) |

| Accrued benefit obligation, end of year | 2,524 | 2,666 |

| Unamortized accumulated actuarial loss, beginning of year | (184) | (313) |

|

Actuarial gain for the year

|

136 | 147 |

|

Amortization of actuarial gain recognized in the yearNote 1

|

(35) | (18) |

| Unamortized accumulated actuarial loss, end of year | (83) | (184) |

| Accrued benefit liability | 2,441 | 2,482 |

Changes in assumptions can result in significantly higher or lower estimates of the accrued benefit obligation. The following table illustrates the possible impact of a change in the actuarial assumptions on the accrued benefit obligation as at March 31:

| Assumptions | Increase (decrease) in the accrued benefit obligation |

|

|---|---|---|

| 2023 | 2022 | |

| Discount rate | ||

|

Increase by 1%

|

(144) | (157) |

|

Decrease by 1%

|

162 | 177 |

| Salary increase rate | ||

|

Increase by 1%

|

133 | 146 |

|

Decrease by 1%

|

(121) | (133) |

| Retirement age | ||

|

Increase by 1 year

|

245 | 264 |

|

Decrease by 1 year

|

(234) | (251) |

| Turnover rate | ||

|

Increase factors by 10%

|

(91) | (100) |

|

Decrease factors by 10%

|

99 | 108 |

| Sick leave utilization rates | ||

|

Increase factors by 10%

|

313 | 332 |

|

Decrease factors by 10%

|

(298) | (316) |

c) Severance benefits

The OAG’s severance benefit obligation is unfunded and will be paid from future parliamentary authorities.

The following table presents information about severance benefits, measured as at March 31:

| 2023 | 2022 | |

|---|---|---|

| Accrued benefit obligation, beginning of year | 1,678 | 1,834 |

|

Current year benefit cost

|

173 | 35 |

|

Benefits paid

|

(248) | (191) |

| Accrued benefit obligation, end of year | 1,603 | 1,678 |

d) Maternity/parental leave benefits

Management determined the accrued benefit obligation and benefit expenses of maternity/parental leave benefits based on the difference between 93% of the employee’s weekly rate of pay and the weekly maternity/parental leave benefit the employee is entitled to receive under the Employment Insurance program or the Québec Parental Insurance Plan. The maternity/parental leave benefit obligation is unfunded and will be paid from future parliamentary authorities.

The following table presents information about maternity/parental leave benefits, measured as at March 31:

| 2023 | 2022 | |

|---|---|---|

| Accrued benefit obligation, beginning of year | 934 | 373 |

|

Current year benefit cost

|

1,031 | 1,574 |

|

Benefits paid

|

(1,543) | (1,013) |

| Accrued benefit obligation, end of year | 422 | 934 |

7. Tangible capital assets

| Cost | Accumulated amortization | 2023 Net book value |

2022 Net book value |

||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Opening balance | Acquisitions | Transfers | Disposals and write‑offs | Closing balance | Opening balance | Amortization | Disposals and write‑offs | Closing balance | |||

| Informatics software | 6,402 | - | - | - | 6,402 | 4,941 | 449 | - | 5,390 | 1,012 | 1,461 |

| Work in progress | 769 | 682 | (47) | (722) | 682 | - | - | - | - | 682 | 769 |

| Informatics hardware and infrastructure | 2,682 | - | - | - | 2,682 | 2,062 | 251 | - | 2,313 | 369 | 620 |

| Leasehold improvements | 3,428 | 273 | 47 | (674) | 3,074 | 3,376 | 24 | (674) | 2,726 | 348 | 52 |

| Office equipment | 1,196 | 42 | - | (17) | 1,221 | 1,162 | 11 | (16) | 1,157 | 64 | 34 |

| Motor vehicle | 45 | - | - | - | 45 | 11 | 9 | - | 20 | 25 | 34 |

| Furniture and fixtures | 4,331 | - | - | (970) | 3,361 | 4,304 | 7 | (970) | 3,341 | 20 | 27 |

| Total | 18,853 | 997 | - | (2,383) | 17,467 | 15,856 | 751 | (1,660) | 14,947 | 2,520 | 2,997 |

8. Expenses by object

The summary of expenses by object for the year ended March 31 is as follows:

| 2023 | 2022 | |

|---|---|---|

| Personnel | 119,033 | 102,150 |

| Rentals | 9,922 | 9,837 |

| Professional and special services | 9,728 | 11,236 |

| Transportation and communications | 2,192 | 712 |

| Information | 1,248 | 925 |

| Small machinery and equipment | 1,109 | 1,050 |

| Amortization of tangible capital assets | 751 | 674 |

| Write‑off of tangible capital assets | 723 | - |

| Utilities, materials, and supplies | 148 | 118 |

| Repairs and maintenance | 116 | 141 |

| Interest on the sick leave accrued benefit obligation | 70 | 55 |

| Total cost of operations | 145,040 | 126,898 |

The total cost of operations includes services provided without charge by other government departments as disclosed in note 10b.

9. Participation in other organizations

a) Canadian Audit and Accountability Foundation

The OAG is a member of the Canadian Audit and Accountability Foundation (CAAF), a not‑for‑profit corporation dedicated to promoting and strengthening public‑sector performance audit, oversight, and accountability in Canada and abroad through research, education, and knowledge sharing.

In the 2022–23 fiscal year, the OAG paid fees and provided in‑kind services to the CAAF totalling $0.6 million ($0.7 million in 2021–22). As at 31 March 2023, the OAG held approximately 41% (44% in 2021–22) of the member voting rights of the CAAF and did not have any representation on the Board of Directors of the CAAF.

The OAG does not control the CAAF; therefore, the CAAF is not consolidated in these financial statements.

b) Canadian Council of Legislative Auditors

The OAG is a member of the Canadian Council of Legislative Auditors (CCOLA). The CCOLA is devoted to sharing information and supporting the continued development of auditing methodology, practices, and professional development. The CCOLA’s membership consists of all the provincial and federal legislative audit offices. The CCOLA has 1 associate member (the Office of the Auditor General of Bermuda) and 1 observer (the Office of the Auditor General of the Cayman Islands).

The OAG contributes to the CCOLA through the provision of secretariat and various administrative and support services. The CCOLA reports annually on its operations for the period from October 1 to September 30. For the year ended 30 September 2022, the OAG provided $0.2 million in services ($0.2 million in 2020–21) to the CCOLA.

The OAG does not control the CCOLA; therefore, the CCOLA is not consolidated in these financial statements.

10. Related party transactions

a) Inter-entity transactions

The OAG had the following inter‑entity transactions during the year, and the following balances as at March 31:

| 2023 | 2022 | |

|---|---|---|

| Expenses—Other government departments and agencies | 15,357 | 13,599 |

| Accounts receivable—Other government departments and agencies | 327 | 1,352 |

| Accounts payable—Other government departments and agencies | 485 | 153 |

Expenses disclosed in the table above exclude common services provided without charge, which are disclosed in the next table. The most significant components of the expenses are related to the statutory contributions to employee benefit plans, translation services, health and training services, and security and network services.

b) Common services provided without charge by other government departments

During the year, the OAG received the following services without charge from certain common service organizations. The expenses related to these services have been recorded in the Statement of Operations and are disclosed in note 8.

| 2023 | 2022 | |

|---|---|---|

| OAG contribution to the health and dental insurance plans—Treasury Board of Canada Secretariat | 8,632 | 7,618 |

| Office accommodation—Public Services and Procurement Canada | 7,847 | 7,835 |

| Services provided without charge | 16,479 | 15,453 |

The Government of Canada has centralized some of its administrative activities for efficiency, cost‑effectiveness purposes, and economic delivery of programs to the public. As a result, the government uses central agencies and common services organizations so that one department performs services for all other departments and agencies without charge. The costs of these services, such as the payroll and cheque‑issuance services provided by Public Services and Procurement Canada, are not included in the Statement of Operations, as they are not significant.

c) Common services provided without charge to other government departments

During the year, the OAG provided services without charge to federal departments and agencies, Crown corporations, and other government organizations. These services were related to the conduct of independent audits. The costs related to the provision of these services are reflected in the Statement of Operations.

d) Parties subject to shared control

The OAG is related to the Canadian Council of Legislative Auditors through its membership.

11. Contractual obligations

The nature of the OAG’s activities can result in contracts and obligations whereby the OAG will be obligated to make future payments when the services/goods are received. Contractual obligations estimated as at 31 March 2023 are summarized as follows:

| 2024 | 2025 | 2026 | 2027 | Total | |

|---|---|---|---|---|---|

| Goods and services | 2,198 | 946 | 946 | 143 | 4,233 |

| Professional services | 2,581 | 351 | 257 | - | 3,189 |

| Operating leases | 6 | - | - | - | 6 |

| Total | 4,785 | 1,297 | 1,203 | 143 | 7,428 |

Contractual obligations with related parties total $3.9 million and are included in the above table.

12. Financial instruments

The following analysis presents the OAG’s exposure to credit and liquidity risks at the reporting date.

a) Credit risk

The OAG is exposed to credit risk resulting from the possibility that parties may default on their financial obligations to pay the OAG. Management believes that the risk of loss on its accounts receivable balances is low because of the credit quality of these parties. Accounts receivable balances are managed and analyzed on an ongoing basis. Accordingly, management believes that all accounts receivable will be collected and has determined that a valuation allowance is not required.

b) Liquidity risk

Liquidity risk is the risk that the OAG will encounter difficulty in meeting its obligation associated with financial liabilities. The OAG’s objective for managing liquidity risk is to manage operations and cash expenditures within the authorities approved by Parliament. Management believes that this risk is low.

13. Planned results

The planned results amounts in the “Expenses” and “Revenues” sections of the Statement of Operations are the amounts reported in the Future‑Oriented Statement of Operations included in the 2022–23 Departmental Plan. The planned results amounts on the line “Total government funding and transfers” of the Statement of Operations and in the Statement of Change in Net Debt were prepared for internal management purposes and have not been previously published.

14. Comparative figures

Certain 2021–22 comparative figures have been reclassified to conform to the presentation adopted for the 2022–23 fiscal year.

Corporate information

Organizational profile

Auditor General of Canada: Karen Hogan, Fellow Chartered Professional AccountantFCPA

Main legislative authorities:

Auditor General Act, Revised Statutes of CanadaR.S.C. 1985, c. A-17

Financial Administration Act, R.S.C. 1985, c. F-11

Year established: 1878

Minister: The Honourable Chrystia Freeland, Privy CouncillorP.C., Member of ParliamentM.P., Minister of FinanceNote *

Raison d’être, mandate, and role: Who we are and what we do

“Raison d’être, mandate, and role: Who we are and what we do” is available on the Office of the Auditor General of Canada’s (OAG’s) website.

Operating context

Information on the operating context is available on the OAG’s website.

Reporting framework

The OAG’s departmental results framework and program inventory of record for the 2022–23 fiscal year are shown in Exhibit 7.

Exhibit 7—Departmental results framework and program inventory

|

Core responsibility: Legislative auditing |

Description Our audit reports provide objective, fact‑based information and advice on government programs and activities. With our audits, we assist Parliament in its authorization and oversight of government spending and operations. Our audits also help territorial legislatures, boards of Crown corporations, and audit committees in their oversight of the management of government activities. Those charged with governance use our audit findings to hold their respective organizations to account for the handling of public funds. Financial audits assess whether the annual financial statements of the Government of Canada, Crown corporations, and others are presented fairly, consistent with applicable accounting standards. Performance audits assess whether government organizations manage programs with due regard for economy, efficiency, and environmental impact, and measure their effectiveness. Over the last 2 years, we have also incorporated the assessment of equity, diversity, and inclusion as a priority area for our performance audits. Special examinations assess whether Crown corporations systems and practices provide reasonable assurance that assets are safeguarded, resources are managed economically and efficiently, and operations are managed effectively. |

|---|---|

|

Result and indicators |

Well-managed and accountable government

|

|

Program inventory |

|

Supporting information on the program inventory

Financial, human resources, and performance information for the OAG’s program inventory is available in GC InfoBase.

Supplementary information tables

The following supplementary information tables are available on the OAG’s website:

- reporting on green procurement

- gender-based analysis plus

- United Nations’ 2030 Agenda for Sustainable Development and the United Nations’ Sustainable Development Goals

Report on staffing

The Auditor General has the staffing authorities of the Public Service Commission of Canada through the Auditor General Act. The commission must report annually to Parliament for the previous fiscal year on matters under its jurisdiction; therefore, the OAG commits to reporting annually on its staffing.

The following description takes into account the OAG’s people management framework and the monitoring requirements set forth in the OAG’s Policy on Staffing. It summarizes the areas of accountability and identifies the indicators present at the OAG. The framework is intended to ensure a values‑based staffing system. Through this framework, the core principles of merit and non‑partisanship are applied in accordance with the core values of fairness, transparency, access, and representativeness.

Delegation of staffing and support to managers

Delegation

The Auditor General has the authority related to human resource management in accordance with the Auditor General Act and may delegate this authority to management. Moreover, staffing responsibilities are fulfilled in accordance with the OAG’s Delegated Human Resources Authorities instrument to align with senior management roles and responsibilities.

Knowledge and support